Get Tennessee Exemption Certificate Template in PDF

Understanding the Tennessee Exemption Certificate form is crucial for organizations aiming to benefit from the specific tax exemptions offered by the state. Issued by the Tennessee Department of Revenue, the form grants qualifying entities, such as the University of Iowa, the authority to make purchases of tangible personal property or taxable services without the payment of sales or use tax. This privilege is strictly for goods and services used or consumed by the organization or for items to be given away, not for merchandise intended for resale. The form also outlines the requirement for organizations to provide their suppliers with a copy of the exemption certificate, maintaining the original for record-keeping purposes. Furthermore, it highlights the importance of the purchasers’ responsibility to ensure that all transactions under this exemption comply with the stipulated conditions and to duly notify the Department of Revenue of any significant changes to their operational status. With an effective date marked, the document also underlines the role of the person acting as the authorized representative of the organization, who must affirm, under the penalty of perjury, the legitimate use of purchases made under this authority. This article aims to delve into the major aspects of the Tennessee Exemption Certificate form, providing essential insights into its application, operational guidelines, and the necessary compliance responsibilities laid out for organizations seeking to utilize this tax exemption provision.

Document Preview Example

N0003101 |

7632128070716 |

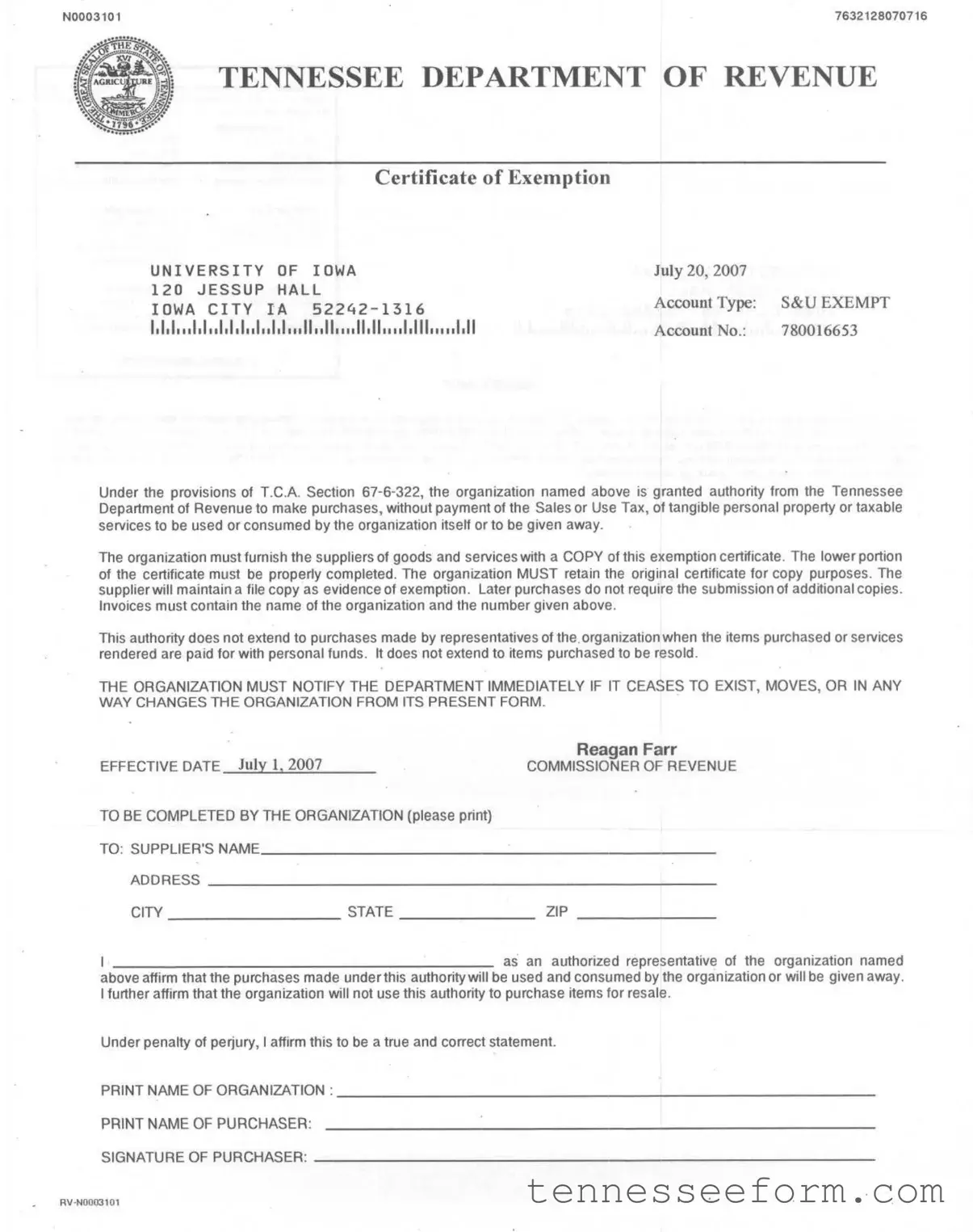

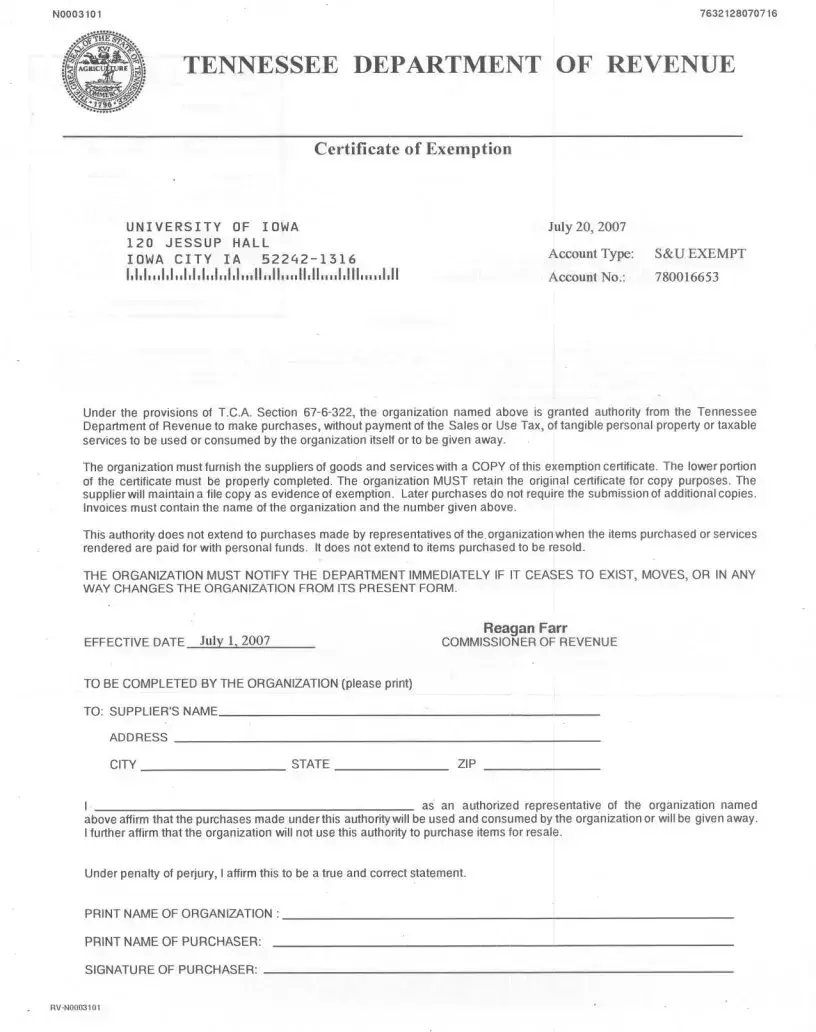

TENNESSEE DEPARTMENT OF REVENUE

Certificate of Exemption

UNIVERSITYOF IOWA

120 JESSUP HALL

IOWA CITY IA

1,1,1".1,1"1.1,1,,1,,1,1,,, 11"11",, 11,11" "1,111,,, "I,ll

July 20, 2007

Account Type: S&U EXEMPT

Account No.: 780016653

Under the provisions of T.CA Section

The organization must furnish the suppliers of goods and services with a COPY of this exemption certificate. The lower portion of the certificate must be properly completed. The organization MUST retain the original certificate for copy purposes. The supplier will maintain a file copy as evidence of exemption. Later purchases do not require the submission of additional copies. Invoices must contain the name of the organization and the number given above.

