Get Tennessee Inh 300 Template in PDF

When individuals in Tennessee make gifts to others, they may need to navigate the complexities of the Tennessee Gift Tax by utilizing the INH 300 form, mandated by the Tennessee Department of Revenue. This form serves as a critical means to report and calculate taxes on gifts made during a calendar year, requiring submission by April 15 of the following year if the value of all gifts surpasses certain exemption levels. It intricately details the process for reporting gifts, computing taxes, and claiming exemptions or deductions, including those for gifts to a spouse (marital deduction) and gifts to charitable organizations. Moreover, it articulates considerations for both residents and non-residents of Tennessee, differentiating between gifts of real estate, tangible personal property, and intangible personal property. Specific provisions are laid out for electing to split gifts between spouses, thereby affecting gift valuation and tax implications. Additionally, the form accommodates for the valuation of a plethora of gift types, from real estate and securities to more unique items, ensuring accurate tax computation and reporting. It emphasizes the importance of accurate gift valuation, adherence to deadlines, and the potential fiscal responsibilities that come with gift-giving, providing a detailed framework for individuals to report their gifts in compliance with state tax laws.

Document Preview Example

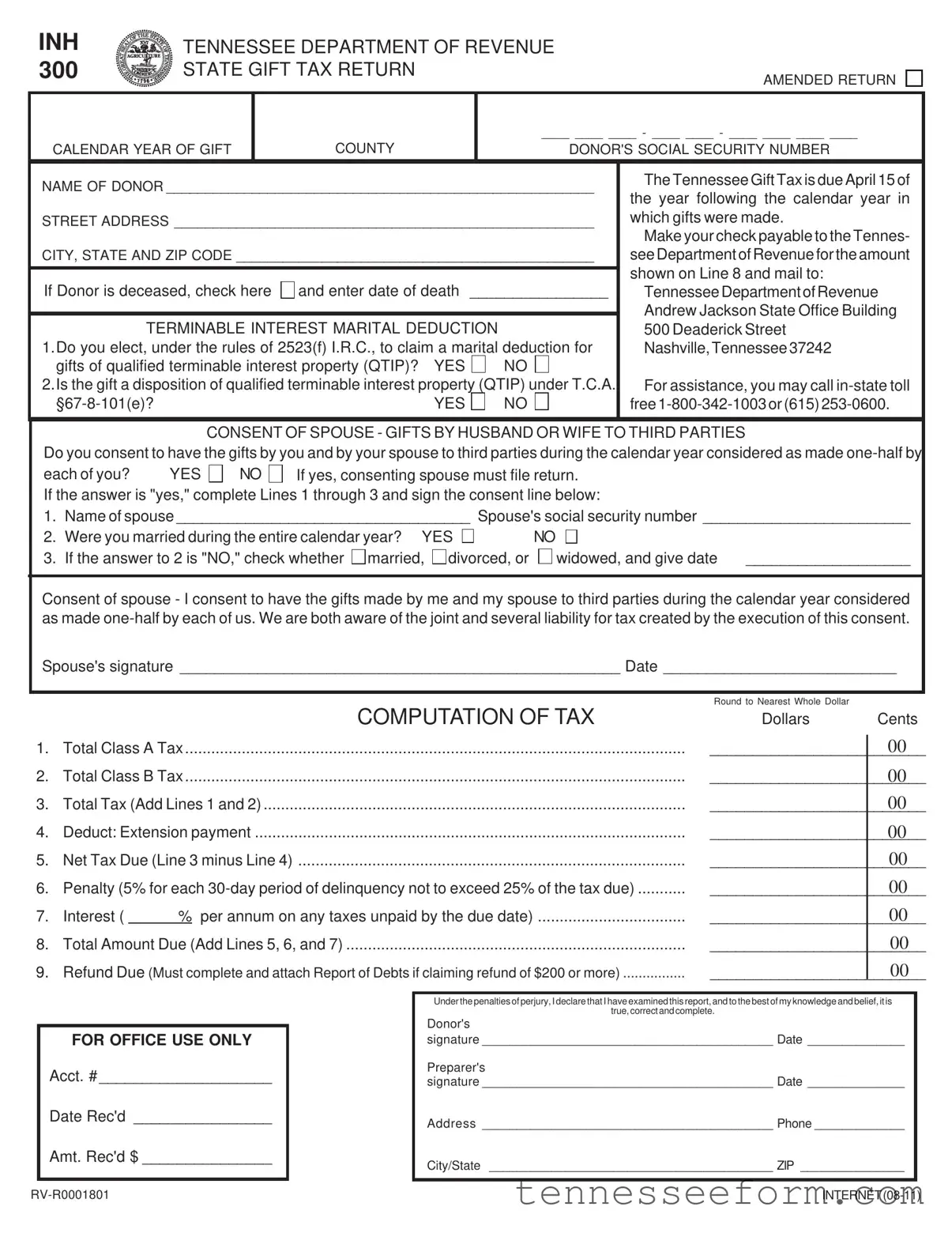

INH 300

TENNESSEE DEPARTMENT OF REVENUE STATE GIFT TAX RETURN

AMENDED RETURN

|

|

____ ____ ____ - ____ ____ - ____ ____ ____ ____ |

CALENDAR YEAR OF GIFT |

COUNTY |

DONOR'S SOCIAL SECURITY NUMBER |

|

|

|

NAME OF DONOR _______________________________________________________ |

The Tennessee Gift Tax is due April 15 of |

||||||||||

the year following the calendar year in |

|||||||||||

|

|

|

|

|

|

|

|

|

|

||

STREET ADDRESS ______________________________________________________ |

which gifts were made. |

||||||||||

|

|

|

|

|

|

|

|

|

|

Make your check payable to the Tennes- |

|

CITY, STATE AND ZIP CODE ______________________________________________ |

see Department of Revenue for the amount |

||||||||||

|

|

|

|

|

|

|

|

|

|

shown on Line 8 and mail to: |

|

If Donor is deceased, check here |

|

and enter date of death |

________________ |

||||||||

|

Tennessee Department of Revenue |

||||||||||

|

|

|

|

|

|

|

|

|

|

Andrew Jackson State Office Building |

|

TERMINABLE INTEREST MARITAL DEDUCTION |

|||||||||||

500 Deaderick Street |

|||||||||||

1.Do you elect, under the rules of 2523(f) I.R.C., to claim a marital deduction for |

Nashville, Tennessee 37242 |

||||||||||

gifts of qualified terminable interest property (QTIP)? YES |

|

|

NO |

|

|

|

|

||||

2.Is the gift a disposition of qualified terminable interest property (QTIP) under T.C.A. |

