Get Tennessee Fae 173 Template in PDF

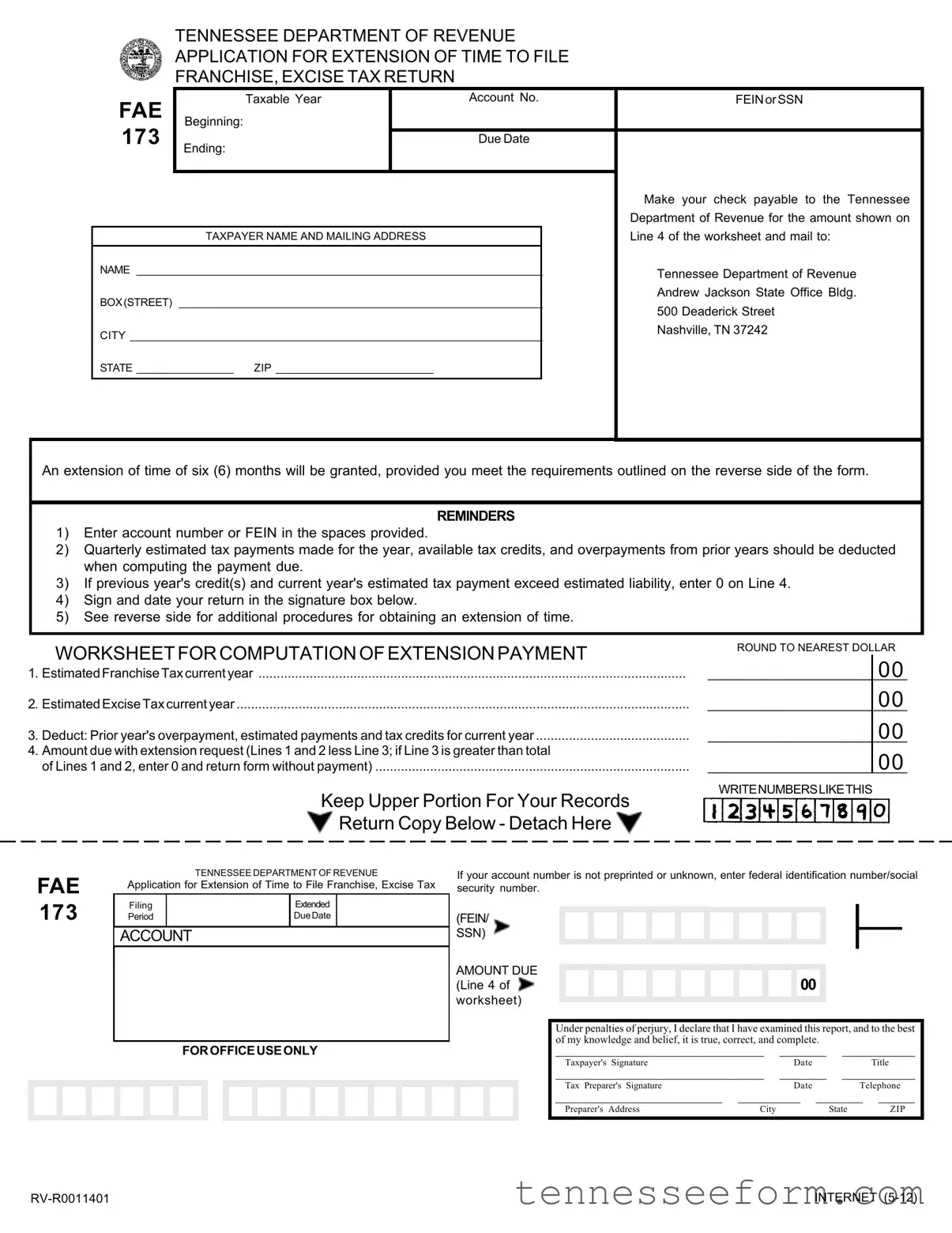

The Tennessee Fae 173 form is an essential document for businesses operating within Tennessee, facilitating an extension of time to file their Franchise and Excise Tax Returns. This application is intricately designed to assist taxpayers in navigating their tax obligations efficiently, aimed at those who require additional time beyond the standard filing date. By adhering to the guidelines provided on the form, taxpayers can secure a six-month extension, provided specific prerequisites outlined on the form's reverse are met. Critical components include accurately entering the taxpayer's account number or Federal Employer Identification Number (FEIN) or Social Security Number (SSN), calculating and reporting estimated taxes due, and making any necessary payments to the Tennessee Department of Revenue. Key reminders on the form guide taxpayers through the calculation of their extension payment, emphasizing the deduction of quarterly estimated tax payments, available tax credits, and overpayments from the previous years. Furthermore, the form sets forth clear instructions for the submission process, including payment modalities and deadlines, while also highlighting penalties for non-compliance. Through its comprehensive design, the FAE 173 form serves as a vital tool for maintaining tax compliance within Tennessee, offering a structured path to securing an extension for filing Franchise and Excise Tax Returns.

Document Preview Example

TENNESSEE DEPARTMENT OF REVENUE

APPLICATION FOR EXTENSION OF TIME TO FILE

FRANCHISE, EXCISE TAX RETURN

|

FAE |

Taxable Year |

|

Account No. |

FEINorSSN |

|

|

Beginning: |

|

|

|

|

|

|

173 |

Ending: |

|

Due Date |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

Make your check payable to the Tennessee |

|

|

|

|

|

|

|

|

|

|

|

|

|

Department of Revenue for the amount shown on |

|

|

TAXPAYER NAME AND MAILING ADDRESS |

|

|

Line 4 of the worksheet and mail to: |

|

|

|

|

|

|||

|

NAME ___________________________________________________________________ |

|

Tennessee Department of Revenue |

|||

|

|

|

|

|

|

|

|

BOX(STREET) ____________________________________________________________ |

|

Andrew Jackson State Office Bldg. |

|||

|

|

500 Deaderick Street |