This authority does not extend to purchases made by representatives of the. organization when the items purchased or services rendered are paid for with personal funds. It does not extend to items purchased to be resold.

THE ORGANIZATION MUST NOTIFY THE DEPARTMENT IMMEDIATELY IF IT CEASES TO EXIST, MOVES, OR IN ANY WAY CHANGES THE ORGANIZATION FROM ITS PRESENT FORM.

|

Reagan |

Farr |

EFFECTIVE DATE July 1, 2007 |

COMMISSIONER |

OF REVENUE |

TO BE COMPLETED BY THE ORGANIZATION (please print)

TO: SUPPLIER'S NAME |

|

|

|

_ |

ADDRESS |

|

|

|

_ |

CITY |

STATE |

_ |

ZIP |

_ |

I |

as |

an |

authorized |

representative of the organization named |

above affirm that the purchases made under this authority will be used and consumed by the organization or will be given away. I further affirm that the organization will not use this authority to purchase items for resale.

Under penalty of perjury, I affirm this to be a true and correct statement.

NAME OF ORGANIZATION: |

_ |

|

NAME OF PURCHASER: |

|

|

SIGNATURE OF PURCHASER: |

_ |

|

RV·N0003101

UNIVERSITY OF IOWA 120 JESSUP HALL

IOWA CITY IA

1,1,1"11,1111,1,111111111'11111111'11111,1111111,111111111,11

ASSISTANCE

For additional information, contact the Taxpayer and

Vehicle Services Division in one of our Department of Revenue Offices:

|

Chattanooga |

|

Jackson |

|

(423) |

(731) |

|||

Suite |

350 |

|

Suite |

340 |

State |

Office |

Building |

Lowell |

Thomas Building |

540 |

McCallie |

Avenue |

225 Martin Luther King Blvd. |

|

|

|

|

||

Johnson |

City |

|

Knoxville |

||

(423) |

|

(865) |

|||

204 High |

Point |

Drive |

Room 606 |

|

|

|

|

|

State |

Office |

Building |

|

|

|

531 |

Henley |

Street |

Memphis |

|

Nashville |

||

(901) |

(615) |

|||

3150 |

Appling Road |

3rd |

Floor, AJ |

Building |

Bartlett |

500 |

Deaderick |

Street |

|

www.tennessee.qov/revenue

For additional information or assIstance regarding this notice, you should contact the Department of Revenue. Tennessee residents may use the

number,

written information to the following address: Tennessee Department of Revenue, 500 Deaderick Street, Nashville, TN 37242. Please provide your account number and notice number when inquiring about the notice.

Document Data

| Fact Name | Description |

|---|---|

| Governing Law | Tennessee Code Annotated (T.C.A) Section 67-6-322 governs the issuance of the Tennessee Exemption Certificate. |

| Purpose | The certificate grants exempt organizations the authority to make tax-free purchases of tangible personal property or taxable services for their own use or to be given away. |

| Eligibility | Organizations must be recognized as exempt under the provisions of T.C.A Section 67-6-322 to qualify for the exemption certificate. |

| Certificate Requirement | Organizations must provide suppliers with a copy of the exemption certificate to make tax-exempt purchases. |

| Recordkeeping | Original certificates must be retained by the organization for copy purposes, and suppliers must keep a file copy as evidence of exemption. |

| Limitations | The exemption does not apply to personal purchases by representatives of the organization, nor to items purchased for resale. |

| Notification Requirement | If there are any changes to the organization's status, existence, or address, the Tennessee Department of Revenue must be notified immediately. |

| Contact Information | For assistance, the Department of Revenue provides contact numbers for offices in Chattanooga, Jackson, Johnson City, Knoxville, Memphis, and Nashville, including a toll-free number and TDD for the hearing impaired. |

Detailed Guide for Using Tennessee Exemption Certificate

Filling out the Tennessee Exemption Certificate is a straightforward process but vital for organizations eligible to make tax-exempt purchases in Tennessee. By following the step-by-step instructions below, the authorized representative of the organization can ensure the certificate is correctly completed and that their purchases comply with the regulations set by the Tennessee Department of Revenue.