For assistance, you may call |

||||||||||

|

YES |

|

|

NO |

|

|

free |

||||

CONSENT OF SPOUSE - GIFTS BY HUSBAND OR WIFE TO THIRD PARTIES

Do you consent to have the gifts by you and by your spouse to third parties during the calendar year considered as made

each of you? |

YES |

|

NO |

|

If yes, consenting spouse must file return. |

|

||||||||||||

If the answer is "yes," complete Lines 1 through 3 and sign the consent line below: |

|

|||||||||||||||||

1. |

Name of spouse __________________________________ Spouse's social security number ________________________ |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||

2. |

Were you married during the entire calendar year? YES |

|

|

NO |

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

If the answer to 2 is "NO," check whether |

|

married, |

|

divorced, or |

|

|

widowed, and give date |

___________________ |

|||||||||

Consent of spouse - I consent to have the gifts made by me and my spouse to third parties during the calendar year considered as made

Spouse's signature ___________________________________________________ Date ___________________________ |

||||

|

|

|

Round to Nearest Whole Dollar |

|

|

|

COMPUTATION OF TAX |

Dollars |

Cents |

1. |

Total Class A Tax |

|

00 |

|

2. |

Total Class B Tax |

|

00 |

|

3. |

Total Tax (Add Lines 1 and 2) |

|

00 |

|

4. |

Deduct: Extension payment |

|

00 |

|

5. |

Net Tax Due (Line 3 minus Line 4) |

|

00 |

|

6. |

Penalty (5% for each |

|

00 |

|

7. |

Interest ( |

% per annum on any taxes unpaid by the due date) |

|

00 |

8. |

Total Amount Due (Add Lines 5, 6, and 7) |

|

00 |

|

9. |

Refund Due (Must complete and attach Report of Debts if claiming refund of $200 or more) |

|

00 |

|

FOR OFFICE USE ONLY Acct. # ____________________

Date Rec'd ________________

Amt. Rec'd $ _______________

Under the penalties of perjury, I declare that I have examined this report, and to the best of my knowledge and belief, it is

true, correct and complete.

Donor's

signature __________________________________________ Date ______________

Preparer's

signature __________________________________________ Date ______________

Address __________________________________________ Phone _____________

City/State _________________________________________ ZIP _______________

INTERNET

INSTRUCTIONS

WHO MUST FILE A RETURN:

Provided that the total value of all gifts during the calendar year exceeds the applicable exemption levels, the State Gift Tax Return must be filed upon transfer by gift by any person of the following property or any interest therein:

(a)When the transfer is from a resident of this state:

(1)Real property situated in Tennessee.

(2)Tangible personal property, except that which is actually situated outside of Tennessee.

(3)All intangible personal property.

(b)When the transfer is from a nonresident of this state:

(1)Real property situated in Tennessee.