||||

|

|

|

|

|

|

|

|

CITY ____________________________________________________________________ |

|

Nashville, TN 37242 |

|||

|

|

|

||||

|

STATE ________________ ZIP __________________________ |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

An extension of time of six (6) months will be granted, provided you meet the requirements outlined on the reverse side of the form.

REMINDERS

1)Enter account number or FEIN in the spaces provided.

2)Quarterly estimated tax payments made for the year, available tax credits, and overpayments from prior years should be deducted when computing the payment due.

3)If previous year's credit(s) and current year's estimated tax payment exceed estimated liability, enter 0 on Line 4.

4)Sign and date your return in the signature box below.

5)See reverse side for additional procedures for obtaining an extension of time.

WORKSHEETFORCOMPUTATIONOFEXTENSIONPAYMENT

1.EstimatedFranchiseTaxcurrentyear .....................................................................................................................

2.EstimatedExciseTaxcurrentyear ............................................................................................................................

3.Deduct: Prior year's overpayment, estimated payments and tax credits for current year ..........................................

4.Amount due with extension request (Lines 1 and 2 less Line 3; if Line 3 is greater than total

of Lines 1 and 2, enter 0 and return form without payment) ......................................................................................

Keep Upper Portion For Your Records

Return Copy Below - Detach Here

Return Copy Below - Detach Here

ROUND TO NEAREST DOLLAR

00

___________________________00

00

00

WRITENUMBERSLIKETHIS

FAE

173

TENNESSEE DEPARTMENT OF REVENUE

Application for Extension of Time to File Franchise, Excise Tax

Filing |

|

Extended |

|

Period |

|

DueDate |

|

|

|

|

|

ACCOUNT

FOROFFICEUSEONLY

If your account number is not preprinted or unknown, enter federal identification number/social security number.

(FEIN/

SSN)

AMOUNT DUE

(Line 4 of  00 worksheet)

00 worksheet)

Under penalties of perjury, I declare that I have examined this report, and to the best of my knowledge and belief, it is true, correct, and complete.

