Get Tennessee Fae 172 Template in PDF

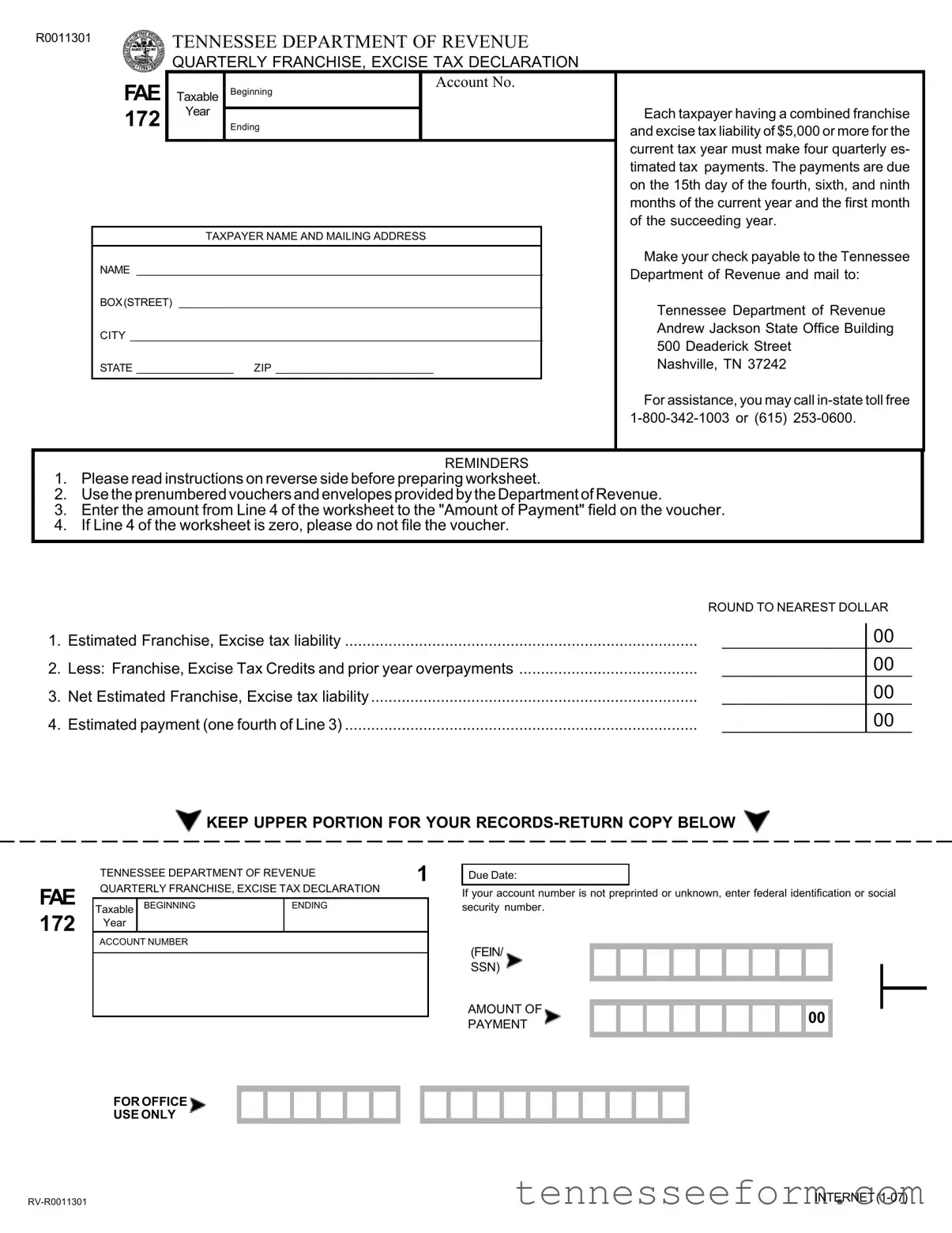

The Tennessee FAE 172 form is an essential document managed by the Tennessee Department of Revenue, designed for taxpayers who must declare and pay their franchise and excise tax quarterly. This requirement kicks in for those with a combined tax liability of $5,000 or more in the current tax year. The form serves as a means to calculate and declare the estimated taxes due across four specific periods: the 15th day of the fourth, sixth, and ninth months of the current year, and the first month of the following year. Its structured design aids taxpayers in determining their estimated tax liability, taking into account any applicable credits and previous overpayments. Compliance with this system involves meticulous attention to the calculation guidelines provided, adherence to the payment schedule to avoid penalties, and making use of the prenumbered vouchers and envelopes for submitting these payments. Furthermore, taxpayers are cautioned against underestimation, as doing so may result in penalties and interest charges, calculated from each installment's due date until the owed amount is paid in full. Overall, the FAE 172 form is a critical component for businesses operating within Tennessee, ensuring that they meet their tax obligations in a systematic and timely manner.

Document Preview Example

R0011301 |

TENNESSEE DEPARTMENT OF REVENUE |

|

QUARTERLY FRANCHISE, EXCISE TAX DECLARATION |

FAE |

|

|

ACCOUNT NO. |

Taxable Beginning |

|||

172 |

Year |

Ending |

|

|

|

||

TAXPAYER NAME AND MAILING ADDRESS |

|

NAME ___________________________________________________________________ |

|

BOX(STREET) ____________________________________________________________ |

|

CITY ____________________________________________________________________ |

|

STATE ________________ |

ZIP __________________________ |

Each taxpayer having a combined franchise and excise tax liability of $5,000 or more for the current tax year must make four quarterly es- timated tax payments. The payments are due on the 15th day of the fourth, sixth, and ninth months of the current year and the first month of the succeeding year.