(2)Tangible personal property which is actually situated in Tennessee.

(c)Property in which a person holds a qualifying income interest for life, which is included for taxation pursuant to

CLASSIFICATION OF DONEES:

CLASS A - Husband, wife, son, daughter, lineal ancestor, lineal descendant, brother, sister,

CLASS B - Any other relative, person, association, or corporation not specifically designated in Class A.

EXEMPTIONS:

(a)There shall be allowed against the net gifts made during any calendar year a maximum single exemption of ten thousand dollars ($10,000) against that portion of the net gifts going to donees of class A, and maximum single exemption of five thousand dollars ($5,000) against that portion of the net gifts going to the donees of Class B.

(b)In the event the aggregate net gifts for any calendar year exceed the allowable maximum single exemptions, the tax shall be applicable only to the extent that the gifts, (other than gifts of future interest in property) to each donee exceed the following amounts:

CLASS A - Gifts made before 2002 - The sum of $10,000

CLASS A - Gifts made in 2002 through 2005 - The sum of $11,000 CLASS A - Gifts made in 2006 through 2008 - The sum of $12,000 CLASS A - Gifts made in 2009 and after - The sum of $13,000 CLASS B - The sum of $3,000

"Net gifts" mean that total amount of gifts made during any calendar year less allowable deductions.

IF THE TOTAL VALUE OF ALL GIFTS MADE BY A PERSON DURING ANY CALENDAR YEAR DOES NOT EXCEED THE EXEMPTION LEVELS, NO GIFT TAX RETURN IS REQUIRED OF SUCH PERSON, UNLESS CONSENTING TO SPLIT GIFTS.

Item

Date of

Gift

SCHEDULE A

Description of Gift - See Instructions

(Include Name of Each Donee)

Value of Gift

Commissioner

Appraisal

TOTAL

NOTE: To facilitate the Class A and B computations, the items listed above should be segregated into the following categories: (1) gifts to spouse, (2) gifts to Class A donees other than the spouse, (3) gifts to Class B donees, and (4) gifts to charity, public, and similar uses.

DONEES

Name

Address

Age

Relationship

INTERNET

SCHEDULE B

COMPUTATION OF TAXABLE GIFTS

(1)Total gifts of donor (from Schedule A) ..................................................................................................

(2)

(3)Balance (Line 1 minus Line 2) .............................................................................................................

(4)Gifts of spouse to be included (from Line 2, Schedule B of spouse’s return) ....................................

(5)Total gifts (Line 3 plus Line 4) .............................................................................................................

(6)Deductions

(a)Total of items______ to ______ given to spouse .........................................................................

(b)Charitable, public and similar gifts .................................................................................................

(7)Total deductions [Line 6(a) plus Line 6(b)] ..........................................................................................

(8)Total gifts after deductions (Line 5 minus Line 7) ...............................................................................

(9)Total gifts to Class A donees ...............................................................................................................

(10)Total exclusions for the calendar year for each

Class A donee (except gifts of future interest) .....................................................................................

(11)Exemption: $10,000 less amount on Line 10 (if Line 10 is $10,000 or greater,

enter zero) Do not enter more than $10,000 on this line ..................................................................

(12)Total Class A exemptions (Line 10 plus Line 11) ...............................................................................

(13)Total taxable Class A gifts (Line 9 minus Line 12) ..............................................................................

(14)Total gifts to Class B donees (Line 8 minus Line 9) ...........................................................................

(15)Total exclusions not exceeding $3,000 for the calendar year

for each Class B donee (except gifts of future interest) .......................................................................

(16)Exemption: $5,000 less amount on Line 15 (if Line 15 is $5,000 or greater,

enter zero) Do not enter more than $5,000 on this line ....................................................................

(17)Total Class B exemptions (Line 15 plus Line 16) ...............................................................................

(18)Total taxable Class B gifts (Line 14 minus Line 17) ...........................................................................

(19)Total taxable gifts (Line 13 plus Line 18) .............................................................................................

________________________ |

1 |

________________________ |

2 |

________________________ |

3 |

________________________ |

4 |

________________________ |

5 |

________________________ |

6a |

________________________ |

6b |

________________________ |

7 |

________________________ |

8 |

________________________ |

9 |

________________________ |

10 |

________________________ |

11 |

________________________ |

12 |

________________________ |

13 |

________________________ |

14 |

________________________ |

15 |

________________________ |

16 |

________________________ |

17 |

________________________ |

18 |

________________________ |

19 |

SCHEDULE C

COMPUTATION OF TAX (For Gifts made after 1983)

(1) Class A taxable gifts from Schedule B, Line 13 |

|

|

AMOUNT |

RATE |

TAX |

(a)First $40,000, or part thereof = _______________________________ X 5.5% = _________________________________