________________________________________ |

_________ |

______________ |

|||

Taxpayer's Signature |

|

Date |

|

|

Title |

________________________________________ |

_________ |

______________ |

|||

Tax Preparer's Signature |

|

Date |

|

Telephone |

|

________________________________ |

____________ |

_________ |

_______ |

||

Preparer's Address |

City |

|

|

State |

ZIP |

INTERNET |

PROCEDURES FOR OBTAINING AN EXTENSION OF TIME

NOTE: This form can be filed electronically free of charge at apps.tn.gov/fnetax

1.Required Payment:

•Payments equal to the lesser of 100% of the prior year tax liability or 90% of the current year tax liability must be made by the original due date.

•If the prior tax year covered less than twelve months, the prior period tax must be annualized when calculating the required payment.

•If there was no liability for the prior year, the required payment is $100.

•Quarterly estimated payments, prior year overpayments and any other

2.Extension requests should be made as follows:

•If you are not required to make a payment because you have already made sufficient payments, either the state form or a copy of your federal extension request can be submitted. The form or copy of the federal extension need not be filed on the original due date of the return. Instead, it should be attached to the return itself, which is to be filed on or before the extended due date.

•If a payment is needed to meet the payment requirement and you do not file your federal return as part of a consolidated group, either the state form or a copy of your federal extension request can be submitted. In this case, the form or copy of your federal extension must be filed with the extension payment on or before the original due date of the return.

•If a payment is required and you file your federal return as part of a consolidated group, you must use this form or file an extension request electronically. This form or the electronic version of this form must be filed with the extension payment on or before the original due date of the return.

3.Other important information:

•Penalty will be computed as though no extension had been granted if, (1) the amount paid on or before the original due date does not satisfy the payment requirement indicated above, or (2) the return is not filed by the extended due date.

•An approved extension does not affect interest. Interest will be computed on any unpaid tax from the original due date of the return until the date the tax is paid.

Document Data

| Fact | Detail |

|---|---|

| Form Name | Tennessee Department of Revenue Application for Extension of Time To File Franchise, Excise Tax Return FAE 173 |

| Form Purpose | To apply for an extension of six (6) months to file the Franchise, Excise Tax Return |

| Payment Requirements | Payment must be the lesser of 100% of the prior year tax liability or 90% of the current year tax liability to qualify for the extension. |

| Minimum Payment | If there was no liability in the prior year, the required minimum payment is $100. |

| Calculations for Extension Payment | Estimated taxes for the current year minus any quarterly estimated payments, prior year's overpayments, and tax credits. |

| Due Date for Extension Payment | Payments must be made by the original due date of the return to qualify for the extension. |

| Electronic Filing | The form FAE 173 can be filed electronically free of charge at apps.tn.gov/fnetax |

| Interest on Unpaid Tax | Interest is computed on any unpaid tax from the original due date of the return until the tax is paid. |

| Penalty for Non-compliance | A penalty is applied as though no extension had been granted if the required payment is not made or the return is not filed by the extended due date. |

| Requirements for Using Federal Extension | A copy of the federal extension request can substitute for the state form if no payment is required or a standalone payment is not being made as part of a consolidated group. |

| Special Note for Consolidated Filers | Those filing as part of a consolidated group and needing to make a payment must use the FAE 173 form or file an extension request electronically by the original due date of the return. |

Detailed Guide for Using Tennessee Fae 173

Fulfilling the requirements for an extension to file the franchise and excise tax return in Tennessee is a straightforward process, designed to provide taxpayers with additional time if needed. This particular form, FAE 173, is used to formally request an extension of six months from the Tennessee Department of Revenue. It's essential to accurately complete this form and submit any required payment to avoid penalties and interest on unpaid taxes. The steps listed below guide you through filling out the form, calculating any payments due, and ensuring that your extension request is properly filed.

- Enter the taxable year at the top of the form, specifying both the beginning and ending dates.

- Provide the account number, if known. If not, enter the Federal Employer Identification Number (FEIN) or Social Security Number (SSN) as applicable.

- Fill in the taxpayer name and mailing address, including the box or street, city, state, and ZIP code in the designated spaces.

- On the worksheet for the computation of extension payment:

- Estimate the current year's franchise and excise tax and enter these amounts on Lines 1 and 2 respectively.

- Deduct any available credits, including prior year’s overpayment, estimated payments for the current year, and any tax credits on Line 3.