- Locate the section of the form titled "TO BE COMPLETED BY THE ORGANIZATION".

- In the space provided, write down the SUPPLIER'S NAME.

- Enter the SUPPLIER'S ADDRESS, including CITY, STATE, and ZIP CODE in the respective fields.

- As an authorized representative of the organization claimed at the beginning of the form, affirm the statement by filling in the organization's name where it says "PRINT NAME OF ORGANIZATION:".

- Next to the above, print your name as the purchaser where it prompts "PRINT NAME OF PURCHASER:".

- Underneath, provide your SIGNATURE in the space labeled "SIGNATURE OF PURCHASER:" to declare the information provided is accurate and you are authorized to make this affirmation.

- Before submitting the completed form to the supplier, re-check all the filled-out sections for accuracy to ensure the information matches that of the original certificate issued by the Tennessee Department of Revenue.

- Keep the original exemption certificate secure as the organization must retain it for copy purposes, and give a copy to the supplier.

After the supplier received the completed form, they should keep it on file as evidence of exemption for tax-exempt transactions. Remember, for any new purchases from the same supplier, it isn't necessary to submit additional copies of the exemption certificate as long as the supplier has the completed form on file. It's also important for the organization to notify the Tennessee Department of Revenue immediately if there are any changes in its status, location, or form.

Important Questions on This Form

What is a Tennessee Exemption Certificate?

A Tennessee Exemption Certificate is a document, issued by the Tennessee Department of Revenue, that authorizes an organization to make purchases of tangible personal property or taxable services without paying the state's sales or use tax. This exemption is specifically granted under the provisions of T.C.A Section 67-6-322 and is applicable when the purchases are intended for use or consumption by the organization itself, or for items to be given away.

Who can use the Tennessee Exemption Certificate?

The certificate can be used by organizations that are recognized as exempt from paying sales or use tax by the Tennessee Department of Revenue. These include certain non-profit organizations, educational institutions, and governmental entities. It is important that the organization is specifically granted authority by the Department before utilizing the exemption certificate for purchases.

How does an organization apply for a Tennessee Exemption Certificate?

Organizations must apply directly to the Tennessee Department of Revenue to obtain a Tennessee Exemption Certificate. The application process involves submitting specific information about the organization for review, including its purpose, operations, and how it qualifies for a sales and use tax exemption. Detailed application procedures can be found on the Tennessee Department of Revenue's website or by contacting their office directly.

What purchases are eligible under the Tennessee Exemption Certificate?

Eligible purchases include tangible personal property or taxable services that are used or consumed by the exempt organization or are given away. These purchases must be directly related to the organization's exempt purpose. It is crucial for organizations to understand that the certificate does not cover purchases made by representatives of the organization if those purchases are for personal use or if the items purchased are for resale.

How should the Tennessee Exemption Certificate be used?

When making an eligible purchase, the exempt organization must provide the supplier with a copy of the exemption certificate. The original must be retained by the organization for its records. Suppliers, in turn, should keep a copy of the certificate on file as evidence of the exemption. Invoices related to such purchases should clearly include the name of the organization and the provided exemption number.

Yes, the Tennessee Exemption Certificate includes an effective date but does not list an expiration date. However, it remains valid as long as the organization's exempt status does not change. If the organization ceases to exist, relocates, or undergoes any significant change in structure or operations that affects its exempt status, it must notify the Tennessee Department of Revenue immediately.

Can the exemption certificate be used for purchases made with personal funds?

No, the exemption provided by the certificate does not extend to purchases made by individuals representing the organization if those purchases are made with personal funds. The exemption is strictly intended for purchases that are directly paid for by the organization and are for the organization's use or for items to be given away.