(b)Next $200,000, or part thereof = ______________________________ X 6.5% = _________________________________

(c)Next $200,000, or part thereof = ______________________________ X 7.5% = _________________________________

(d)Amount over $440,000 .. ____________________________________ X 9.5% = _________________________________

(e) Total Class A tax (Add lines a through d and transfer to Page 1, Line 1) |

............... = |

_________________________________ |

(2) Class B taxable gifts from Schedule B, Line 18 |

|

|

AMOUNT |

RATE |

TAX |

(a)First $50,000, or part thereof = _______________________________ X 6.5% = _________________________________

(b)Next $50,000, or part thereof = _______________________________ X 9.5% = _________________________________

(c)Next $50,000, or part thereof = _______________________________ X 12.0% = _________________________________

(d)Next $50,000, or part thereof = _______________________________ X 13.5% = _________________________________

(e)Amount over $200,000 .. ____________________________________ X 16.0% = _________________________________

(f) Total Class B tax (Add lines a through e and transfer to Page 1, Line 2) |

= _________________________________ |

INTERNET

INSTRUCTIONS

DEDUCTION:

(a)Marital Deductions - There shall be allowed as a deduction in computing taxable gifts for a calendar year an amount equal to the gift(s) made by a donor to his/her spouse, provided they were married to each other at the time such gift(s) were made, and further provided that the property so transferred is not either of the following:

(1)Characterized as being a terminable interest; however, see (QTIP) election below.

(2)An interest in unidentified assets.

(b)Election to Deduct Qualified Terminable Interests - You may elect to claim a marital deduction for qualified terminable property or property interests. The election is irrevocable. The effect of the election is that the property (interest) will be treated as passing to the spouse and will not be treated as a nondeductible terminable interest. All of the other martial deduction requirements must still be satisfied before you may make this election.

Qualified terminable interest property is property that: (1 ) passes from the donor; and

(2) in which the spouse has qualifying income interest for life.

The spouse has a qualifying income interest for life if the spouse is entitled to all of the income for the property payable annually or at more frequent intervals, and during the spouse’s lifetime no person has a power to appoint any part of the property to any person other than the spouse.

In order to claim this election, you must check “yes” in the appropriate box on the face of the return. On Schedule A, you should group the property interests for which you made the election separately and mark them “Qualified Terminable Interest Property.” (QTIP)

(c)Charitable Deduction - There shall be allowed as a deduction in computing taxable gifts for a calendar year those gifts transferred to the United States, the State of Tennessee, or to any political subdivision thereof, any public institution herein for exclusively public purpose, or any corporation, society, association or trust therein, or in a state which grants a like exemption to such institutions in Tennessee formed for charitable, educational, scientific, or religious purposes.

DATES AND VALUATION:

The valuation of all property, real and personal, shall be appraised at its full and true value as of the date of the making of the gift.

INFORMATION REQUIRED:

1.REAL ESTATE - describe and identify each parcel so that it may be readily located for inspection and valuation. If formal appraisals are accomplished, attach a copy of the appraisal to the tax return. For city properties, state the street and number, ward, subdivision, block and lot identification numbers or letters. For rural properties, state the township, range, landmarks, number of acres and the road or street name upon which the property is located. For all improved properties, include a short statement of the type and description of the improvement(s). State the gross monthly rental for all parcels of real estate that are rented. Attach a copy of the lease for all leased parcels.

2.STOCKS AND BONDS - the description of stocks should indicate the number of shares, whether common or preferred price per share, exact name of corporation and, if not listed on a stock exchange, the address of the principal business office. If stock is listed, state the principal stock exchange upon which sold. The description of bonds should include quantity and denomination, name of the obligor, kind of bond, date of maturity, interest rate, and interest due dates. State the exchange upon which the bonds are listed, or if unlisted, the principal business office address of the company or municipality.

3.

4.NOTES AND MORTGAGES RECEIVABLE - indicate the face value, unpaid balance, date of the note or mortgage, date of maturity, name of maker, interest rate, interest dates, and a brief description of the property mortgaged.

5.ARTISTIC OR INTRINSICALLY VALUABLE GIFTS - attach a copy of the expert appraisal of the gift items.

6.GIFTS TO A TRUST - attach a copy of the trust agreement or governing instrument.

7.PARTIAL CONSIDERATION

8.POWERS OF APPOINTMENT - the exercise or release of a power of appointment may constitute a gift by the individual possessing such a power. In any case where such action has been taken, see

9.ACTUARIAL VALUATION OF FUTURE AND LlMITED ESTATES - computation of the values of any future, contingent or limited estate, income interest, or annuity must be attached to the tax return. Under

10.OTHER GIFTS - all other gifts should be fully described so that the value placed on the gift can be verified.