- Calculate the amount due with your extension request by subtracting Line 3 from the total of Lines 1 and 2. Enter this amount on Line 4. If the result is less than 0, enter 0 and no payment is due with the form.

- Make your check payable to the Tennessee Department of Revenue for the amount shown on Line 4 of the worksheet.

- Sign and date the form in the designated signature area, including the title if applicable. A tax preparer completing the form on behalf of a taxpayer should also sign and date, including their telephone number and address.

- Mail the completed form and any required payment to: Tennessee Department of Revenue, Andrew Jackson State Office Bldg., 500 Deaderick Street, Nashville, TN 37242.

By closely following these steps, taxpayers can ensure their extension request is processed efficiently. It's important to remember that obtaining an extension to file does not extend the time to pay any taxes due. To avoid penalties and interest, accurately calculate and remit any owed amount with your extension request.

Important Questions on This Form

What is the Tennessee FAE 173 form?

The Tennessee FAE 173 form is an application for businesses to request an extension of time to file their Franchise and Excise Tax Returns. It is used by the Tennessee Department of Revenue to allow companies an additional six months to prepare their returns adequately, ensuring they can compile all necessary information and payments. This form is crucial for businesses that need extra time to accurately calculate their taxes and avoid errors in their filings.

How do I calculate the amount due with my extension request?

To calculate the amount due with your extension request on the Tennessee FAE 173 form, you should follow these steps outlined in the form's worksheet:

- Estimate your current year's Franchise and Excise Tax.

- Deduct any prior year's overpayments, estimated payments, and tax credits for the current year from this estimate.

- The result is the amount due. If your deductions exceed your estimated taxes, you will enter 0 and return the form without payment.

Can I file the Tennessee FAE 173 form electronically?

Yes, the Tennessee Department of Revenue encourages filers to submit the FAE 173 form electronically for faster processing and convenience. Businesses can file this extension request form online at no charge through the official Tennessee Department of Revenue website's electronic filing system. This method allows for an immediate confirmation of submission and helps reduce paper waste.

What are the payment requirements for filing an extension request?

The payment requirements for filing an extension request with the Tennessee FAE 173 form are specific and must be adhered to for the extension to be granted:

- Payments must be equal to the lesser of 100% of the prior year tax liability or 90% of the current year tax liability. This payment must be made by the original due date of the return.

- If the business had no liability in the prior year, a minimum payment of $100 is required.

- Prior year's overpayments, quarterly estimated payments, and any other pre-payments should be deducted to calculate the required payment for the extension.

Common mistakes

When filing the Tennessee FAE 173 form, an Application for Extension of Time to File Franchise, Excise Tax Return, individuals often encounter a variety of common pitfalls. These mistakes can lead to delays, penalties, or even the rejection of an extension request. Recognizing and avoiding these errors can streamline the process, ensuring compliance with Tennessee tax laws.

- Incorrect or Incomplete Taxpayer Information: Failing to include complete taxpayer name, mailing address, account number, or Federal Employer Identification Number (FEIN) / Social Security Number (SSN). This basic information is crucial for the Department of Revenue to process the form accurately.

- Errors in Payment Calculation: Not correctly calculating the amount due with the extension request can lead to underpayment or overpayment. It's important to carefully follow the worksheet provided for computation of extension payment to ensure that prior year's overpayments, estimated payments, and tax credits for the current year are accurately deducted.

- Not Submitting Required Payment: If a payment is needed to meet the extension requirements, not submitting this payment with the form can invalidate the extension request. The required payment must be the lesser of 100% of the prior year tax liability or 90% of the current year tax liability.

- Overlooking Signature and Date: The form requires a signature and date to certify that the information provided is true, correct, and complete under penalties of perjury. Missing signatures or dating can result in the form being returned or not accepted.

In addition to these errors, individuals often miss several other details that are critical for the successful filing of the Tennessee FAE 173 form:

- Not rounding numbers to the nearest dollar can create issues in processing the form.

- Failing to keep the upper portion for personal records may result in difficulties if verification of the submission is required.