Make your check payable to the Tennessee Department of Revenue and mail to:

Tennessee Department of Revenue

Andrew Jackson State Office Building

500 Deaderick Street

Nashville, TN 37242

For assistance, you may call

REMINDERS

1.Please read instructions on reverse side before preparing worksheet.

2.UsetheprenumberedvouchersandenvelopesprovidedbytheDepartmentofRevenue.

3.Enter the amount from Line 4 of the worksheet to the "Amount of Payment" field on the voucher.

4.If Line 4 of the worksheet is zero, please do not file the voucher.

|

|

ROUND TO NEAREST DOLLAR |

|

|

00 |

1. |

Estimated Franchise, Excise tax liability |

______________________ |

|

|

00 |

2. |

Less: Franchise, Excise Tax Credits and prior year overpayments |

______________________ |

|

|

00 |

3. |

Net Estimated Franchise, Excise tax liability |

______________________ |

|

|

00 |

4. |

Estimated payment (one fourth of Line 3) |

______________________ |

KEEP UPPER PORTION FOR YOUR

KEEP UPPER PORTION FOR YOUR

FAE 172

TENNESSEE DEPARTMENT OF REVENUE |

1 |

||

QUARTERLY FRANCHISE, EXCISE TAX DECLARATION |

|

||

|

|

|

|

Taxable |

BEGINNING |

ENDING |

|

Year |

|

|

|

|

|

|

|

ACCOUNT NUMBER |

|

|

|

|

|

|

|

|

|

|

|

Due Date:

If your account number is not preprinted or unknown, enter federal identification or social security number.

(FEIN/

SSN)

AMOUNT OF |

|

|

|

|

|

|

|

|

00 |

PAYMENT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FOR OFFICE

USE ONLY

|

INSTRUCTIONS

1.WHO MUST MAKE ESTIMATED TAX PAYMENTS: Taxpayers who expect a franchise, excise tax liability of $5,000 or more for the current tax year must file a declaration of their franchise, excise tax for the taxable year and make quarterly payments.

2.WHEN TO MAKE PAYMENTS: Quarterly payments of the estimated franchise, excise tax are to be made as follows:

1st payment - The 15th day of the 4th month of the current taxable year. 2nd payment - The 15th day of the 6th month of the current taxable year. 3rd payment - The 15th day of the 9th month of the current taxable year.

4th payment - The 15th day of the 1st month of the subsequent taxable year.