11.CONSENT OF SPOUSE - gifts made during the calendar year by the donor and spouse to third parties may be considered as being made

entirety, to perfect the election for gift splitting.

Document Data

| Fact Name | Description |

|---|---|

| Form Purpose | The INH 300 is used for filing a Tennessee state gift tax return or an amended return. |

| Due Date | The gift tax is due on April 15 of the year following the calendar year in which gifts were made. |

| Payee Information | Checks for gift tax payments should be made payable to the Tennessee Department of Revenue. |

| Marital Deduction | Allows for a deduction for gifts made to a spouse under certain conditions, aligning with I.R.C. §2523(f). |

| Governing Law | The form is governed by Tennessee Code Annotated (T.C.A.) §67-8-101(e) for certain property types and additional relevant state tax provisions. |

| Donor Categories | Classifies donees into Class A (close relatives) and Class B (others) for differential tax treatment. |

Detailed Guide for Using Tennessee Inh 300

Filling out the Tennessee INH 300 form is a crucial step for individuals who have made gifts that meet the specified criteria within the calendar year, ensuring compliance with state tax requirements. This guide simplifies the process into clear, actionable steps. Upon completion, the form should be submitted alongside the applicable payment to the Tennessee Department of Revenue by the due date to avoid penalties.

- Begin with the top section of the form by entering the calendar year of the gift.

- Fill in the county where the gift was made or owned.

- Enter the donor's Social Security Number in the designated spaces.

- Provide the name of the donor as well as their complete street address, including city, state, and ZIP code.

- If the donor is deceased, check the box provided and enter the date of death.

- Answer the questions related to terminable interest marital deduction and consent of spouse by checking "YES" or "NO" as appropriate.

- If consenting to spouse’s gifts, complete the details required in the consent section including the spouse's name, Social Security Number, marital status throughout the calendar year, and the spouse’s signature with date.

- Proceed to the "COMPUTATION OF TAX" section, rounding all amounts to the nearest whole dollar, and fill in Lines 1 through 9 as instructed by the calculation requirements.

- Sign and date the declaration at the bottom under penalty of perjury. If someone prepared the form on behalf of the donor, they must also sign and provide their address and phone number.

- Ensure all relevant schedules and documents (Schedule A for the description and value of gifts, Schedule B for computation of taxable gifts, and Schedule C for computation of tax) are completed and attached as necessary.

- Review the entire form for accuracy and completeness before mailing it with the appropriate tax payment or refund request to the Tennessee Department of Revenue, Andrew Jackson State Office Building, 500 Deaderick Street, Nashville, Tennessee 37242.

Once the form and any corresponding payment are submitted, the Tennessee Department of Revenue will process the return. Timely submission ensures compliance with state laws and avoids unnecessary penalties or interest on late payments. Keep a copy of the completed form and any correspondence for your records.

Important Questions on This Form

What is the Tennessee Inh 300 form?

The Tennessee Inh 300 form is a State Gift Tax Return document that must be filed with the Tennessee Department of Revenue. It is used to report the transfer of gifts by any person that exceed the exemption levels specified by the state law, including real property situated in Tennessee, tangible personal property unless situated outside of Tennessee, and all intangible personal property. For non-residents, it pertains to real property and tangible personal property situated within Tennessee. This form also includes sections for computing tax dues, electing marital deductions, and seeking consent for spouse gift-splitting.

When is the Tennessee Inh 300 due?

The due date for the Tennessee Inh 300 form is April 15 of the year following the calendar year in which the gifts were made. If the donor is unable to meet this deadline, payments must still be made to avoid penalties, and the preparer should ensure accuracy to prevent the need for an amended return. This deadline ensures that all gift transfers are accounted for in a timely manner, and the necessary taxes are collected by the state.

Who must file the Tennessee Inh 300 form?

- Residents who transfer real property in Tennessee, tangible personal property (unless situated outside Tennessee), or any intangible personal property.

- Non-residents who transfer real property in Tennessee or tangible personal property situated within Tennessee.

- Anyone transferring property in which a person holds a qualifying income interest for life, included for taxation pursuant to §67-8-101(e) Tennessee Code Annotated.

It is crucial for potential donors to understand these requirements to ensure compliance with state laws regarding gift taxation.

How are gift tax exemptions and deductions determined on this form?

The Tennessee Inh 300 form allows for exemptions and deductions under specific conditions:

- Exemptions: A maximum single exemption amount is allowed against the net gifts made during any calendar year - $10,000 for Class A donees (close family members) and $5,000 for Class B donees (others).

- Marital Deduction: Gifts made to a spouse may be deducted, assuming qualifications are met and the property transferred does not constitute a terminable interest or an interest in unidentified assets.