What should an organization do if its status changes after receiving the Tennessee Exemption Certificate?

If there are any changes to an organization's status, location, or structure, it must notify the Tennessee Department of Revenue immediately. Changes that affect the organization's exempt status could invalidate the exemption certificate, and failure to notify the Department may result in the organization being held liable for sales and use taxes on purchases made after such changes.

Common mistakes

When completing the Tennessee Exemption Certificate form, accuracy and attention to detail are paramount. However, there are common mistakes that individuals and organizations frequently make, which can lead to issues with tax exemptions and compliance. Identifying these errors can significantly streamline the process, ensuring that the benefits of tax exemption are fully realized without unnecessary complications.

- Not providing the complete name and address of the organization – Essential for proper identification and to avoid mix-ups with similarly named entities.

- Failure to print clearly – Legibility is crucial as any misunderstanding can delay the approval process or lead to incorrect recordings of the exemption status.

- Omitting the authorized representative’s signature – A common oversight that invalidates the form since the signature provides a binding declaration of the information’s accuracy.

- Forgetting to include the exemption number on subsequent invoices – Suppliers need this for their records to verify the tax-exempt purchase, ensuring compliance on both ends.

- Neglecting to indicate the specific use of purchased items – Clarifying whether items will be used directly by the organization, or given away, is mandatory to maintain the exemption.

- Assuming the certificate covers personal purchases – The exemption is strictly for the organization’s use. Personal purchases by representatives must be kept separate.

- Using the certificate for items intended for resale – This is a direct violation of the terms of the exemption and can lead to its revocation.

- Not updating the Department of Revenue on organizational changes – Any modifications to the organization's status, location, or form must be reported immediately to maintain the exemption.

- Overlooking the need for contacting the Department of Revenue for assistance – Guidance is available and should be sought in case of uncertainties regarding the completion of the certificate or changes affecting exemption status.

Adhering to these guidelines can help avoid the pitfalls that frequently accompany the completion of the Tennessee Exemption Certificate form. The emphasis should always be on clear communication, thoroughness, and an understanding of the restrictions and responsibilities conferred by the tax-exempt status. By avoiding these common mistakes, organizations can ensure a smoother process and focus on their core missions without undue administrative burdens.

In conclusion, the process of completing the Tennessee Exemption Certificate form requires careful consideration of several key details. Organizations seeking tax-exempt status for their purchases must be diligent in their adherence to the stipulations set forth by the Tennessee Department of Revenue. By avoiding common errors, such as those listed above, and seeking clarity and assistance when needed, organizations can navigate the exemption process more efficiently and effectively. The ultimate goal is to leverage tax-exempt privileges responsibly, thereby supporting the organization’s objectives while remaining compliant with state tax laws.

Documents used along the form

Securing a Tennessee Exemption Certificate is a critical step for eligible entities wishing to purchase goods or services without the added weight of sales or use tax. This document, while powerful, is often just one piece of the broader compliance and documentary framework necessary for smooth operational procedures, especially for non-profit organizations, educational institutions, and other qualifying entities in Tennessee. Several other forms and documents typically accompany or complement the exemption certificate in various transactions and regulatory requirements.

- Streamlined Sales and Use Tax Agreement Certificate of Exemption: This multi-state form allows qualifying entities to make exempt purchases in Tennessee and other member states without needing to complete separate exemption certificates for each state.

- Business Tax Application: Entities establishing operations in Tennessee must file this form to register for business tax, which is a prerequisite for applying for certain types of tax exemptions.

- Annual Financial Statement: While not a form submitted to the Tennessee Department of Revenue, many organizations must prepare and retain annual financial statements. These documents are crucial during audits to validate the non-profit status and proper use of purchased goods under the tax exemption.

- IRS Determination Letter: This letter from the Internal Revenue Service (IRS) confirms an entity's tax-exempt status under Section 501(c)(3) or other applicable sections. It is often required to be on file or presented when applying for state-level exemptions.

- Sales and Use Tax Return: Despite being exempt from sales and use tax on certain purchases, organizations might still need to file periodic returns to report other taxable sales or purchases not covered by their exemption certificate.