3.REQUIREDPAYMENT: Theminimumamountofeachquarterlypaymentshallbethelesserof:(a)25%ofthecombinedfranchise, excise tax shown on the tax return for the preceding tax year, annualized if the preceding tax year was for less than twelve (12) months; or (b) 25% of 100% of the combined franchise, excise tax liability for the current tax year.

4.PENALTYANDINTEREST: Penaltyattherateof5%permonth,upto25%,andinterestatthecurrentrateperannumareimposed upon any quarterly installment which is late or underpaid. Penalty and interest are computed from the due date of the installment to the date paid or until the fifteenth day of the fourth month following the close of the taxable year.

5.WHICH FORM TO USE: All franchise, excise tax payments must be accompanied by the Tennessee Estimated Franchise, ExciseTaxDeclarationform.Ifyoureceivedapreaddressedpacket,pleaseusetheprenumberedvouchersandenvelopessupplied with the packet. This will help expedite the processing of your estimated payments.

RECORD OF ESTIMATED TAX PAYMENTS

|

|

DUE DATE OF PAYMENT |

|

|

|

|

|

|

|

DATE PAID |

|

|

|

|

AMOUNT PAID |

|

||||||||||||||||||||||||||||||||||||||||||||||||

|

_____________________________________________________________ |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

1. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

2. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

3. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

4. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Total payments to be taken on completed return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FAE 172

TENNESSEE DEPARTMENT OF REVENUE |

2 |

||

QUARTERLY FRANCHISE, EXCISE TAX DECLARATION |

|

||

|

|

|

|

Taxable |

BEGINNING |

ENDING |

|

Year |

|

|

|

ACCOUNT NUMBER |

|

|

|

|

|

|

|

|

|

|

|

FOR OFFICE

USE ONLY

Due Date:

If your account number is not preprinted or unknown, enter federal identification or social security number.

(FEIN/

SSN)

AMOUNT OF |

|

|

|

|

|

|

|

|

00 |

PAYMENT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FAE 172

TENNESSEE DEPARTMENT OF REVENUE |

3 |

||

QUARTERLY FRANCHISE, EXCISE TAX DECLARATION |

|

||

|

|

|

|

Taxable |

BEGINNING |

ENDING |

|

Year |

|

|

|

ACCOUNT NUMBER |

|

|

|

|

|

|

|

|

|

|

|

FOR OFFICE

USE ONLY

Due Date:

If your account number is not preprinted or unknown, enter federal identification or social security number.

(FEIN/

SSN)

AMOUNT OF |

|

|

|

|

|

|

|

|

00 |

PAYMENT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FAE 172

TENNESSEE DEPARTMENT OF REVENUE |

4 |

||

QUARTERLY FRANCHISE, EXCISE TAX DECLARATION |

|

||

|

|

|

|

Taxable |

BEGINNING |

ENDING |

|

Year |

|

|

|

|

|

|

|

ACCOUNT NUMBER |

|

|

|

|

|

|

|

|

|

|

|

FOR OFFICE

USE ONLY

Due Date:

If your account number is not preprinted or unknown, enter federal identification or social security number.

(FEIN/

SSN)

AMOUNT OF |

|

|

|

|

|

|

|

|

00 |

PAYMENT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Document Data

| Fact Name | Description |

|---|---|

| Form Identification | The form is titled "Tennessee Department of Revenue Quarterly Franchise, Excise Tax Declaration" and is designated as FAE 172. |

| Eligibility for Filing | Each taxpayer with a combined franchise and excise tax liability of $5,000 or more for the current tax year is required to make four quarterly estimated tax payments. |

| Payment Schedule | Quarterly payments are due on the 15th day of the fourth, sixth, and ninth months of the current year, and the first month of the succeeding year. |

| Penalties and Interest | A penalty at the rate of 5% per month, up to 25%, and interest at the current rate per annum are imposed upon any quarterly installment which is late or underpaid. |

Detailed Guide for Using Tennessee Fae 172

Completing the Tennessee FAE 172 form is an essential process for businesses that anticipate a franchise and excise tax liability of $5,000 or more for the current tax year. This form helps to organize quarterly estimated tax payments, ensuring that businesses comply with state tax requirements and avoid potential penalties and interest for underpayment or late submissions. Below are the steps you should follow to accurately fill out the form. Being thorough and precise in your calculations and submissions will streamline this periodic obligation, allowing you to focus on your business operations.