- Charitable Deduction: Gifts transferred to qualified governmental or nonprofit organizations for public, charitable, educational, scientific, or religious purposes are deductible.

Common mistakes

Filling out tax forms can be tricky, especially when it comes to something as specific as the Tennessee Inh 300 form, which deals with state gift taxes. It's easy to make a mistake, but being aware of common pitfalls can help you navigate this process more smoothly. Here are four mistakes people often make when completing this form.

Firstly, a common error occurs with the classification of donees. The Tennessee Inh 300 form distinguishes between Class A and Class B donees, with different tax implications for each. Class A donees include close relatives like spouses, children, and siblings, while Class B encompasses more distant relatives and unrelated recipients. Individuals frequently misclassify donees, leading to incorrect tax calculations. It's crucial to review the classification rules carefully to ensure each donee is correctly categorized, preventing potential issues with the Department of Revenue.

Another mistake involves incorrectly reporting the valuation of gifts. The form requires that all gifts, whether they're real estate, stocks, or personal items, be reported at their full and true value as of the gift's date. Often, individuals either underestimate the value of gifts to reduce the tax liability or simply make errors in valuation. Such mistakes can result in penalties or additional taxes if discovered upon review. It's advisable to obtain professional appraisals for high-value items and to consult the relevant guidelines for stocks and real estate valuation.

- Not utilizing the marital and charitable deductions correctly. The Inh 300 form offers specific deductions for gifts made to spouses (marital deductions) and gifts made to charitable organizations. Many filers overlook or misunderstand how to apply these deductions, missing opportunities to lower their taxable gift amounts. Understanding the criteria for these deductions can significantly affect the tax outcome.

- Skipping the consent of spouse section when applicable. For married individuals who make gifts to third parties, there's an option to treat these gifts as split equally between the spouse and the donor, which can affect the total gift tax calculation. Failing to complete this section when eligible means missing out on a tax strategy that could potentially lower the overall gift tax liability.

To avoid these common mistakes on the Tennessee Inh 300 form:

- Double-check the classification of your donees to ensure they are listed correctly.

- Ensure all gifts are valued accurately according to the guidelines provided, possibly seeking professional valuations when necessary.

- Review the instructions for marital and charitable deductions carefully, to make full use of available benefits.

- If married, consider the strategy of splitting gifts with your spouse and complete the consent section meticulously to ensure compliance.

By paying attention to these details, you can fill out the Inh 300 form accurately and efficiently, potentially saving time and reducing your tax liability. Remember, when in doubt, consulting with a tax professional can provide clarity and ensure you're making the most of the tax rules and deductions available to you.

Documents used along the form

When dealing with the Tennessee Inh 300 form, also known as the State Gift Tax Return, individuals might need to consider other documents and forms to ensure full compliance and accuracy in their filings. Understanding these documents can help navigate the complexities of gift taxation and make informed decisions about transfers of property or wealth.

- Real Estate Appraisal Report: This document provides a professional estimation of the value of real property, ensuring accurate reporting of the gift's value on the tax return.

- Stock Certificates: Represent ownership in a corporation. When gifting stocks, these certificates are required to establish the number of shares and the value of the gift.

- Bond Certificates: Essential for gifts involving government or corporate bonds, detailing the bond's issuer, face value, interest rate, and maturity date.

- Partnership Agreements: If a gift involves interest in a partnership, this document outlines the terms, confirming the donor's interest being transferred.

- Trust Documents: For gifts placed in a trust, these documents are crucial to describe the nature of the trust, the beneficiaries, and the terms under which the trust operates.

- Life Insurance Policies: In cases where life insurance is gifted, the policy document clarifies the value and terms of the gift.

- Personal Property Appraisals: Appraisals for high-value items like art, jewelry, or antiques ensure the gift's value is properly documented and taxed accordingly.

- Gift Deed: This legal document formalizes the transfer of real estate or other significant property gifts, detailing the donor, recipient, and the gift itself.

- Charitable Donation Receipts: For gifts to nonprofits or charitable organizations, receipts verify the transaction and may be necessary for tax deduction purposes.

The process of gifting, especially significant assets, requires careful planning and documentation to comply with Tennessee's tax laws. Each supporting document, from appraisal reports to trust agreements, plays a vital role in ensuring transparency, legality, and the accurate valuation of gifts. Keeping thorough and accurate records will not only facilitate the filing of the Tennessee Inh 300 form but also help in future financial planning and estate management.