- Incorrectly assuming an extension of time to file also extends the time for payment. It is essential to understand that interest will still be computed on any unpaid tax from the original due date of the return until the tax is paid.

- Not considering the specific requirements for those who file their federal return as part of a consolidated group, which requires using the Tennessee FAE 173 form or filing an extension request electronically.

- Overlooking the procedures on the reverse side of the form, which provide important details about obtaining an extension of time, including the necessity of attaching the state form or a copy of your federal extension to the return if sufficent payments have already been made.

By paying close attention to these common mistakes and ensuring all parts of the FAE 173 form are completed accurately and thoroughly, taxpayers can avoid unnecessary stress and complications. Remembering to read all instructions carefully and review the form before submission can greatly decrease the likelihood of encountering issues with the Tennessee Department of Revenue.

Documents used along the form

When filing the Tennessee FAE 173 form, an Application for Extension of Time to File Franchise, Excise Tax Return, there are a handful of other forms and documents that businesses often need to have ready. Whether it's to ensure compliance with tax laws, facilitate accurate calculations of taxes owed, or to document tax payments already made, integrating these documents can streamline the filing process remarkably.

- Form FAE 170 - Franchise and Excise Tax Return: This is the primary tax return form for businesses subject to franchise and excise taxes in Tennessee. It’s where you report your taxes due for the year. Filing an extension with Form FAE 173 does not exempt you from eventually completing this form with all pertinent financial details of the business year.

- Form FAE 174 - Franchise & Excise Tax Annual Exemption Renewal: For entities claiming exemption from these taxes, this form is necessary to maintain that status. It confirms the eligibility for exemption in the upcoming tax year.

- Form FAE 183 - Application for Registration/Re-registration: This form is for businesses starting in Tennessee or those needing to update their registration details. Accurate registration is crucial for tax identification and compliance.

- Schedule N - Net Worth Schedule: Attached to the Franchise Tax Return, this schedule details a company’s net worth, which is essential for calculating the franchise tax.

- Form BUS415-3 - Quarterly Estimated Tax Payment Voucher: Businesses expecting to owe more than $5,000 in excise tax must make quarterly payments. These vouchers are used to submit estimated tax payments throughout the year.

- Request for Penalty Waiver - If a business faces specific hardships that lead to late payments or filings, this document can be submitted to request a waiver for penalties incurred. The documentation must outline the cause and provide supporting evidence.

Each of these forms and documents plays a vital role in the tax filing process for businesses in Tennessee. By understanding what is required and preparing these documents in advance, businesses can ensure a smoother filing process, avoid penalties for late submissions, and maintain compliance with state tax regulations. Importantly, these forms collectively provide a comprehensive view of a business's financial and tax obligations, facilitating strategic planning and financial management.

Similar forms

The Tennessee FAE 173 form, used for requesting an extension to file franchise and excise taxes, shares similarities with the Federal Form 7004. The Federal Form 7004 is the "Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns." Both forms serve the purpose of granting businesses additional time to file their tax returns, with both requiring an estimation of taxes owed and any payments that have already been made. This aligns with the FAE 173 form's requirement for estimated taxes to determine the extension payment.

Another document resembling the Tennessee FAE 173 form is the IRS Form 4868, which is the "Application for Automatic Extension of Time to File U.S. Individual Income Tax Return." Although the 4868 form is for individuals rather than businesses, it also allows taxpayers to get a six-month extension on filing their tax returns, much like the FAE 173 does for franchise and excise taxes in Tennessee. Both documents necessitate the calculation of estimated tax liability and payments made to date to determine if an additional payment is required with the extension request.

The Tennessee FAE 173 form also mirrors the state-specific extension requests for other types of taxes, such as the California Form 3519, used for individuals to request an extension to file their personal income tax returns. Similar to the FAE 173, taxpayers must estimate their tax liability and report any payments made throughout the year. This helps in determining if additional payment is necessary upon filing the extension request, emphasizing the taxpayer's responsibility to approximate due taxes.