- Begin with filling out the Taxpayer Name and Mailing Address section. Include the legal name of your entity, your business address (box or street), city, state, and ZIP code.

- Specify the Taxable Year Beginning and Ending dates related to the fiscal year for which the taxes are being estimated.

- Locate the provided FAE Account Number. If it's preprinted, verify its accuracy. If not, you'll need to enter your Federal Employer Identification Number (FEIN) or Social Security Number (SSN) if you're a sole proprietor.

- Calculate your Estimated Franchise, Excise Tax Liability and enter this amount in the corresponding field. This figure is your total expected tax liability before any deductions.

- Deduct any available Franchise, Excise Tax Credits and prior year overpayments from your estimated tax liability to determine your net estimated tax liability.

- Enter the result in the Net Estimated Franchise, Excise Tax Liability field.

- Divide the net estimated tax liability by four to arrive at your Estimated Payment for the quarter and input this figure in the designated field. This step calculates the amount you should pay for this particular estimated tax voucher.

- Before submitting the form, review the Reminders section and the Instructions on the reverse side of the form to ensure all requirements are met, including roundings to the nearest dollar.

- Once completed, mail your form along with the estimated payment to the address provided on the form: Tennessee Department of Revenue, Andrew Jackson State Office Building, 500 Deaderick Street, Nashville, TN 37242.

After submission, mark your calendar for the next payment due dates as specified in the form instructions: the 15th day of the fourth, sixth, and ninth months of the current year, and the first month of the following year. Keeping track of these dates and planning accordingly will ensure timely compliance and help manage your business's financial obligations efficiently.

Important Questions on This Form

Who needs to file the Tennessee FAE 172 form?

The Tennessee FAE 172 form must be filed by taxpayers who anticipate having a combined franchise and excise tax liability of $5,000 or more for the current tax year. This form allows them to declare their franchise and excise tax for the taxable year and make the required quarterly payments.

When are the estimated payments due?

Estimated payments on the FAE 172 form are spread throughout the current tax year and are due on specific dates:

- The first payment is due on the 15th day of the 4th month of the current tax year.

- The second payment is due on the 15th day of the 6th month of the current tax year.

- The third payment is due on the 15th day of the 9th month of the current tax year.

- The fourth payment is due on the 15th day of the 1st month of the following tax year.

How is the amount of each estimated payment determined?

The amount of each quarterly payment must be the lesser of either:

- 25% of the combined franchise and excise tax shown on the tax return for the preceding tax year, which is adjusted accordingly if the preceding tax year was less than twelve months; or

- 25% of 100% of the combined franchise and excise tax liability estimated for the current tax year.

What are the penalties and interest for late or underpaid payments?

A penalty is assessed at a rate of 5% per month for any quarterly installment that is either late or underpaid, up to a total penalty of 25%. Additionally, interest accrues at the current rate per annum from the due date of the installment until the payment is made or until the fifteenth day of the fourth month following the close of the taxable year.

Which form should be used for making these payments?

All franchise and excise tax payments must be accompanied by the Tennessee Estimated Franchise, Excise Tax Declaration form (FAE 172). If a taxpayer received a pre-addressed packet from the Tennessee Department of Revenue, it is preferred to use the prenumbered vouchers and envelopes supplied with this packet. This aids in the expedited processing of estimated payments.

Common mistakes

Filling out the Tennessee FAE 172 form, a crucial document needed for the quarterly franchise and excise tax declaration, requires attention to detail. However, many people overlook several key aspects. Awareness and avoidance of these common mistakes can ensure the process is smoother and more accurate.

Firstly, many individuals mistakenly omit their account number or incorrectly enter their federal identification or social security number. This critical piece of information ensures that the payment is correctly applied to the taxpayer's account. Without it, processing can be delayed, leading to potential penalties.