Similar forms

The Tennessee Inh 300 form closely mirrors the Federal Gift Tax Return Form 709 due to their shared objective of documenting gifts that surpass the exempt amounts established by their respective governments. Both forms require detailed information about the donor and recipient(s), including Social Security numbers for domestic filings. They also necessitate a comprehensive listing of gifts provided over the year, breaking them down by type and recipient class, to accurately assess the applicable taxes after accounting for allowable exclusions and deductions. Additionally, each form incorporates provisions for gift splitting between spouses, enabling the division of gift amounts for tax purposes, highlighting their alignment in the facilitation of tax calculations related to gift distributions.

Another similar document is the Estate (and Generation-Skipping Transfer) Tax Return, IRS Form 706, which also interacts with gift tax rules. Though the Estate Tax Return primarily focuses on transfers of property at death, it shares similarities in its allowance for marital deductions, similar classifications of recipients, and requirements for valuation of assets. Both forms consider the impact of previous gifts on the tax implications of assets transferred either during life (Inh 300) or at death (Form 706), illustrating their interconnectedness in cumulative taxation matters.

The Unified Tax Credit for Estate and Gift Taxes form further intersects with the Tennessee Inh 300 form, as it directly influences the tax liabilities calculated for gifts. This credit signifies a crucial connection point by providing a unified framework that applies to both lifetime gifts and estate transfers, allowing individuals to utilize a portion of their exemption limit during their lifetime without immediate tax consequences, reflected in similar calculations and deductions claimed on the Inh 300 form.

State Inheritance Tax Returns from other states with inheritance tax systems, albeit varying in details and rates, bear resemblance to the Tennessee Inh 300 form in their foundational purpose of taxing transfers of wealth. Although the taxing authority and specific exemptions or rates may differ, the conceptual framework remains consistent: documenting transfers of wealth to determine tax obligations. These forms collectively seek to capture a snapshot of wealth transfer within a given period, ensuring that eligible transmissions are properly recorded and taxed in accordance with state law.

Likewise, the Intangible Personal Property Tax forms, applicable in some jurisdictions, echo the Inh 300 form's inclusion of intangible gifts in tax computations. While centering on a different asset class, these documents similarly require detailed listing of assets subject to their governance, underscoring the taxation approach across various types of property. This highlights the broader reach of taxation mechanisms as they encompass a wide spectrum of assets, including those not physically tangible.

The Qualified Terminal Interest Property (QTIP) Trust forms part of estate planning converge with the Inh 300 form through the QTIP election referenced within. Both legal instruments deal with the strategic passage and taxation of assets while considering marital deductions. This election is fundamental in optimizing tax liabilities associated with significant intergenerational wealth transfer, showcasing a strategic alignment in fostering tax-efficient asset transitions.

Marital Deduction forms filed with tax authorities to claim allowable deductions for gifts between spouses share parallels with the Tennessee Inh 300, particularly in its consent of spouse section. These documents play a pivotal role in the tax planning process by recognizing the special status of spousal transfers, thus permitting favorable tax treatment. Their emphasis on marital deduction reflects a common legal acknowledgment of the unique economic unit represented by married couples.

Finally, the Charitable Contribution Deduction forms, used to claim deductions for gifts made to qualified charities, resonate with aspects of the Inh 300 form that allow for reductions in taxable amounts through charitable giving. Both sets of documents underscore the tax code’s encouragement of philanthropy by providing avenues for donors to receive favorable tax consideration for charitable contributions, thus linking individual generosity with potential tax benefits.

Each of these documents, while individually tailored to specific aspects of tax law, collectively embodies the broader principles of wealth transfer taxation. From facilitating charitable giving to optimizing estate and gift tax implications, they underscore the extensive planning and reporting mechanisms individuals engage with in managing their fiscal responsibilities.

Dos and Don'ts

When completing the Tennessee INH 300 form, which is the State Gift Tax Return, attention to detail and adherence to the rules are critical. It's important to remember these do's and don'ts:

- Do ensure that all personal information is accurate, including the donor's name, Social Security Number, and address.

- Don't forget to check the box if the donor is deceased and provide the date of death.

- Do decide and indicate correctly whether you are electing to claim a marital deduction for gifts of qualified terminable interest property.

- Don't neglect the consent of spouse section if making joint gifts, ensuring that all parts are filled out and signed correctly.

- Do round all numbers to the nearest whole dollar as instructed on the form.

- Don't miscalculate the tax; follow the computation instructions carefully and ensure that all deductions and taxable amounts are entered correctly.

- Do attach any required documentation, such as appraisals for real estate or artistic items, as well as any documentation for trusts or non-listed corporations.

- Don't ignore the deadlines; the Tennessee Gift Tax is due April 15 of the year following the calendar year in which gifts were made.

- Do sign and date the form, ensuring that both the donor and the preparer (if applicable) provide their signatures.

- Don't send the form without reviewing it for completeness and accuracy to avoid any potential for delays or penalties.