Furthermore, the UK's HM Revenue and Customs (HMRC) form SA303 is akin to the FAE 173 form in that it allows UK taxpayers to request an extension for filing self-assessment tax returns. While the SA303 caters to a different tax system and jurisdiction, it shares the principle of providing taxpayers additional time to file accurate returns, paralleling the objective of the FAE 173 form's extension for franchise and excise taxes in Tennessee.

On a state level, the New York Form IT-370, "Application for Automatic Six-Month Extension of Time to File for Individuals," parallels the Tennessee FAE 173 form by extending filing deadlines. Both forms require an estimation of the total tax liability and account for payments made throughout the year. This process enables taxpayers to remain compliant while affording them extra time to gather necessary documentation for filing.

Another document similar to the Tennessee FAE 173 form is the Texas Franchise Tax Extension Request, which businesses operating in Texas must use to request extra time to file their franchise tax reports. Like the FAE 173, the Texas extension stipulates that an estimation of owed taxes and a review of payments already made are necessary steps in the extension process, reinforcing the taxpayer's obligation to maintain accurate financial records.

The IRS Form 8809, "Application for Extension of Time to File Information Returns," also shares a resemblance to Tennessee's FAE 173 form, though it targets information returns rather than tax returns. Both forms are instrumental in requesting additional time from the respective tax authority, requiring detailed knowledge of financial conditions and obligations due within the extension period.

State of New Jersey’s Division of Taxation Form NJ-630 is used to apply for an extension to file the state income tax return, much like the Tennessee FAE 173 form for franchise and excise taxes. Both forms do not eliminate the taxpayer's obligation to estimate and pay any owed taxes by the original due date, underlining the principle of provisional tax payment within extension applications across different tax jurisdictions.

The Colorado Department of Revenue Tax Form DR 0158-I, serving as an extension request for filing individual income tax returns, parallels the FAE 173 in guiding taxpayers through an extension process. While catering to different taxes, both documents emphasize the necessity of estimating whether taxes owed have been fully paid by the due date to avoid penalties, showcasing a common theme in extension requests nationally.

Last but not least, the Virginia Form 760IP, used for requesting an automatic six-month filing extension for individual income tax returns, resembles the Tennessee FAE 173 form in purpose and requirement. Although one addresses individual income and the other franchise and excise taxes, both necessitate an accurate estimation of taxes due and consider payments already made, highlighting the universal tax principle of balancing payments with liabilities during extension periods.

Dos and Don'ts

When it comes to filling out the Tennessee FAE 173 form, an Application for Extension of Time to File Franchise, Excise Tax Return, there are important do’s and don’ts that can help streamline the process and avoid potential issues. This list combines both to ensure you tackle this task correctly.

- Do enter your account number or Federal Employer Identification Number (FEIN) or Social Security Number (SSN) in the spaces provided. This is crucial for your form to be processed correctly.

- Do deduct quarterly estimated tax payments, available tax credits, and any overpayments from prior years when computing the payment due. This helps in accurately determining the amount you need to pay with your extension request.

- Do sign and date your return in the designated signature box. An unsigned form could be considered invalid.

- Do make your check payable to the Tennessee Department of Revenue for the amount shown on Line 4 of the worksheet. Accurate payment ensures that your extension request is processed without delays.

- Do keep the upper portion of the form for your records. It's important to have a copy of what you've submitted for future reference.

- Don’t enter a value on Line 4 of the worksheet if your deductions (prior year's credits and current year's estimated tax payment) exceed the estimated liability; instead, enter 0 and return the form without payment.

- Don’t ignore the requirements listed on the reverse side of the form for obtaining an extension of time. These guidelines are there to help ensure you complete the process correctly.

- Don’t delay in sending your form and payment to the provided address of the Tennessee Department of Revenue in Nashville. Timeliness is key to avoiding penalties and interest.

- Don’t overlook the option to file this form electronically free of charge, which might offer a more convenient and faster submission method.

Being attentive to these dos and don’ts will facilitate a smoother process in requesting an extension of time for filing your Franchise, Excise Tax Return. Ensuring proper completion and timely submission of the Tennessee FAE 173 form not only complies with state requirements but also positions you favorably in managing your taxes effectively.