Moreover, neglecting to make the estimated tax payment by the appropriate due dates is another frequent oversight. The form clearly outlines when payments are due - on the 15th day of the fourth, sixth, and ninth months of the current year, and the first month of the following year. Late payments may incur penalties and interest charges.

Furthermore, many filers fail to calculate their estimated payments accurately. The form provides a method to calculate the payment based on the lesser amount of 25% of the previous year's combined franchise and excise tax or 25% of the current year's estimated tax liability. An incorrect calculation can lead to underpayment or overpayment.

- Not reading the instructions on the back of the form carefully before beginning, leading to errors in completion.

- Forgetting to use the prenumbered vouchers and envelopes provided by the Department of Revenue, which can delay processing.

- Entering the wrong amount on the voucher compared to what was calculated on line 4 of the worksheet.

- Filing a voucher even when line 4 of the worksheet is zero, which is unnecessary.

- Rounding numbers incorrectly to the nearest dollar, leading to minor discrepancies in payment.

- Failing to keep the upper portion of the form for personal records, which is crucial for tracking payments.

- Overlooking the need to make adjustments for any tax credits or prior year overpayments, which can alter the net payment due.

Many of these errors can be easily avoided by taking the time to carefully review the form instructions and ensuring all information is complete and accurate before submission. Always remember the importance of timely and accurate payments to prevent any complications with the Tennessee Department of Revenue.

In summary, a thorough understanding and attention to detail when filling out the Tennessee FAE 172 form can prevent common mistakes that lead to processing delays, incorrect payment amounts, and potential penalties. By ensuring that all information is accurate and submissions are made on time, taxpayers can avoid unnecessary stress and complications..

Documents used along the form

When dealing with the complexities of tax documentation and compliance, knowing which forms and documents companionably align with Tennessee's FAE 172 form is crucial. This form, essential for quarterly franchise and excise tax declarations, integrates with several other documents critical for businesses aiming for accuracy and timeliness in their tax responsibilities. Each of these accompanying forms plays a distinctive role in ensuring that the breadth of taxation requirements is comprehensively addressed.

- Tennessee Department of Revenue Schedule N: This form is pivotal for reporting non-dividend distributions. It delineates the specifics of any distributions that do not qualify as dividends, which can influence the computation of excise taxes.

- Tennessee Form FAE 183: Essential for entities engaged in multistate business operations, this schedule aids in the apportionment of income. It allocates the income and franchise taxes based on the proportion of business activity conducted within the state.

- Tennessee Department of Revenue Schedule J: Focused on adjustments, Schedule J allows businesses to amend their gross income. It covers adjustments related both to additions and subtractions, ultimately affecting the taxable income calculation.

- Tennessee Form BUS415-3: Also known as the Application for Registration, this form is a preliminary requirement for businesses to legally operate in Tennessee. Its completion is essential before addressing franchise and excise tax obligations.

- Tennessee Department of Revenue Schedule G: This outlines the credits against franchise and excise taxes. By identifying eligible credits, businesses can reduce their owed tax amounts appropriately, reflecting any incentives or programs they utilize.

- Tennessee Form FAE170: This annual franchise and excise tax return is crucial for finalizing the yearly tax obligations. It consolidates the quarterly payments made with the FAE 172 form and reconciles them against the total annual liability.

Comprehending and appropriately applying these forms in conjunction with the FAE 172 form can significantly streamline the tax filing process for Tennessee businesses. Each document's unique role ensures that entities meet their tax obligations with precision, benefiting from all applicable deductions and credits. Indeed, navigating these requirements with a sharp and informed approach fosters both compliance and financial health for businesses within the state.

Similar forms

The Form 1040-ES, "Estimated Tax for Individuals," shares similarities with the Tennessee FAE 172 form in its fundamental purpose, which is to facilitate the process of estimating and paying taxes ahead of the normal filing deadline. Both forms require taxpayers to calculate the amount of tax they expect to owe for the year and make payments on a quarterly basis. While the FAE 172 form is specific to Tennessee's franchise and excise taxes, the 1040-ES is used by individuals for federal income tax. Despite this difference, each form is crucial in helping taxpayers avoid underpayment penalties by encouraging the timely and incremental payment of estimated taxes.