By carefully following these guidelines, you can help ensure the process is as smooth and error-free as possible.

Misconceptions

When dealing with the Tennessee INH 300 form, State Gift Tax Return, several misconceptions frequently surface. Understanding these misconceptions is crucial for accurately filing and managing expectations regarding gift taxation in Tennessee. Below are seven common misconceptions clarified:

- Misconception #1: Filing is required for all gifts, regardless of amount. It's a common misunderstanding that any gift necessitates the filing of the INH 300 form. However, gifts only require reporting if their total value in a calendar year surpasses the applicable exemption levels. This illustrates the importance of understanding exemption thresholds before determining the necessity to file.

- Misconception #2: Only residents of Tennessee must file the INH 300 form. Both residents and non-residents may need to file this form. For residents, it pertains to a broad range of property types. For non-residents, the requirement applies to real property and tangible personal property situated in Tennessee, underscoring the form's reach beyond state residency.

- Misconception #3: Gift taxes are the same for all recipients. Tennessee distinguishes between Class A and Class B donees, significantly impacting the tax implications of gifts. Classifications affect exemptions and rates, highlighting the need for strategic gift planning.

- Misconception #4: Spousal consent is unnecessary in the filing process. When gifts are made to third parties by both spouses, consenting to split the gifts equally is an option that requires explicit consent on the form. This option, often overlooked, can influence the tax responsibilities and benefits for married couples.

- Misconception #5: The gift tax computation is standard for all gifts. Tax calculation varies significantly based on several factors, including the classification of the donee and the total amount of gifts. The process involves deductions, exemptions, and rates that differ between Class A and Class B donees, underscoring the complexity of accurately determining tax liability.

- Misconception #6: Marital deductions are straightforward. Marital deductions indeed offer opportunities for tax benefits but come with restrictions, such as the exclusion of terminable interests and unidentified asset interests. Additionally, electing to claim a deduction for qualified terminable interest property (QTIP) is irrevocable, requiring careful consideration and understanding of its implications.

- Misconception #7: Any property valuation method is acceptable. For gift tax purposes, the valuation of property must reflect its "full and true value" as of the date of the gift. Specific instructions for different types of property ensure that valuation is not only accurate but also conforms to the guidelines set forth by the Tennessee Department of Revenue. Adhering to these requirements is essential for compliance and accurate tax calculation.

Clearing up these misconceptions is critical for anyone involved in the transfer of gifts in Tennessee. Accurate understanding and compliance with the INH 300 form instructions ensure that donors can navigate the complexities of state gift taxation effectively.

Key takeaways

Understanding the Tennessee INH 300 form is crucial for taxpayers looking to report and potentially pay the state gift tax. Below are key takeaways that can help individuals navigate through the complexities of this tax form:

- Individuals must file the INH 300 form if they have transferred property by gift exceeding certain exemption levels during the calendar year, including real estate in Tennessee, tangible personal property within the state (excluding property situated outside Tennessee for residents), or any intangible personal property.

- The form serves to calculate and report gift taxes due to the Tennessee Department of Revenue for gifts made within a calendar year, with taxes due by April 15 of the following year.

- A unique feature of the Tennessee gift tax involves the classification of donees into two categories: Class A (close relatives like spouses, children, siblings) and Class B (other recipients), as this classification affects exemption amounts and tax rates.

- Exemptions are in place to reduce the taxable value of gifts; for instance, there are specific exemptions amounts for gifts to Class A and Class B donees ($10,000 and $5,000 respectively), which are deducted from the net gifts made during the year.

- The form allows for the application of marital deductions and elections to treat certain gifts to a spouse differently in cases of qualified terminable interest property (QTIP), potentially lowering the taxable gift amount.

- Charitable gifts made to approved institutions may also be deducted, which underscores the benefit of philanthropic gifts in estate planning and tax minimization.

- Determination of the fair market value of gifts at the time of transfer is required for tax purposes, and the form requests detailed information about each gift, including appraisals for real estate and art, and financial statements for business interests.

- The consent of a spouse feature allows the splitting of gift amounts between spouses for tax purposes, a strategy that can significantly impact the taxable estate and the utilization of exemptions.

- Penalties and interest apply for late payments or underpayments of the gift tax, highlighting the importance of accurate calculation and timely submission of the form.

By taking a methodical approach to filling out the INH 300 form and leveraging the available deductions and exemptions, individuals can effectively manage their gift tax liability in Tennessee.

Create Other Documents

Llc in Tennessee Cost - Failure to properly file an amendment can lead to discrepancies in legal documents, affecting contracts, and potentially leading to legal misunderstandings.

Workers Comp Exemption Tn - Structured to ensure all relevant medical opinions are considered in workers' compensation cases.