Misconceptions

Among the formalities and provisions linked to tax regulations in Tennessee, particularly regarding the FAE 173 form, or the Application for Extension of Time to File Franchise, Excise Tax Return, several misunderstandings commonly arise. Identifying and clarifying these misconceptions can provide clarity and ease the apprehension often associated with tax obligations.

Misconception 1: An extension grants additional time to pay taxes. It’s broadly misunderstood that filing the FAE 173 form provides taxpayers with extra time to settle their tax liabilities. In truth, the extension solely applies to the filing of returns. Taxpayers are required to estimate and remit the amount due (as determined by the worksheet on the form) by the original due date. Failure to meet this payment requirement may result in penalties and interest accruing from the due date.

Misconception 2: Prior year’s tax liability is irrelevant. Another common oversight is neglecting the role of the previous year's tax liability in determining the minimum payment due with the extension request. The form stipulates that the extension payment must be the lesser of 100% of the prior year’s liability or 90% of the current year’s liability. This rule underscores the relevance of prior year figures in calculating the extension payment.

Misconception 3: Overpayment and credits need not be reported on the extension form. A prevalent misconception is that details concerning the taxpayer's overpayment from the prior year, estimated payments, and tax credits do not influence the extension process. Conversely, these amounts are crucial for determining the accurate extension payment. They must be deducted on Line 3 of the worksheet to ascertain the appropriate amount due with the extension request.

Misconception 4: Filing the extension form is optional if no payment is due. Even if taxpayers believe no additional payment is due with their extension, some presume the FAE 173 form need not be filed. However, the form serves as a notification to the Department of Revenue about the taxpayer's intention to file after the original deadline. Submitting the form (or a copy of the federal extension) is imperative to prevent potential misunderstanding and penalties, especially if the submission deadline is misunderstood.

Understanding these nuances of the FAE 173 form helps taxpayers navigate the complexities of franchise and excise tax requirements in Tennessee. By elucidating these misconceptions, taxpayers can more confidently manage their filing obligations, minimize exposure to penalties, and ensure compliance with state tax laws.

Key takeaways

Understanding the process and requirements for filing the Tennessee FAE 173 form, an Application for Extension of Time to File Franchise, Excise Tax Return, is crucial for businesses operating within the state. Here are key takeaways to ensure compliance and accuracy during this process:

- The form allows for a six-month extension beyond the original due date for filing your franchise and excise tax returns, provided certain conditions are met.

- It is important to correctly enter either your account number or your Federal Employer Identification Number (FEIN) or Social Security Number (SSN) in the designated spaces to ensure proper processing of your extension request.

- When calculating the payment due with the extension request, you must deduct any quarterly estimated tax payments, available tax credits, and overpayments from prior years from the current year’s estimated franchise and excise tax.

- If your deductions (previous year's credits and current year's estimated payments) exceed your estimated liability for the current year, you should enter "0" on Line 4 of the worksheet and return the form without payment.

- Be sure to sign and date the return in the signature box provided. This is a declaration under the penalties of perjury that to the best of your knowledge, the information provided is true, correct, and complete.

- Payments made should be equal to the lesser of 100% of the previous year's tax liability or 90% of the current year's tax liability and must be submitted by the original due date to avoid penalties.

- The form or a copy of your federal extension request can be submitted in cases where no payment is due with the extension because sufficient payments have already been made. However, if a payment is required to meet the minimum payment criterion, the form or federal extension must be filed with the payment by the original due date.

- An extension of time to file does not grant an extension for payment due. Interest will accrivate on any unpaid taxes from the original due date until the tax is paid in full. Additionally, failure to pay the required amount by the original due date may result in penalties, computed as though no extension had been granted.

Note: The Tennessee Department of Revenue offers electronic filing for the FAE 173 form, which can streamline the process and ensure timely submission. Always consult the latest guidance and resources available on the Tennessee Department of Revenue's website or consult with a tax professional for the most accurate and up-to-date advice.

Create Other Documents

Tennessee Llc Formation - Instrument for declaring a partnership as an LLP in Tennessee, with specifications for immediate or delayed registration effectiveness.

Tennessee Bus 415 - The BUS 415 allows for deductions based on interstate commerce, cash discounts, and repossessions.