The Form 1120-W, "Estimated Tax for Corporations," is another document that resembles the FAE 172 form, albeit for corporate entities. Corporations use the 1120-W to estimate their federal income tax liability and make quarterly tax payments, similar to how businesses in Tennessee use the FAE 172 form for their franchise and excise taxes. Both forms serve to help entities manage their tax liabilities through scheduled payments, thus preventing large lump-sum payments at the end of the tax year. However, the specific taxes addressed by each form differ, reflecting the distinct tax obligations of individuals and corporate entities at the federal and state levels, respectively.

The "Employer's Quarterly Federal Tax Return," known as Form 941, is utilized by employers to report income taxes, Social Security tax, or Medicare tax withheld from employees' paychecks, and it also involves the employer's portion of Social Security or Medicare tax. The parallel to the FAE 172 form lies in the quarterly submission requirement, designed to manage cash flow effectively and ensure compliance through regular remittances to the tax authorities. Although the FAE 172 focuses on franchise and excise taxes for businesses in Tennessee and Form 941 addresses federal payroll taxes, both are pivotal in maintaining taxpayer compliance on a quarterly basis.

Form 720, "Quarterly Federal Excise Tax Return," is used to report and on paying federal excise taxes on specific goods, services, and activities. The similarity to the Tennessee FAE 172 form comes from its quarterly filing aspect and its focus on excise taxes, although the FAE 172 combines franchise and excise taxes applicable within Tennessee. Both forms are essential for businesses to comply with their respective tax obligations, ensuring timely payments and reporting that help to fund federal and state initiatives.

The Schedule H (Form 1040), "Household Employment Taxes," is intended for individuals who employ household help and are responsible for paying federal employment taxes on wages paid to their employees. While it serves a different taxpayer group, the underlying principle of scheduled tax payments and reporting is a shared feature with the FAE 172 form. The Schedule H consolidates tax reporting and payment on an annual basis, as opposed to the quarterly approach of the FAE 172; nonetheless, both documents facilitate the orderly payment of taxes owed, further illustrating the broad applicability of pre-payment mechanisms across various tax types and jurisdictions.

Dos and Don'ts

When completing the Tennessee FAE 172 form, a Quarterly Franchise, Excise Tax Declaration, there are key practices to follow to ensure accuracy and compliance. Below are six do's and don'ts to guide you through the process:

- Do carefully read the instructions on the reverse side of the form before starting. They provide crucial details about how to fill out the form correctly.

- Do use the prenumbered vouchers and envelopes provided by the Department of Revenue. These are designed to help streamline the submission process and ensure your payments are processed efficiently.

- Do enter the amount from Line 4 of the worksheet into the "Amount of Payment" field on the voucher accurately. This ensures that your payment is accurately reflected in your tax records.

- Don't neglect to round to the nearest dollar. The form specifies that all financial amounts should be rounded, which helps avoid discrepancies and simplifies the calculation process.

- Don't submit the voucher if Line 4 of the worksheet is zero. Submitting unnecessary documentation can complicate your tax file and involves unnecessary paperwork for the Department of Revenue.

- Don't overlook the due dates for the quarterly payments. Late or underpaid installments can result in penalties and interest charges, so it is crucial to make payments on time and in the correct amount.

Adhering to these guidelines will help ensure that the process of completing the Tennessee FAE 172 form goes smoothly and that your franchise and excise tax obligations are met accurately and on time.

Misconceptions

Understanding the Tennessee FAE 172 form is crucial for businesses operating within the state. This document facilitates the quarterly declaration and payment of franchise and excise taxes due to the Tennessee Department of Revenue. However, misconceptions surrounding the form can lead to errors in compliance and the administration of taxes. This can have significant implications for any business. Here, we aim to clarify four common misconceptions to ensure businesses can navigate their tax obligations with confidence.

Misconception 1: Only Large Businesses Need to File the FAE 172 Form

Some businesses operate under the incorrect assumption that the FAE 172 form only applies to large or established businesses. In reality, any business that expects a combined franchise and excise tax liability of $5,000 or more for the current tax year is required to file this form and make quarterly payments. This threshold can apply to businesses of various sizes, and overlooking this obligation can lead to underpayment penalties and interest.

Misconception 2: The Form is Optional if Estimated Taxes are Below $5,000

There’s a belief that if a business anticipates its franchise and excise tax liability will be less than $5,000 for the year, filing the FAE 172 form becomes optional. This misunderstanding can cause confusion about tax obligations. While it’s true that the mandatory filing requirement kicks in at the $5,000 mark, opting not to calculate or submit quarterly payments accurately can lead to a surprise tax liability at year-end. It is advisable for all businesses to closely monitor their tax liabilities to avoid unexpected debt to the Department of Revenue.

Misconception 3: Penalty and Interest Charges are Negligible

Some taxpayers downplay the significance of the penalty and interest charges applied to late or underpaid quarterly installments. The FAE 172 instructions outline that a penalty at the rate of 5% per month up to a 25% maximum, plus interest at the current rate per annum, is applied to any installment not paid on time or if underpaid. These charges can accumulate quickly, adding a substantial burden to the original tax liability, emphasizing the importance of timely and accurate payments.

Misconception 4: The Payment Due Date is Flexible

A common fallacy among some businesses is the belief that the due date for each quarterly payment offers some degree of flexibility. In contrast, the Tennessee Department of Revenue enforces strict deadlines for these payments: the 15th day of the fourth, sixth, and ninth months of the current tax year, and the first month of the succeeding year. Missing these deadlines, even by a small margin, can trigger the penalties and interest detailed above. It underscores the necessity for businesses to prepare their tax calculations well in advance of these dates.

Correcting these misconceptions and adopting a proactive approach to tax responsibilities can save businesses time and money. The Tennessee FAE 172 form is a pivotal component of state tax compliance, and understanding its requirements is essential for all businesses required to file. Accurate and timely adherence to these obligations not only ensures compliance but also prevents the accrual of unnecessary penalties and interest.

Key takeaways

The Tennessee Department of Revenue requires certain businesses to make quarterly franchise and excise tax payments throughout the fiscal year. Understanding the essential elements of the Tennessee FAE 172 form can guide taxpayers through the process of making these payments accurately and on time. Here are five key takeaways:

- Who must file: Any taxpayer anticipating a combined franchise and excise tax liability of $5,000 or more for the current tax year is obligated to file the Tennessee FAE 172 form. This form enables them to declare their estimated tax liability and make appropriate quarterly payments.

- When to make payments: Payments are due at four critical times throughout the year: the 15th day of the fourth month, the 15th day of the sixth month, the 15th day of the ninth month of the current year, and the 15th day of the first month of the following year.

- How to calculate the payment: The minimum amount due for each quarterly payment is the lesser of 25% of the combined franchise and excise tax shown on the return for the previous year or 25% of 100% of the estimated tax liability for the current year.

- Penalties for late or underpayment: If quarterly installments are paid late or are underpaid, the taxpayer faces a penalty of 5% per month, up to a maximum of 25%, along with interest at the current rate from the installment's due date until payment.

- Required documentation: All franchise and excise tax payments must be accompanied by the Tennessee Estimated Franchise, Excise Tax Declaration form (FAE 172). Utilizing the prenumbered vouchers and envelopes provided by the Tennessee Department of Revenue can help expedite processing.

These key points can help ensure that taxpayers meet their obligations efficiently, avoiding unnecessary penalties and delays. It’s also imperative to consult the instructions on the reverse side of the FAE 172 form for detailed guidance on filling out the form and making accurate calculations.

Create Other Documents

What Is a Class D License in Tn - The form serves as a direct communication line with the Tennessee Department of Safety, streamlining crash reporting.

Llc in Tennessee Cost - Understanding and utilizing this form is crucial for the legal maintenance and operational integrity of an LLC in Tennessee.

How Long After Mediation Is Divorce Final in Tennessee - A foundational document in Tennessee divorces, solidifying the terms of separation including asset division and parenting responsibilities.