- Purchase Order Documentation: When making an exempt purchase, the entity must often provide a purchase order or similar documentation alongside the exemption certificate. This helps to assure vendors that the purchase qualifies for the tax exemption.

- Change of Address or Status Form: Should an organization move, change its name, or undergo significant operational changes, it needs to update its information with the Tennessee Department of Revenue to maintain its exemption status.

Together, these documents form a cohesive bundle that qualifying entities in Tennessee must manage with diligence and care. Whether engaging in everyday operations or undergoing scrutiny during audits, the Tennessee Exemption Certificate and its companion documents ensure that organizations can navigate tax regulations efficiently while dedicating their resources to the mission-critical endeavors that define their work.

Similar forms

The Form W-9, Request for Taxpayer Identification Number and Certification, shares similarities with the Tennessee Exemption Certificate, primarily in its purpose to provide necessary documentation to exempt entities from tax withholdings. Both forms serve as essential instruments for tax compliance, ensuring that organizations engage in transactions without the need for tax deductions at the source, based on specific qualifying conditions set by the IRS for the Form W-9 and the Tennessee Department of Revenue for the Exemption Certificate.

Another comparable document is the Sales and Use Tax Exemption Certificate, universally used across various states to document the exemption of qualifying organizations from sales and use tax. Similar to the Tennessee Exemption Certificate, these certificates require detailed information about the purchasing entity and affirm the purpose of purchases to ensure compliance with tax exemption statutes, thus avoiding unnecessary tax payments on applicable transactions.

The Nonprofit Organization's Declaration of Sales Tax Exemption functions similarly to the Tennessee Exemption Certificate by allowing nonprofit organizations to make purchases or conduct transactions without being charged sales tax. This declaration often necessitates the nonprofit to provide proof of its tax-exempt status, just as the Tennessee Exemption Certificate necessitates proof of exemption under T.C.A Section 67-6-322. Both documents facilitate tax-free purchases when conditions are met.

The Resale Certificate is used by businesses to purchase goods intended for resale without paying sales tax. This document parallels the Tennessee Exemption Certificate in its role of tax exemption, although it specifically addresses items for resale, which the Tennessee Exemption Certificate explicitly excludes. Both certificates prevent unnecessary taxation, maintaining the integrity of tax-exempt purchases but for categorically different purposes.

Streamlined Sales Tax Exemption Certificates, which are part of a simplification effort across multiple states to standardize tax exemption processes for sellers and purchasers, share the goal of the Tennessee Exemption Certificate to simplify tax-exempt transactions. While the Streamlined versions apply across participating states for various exempt purposes, Tennessee’s certificate specifically facilitates tax-exempt purchases within state boundaries as defined by its laws.

The Exempt Organization Business Income Tax Return (Form 990-T) is notably different in purpose, being an IRS form for reporting unrelated business income by tax-exempt entities, but it aligns with the Tennessee Exemption Certificate in its connection to tax-exempt status management. Organizations that use the Tennessee certificate must similarly track and report certain activities that might not be covered by their exemption, emphasizing the continuous obligation of tax-exempt entities to maintain compliance across different tax scenarios.

The Certificate of Authority, which is often required for non-local businesses to legally operate in a foreign state, shares a fundamental connection with the Tennessee Exemption Certificate through the necessity of obtaining authorization from state authorities. Although one certifies legal business operation and the other tax exemption, both are official recognitions by state agencies that grant specific privileges or rights.

Lastly, the Property Tax Exemption Application shares a conceptual resemblance with the Tennessee Exemption Certificate by affirming an entity's right to bypass certain taxation based on qualifying criteria. While the Property Tax Exemption pertains to real estate and personal property tax, the foundation of affirming eligibility for exemptions under certain conditions remains a common attribute between the two documents, streamlining tax relief efforts for eligible parties.

Dos and Don'ts

When filling out the Tennessee Exemption Certificate form, it is important to follow certain guidelines to ensure that the process is completed efficiently and correctly. Here is a list of things one should and shouldn't do:

- Do provide accurate information about your organization, including the correct name and address. This ensures that all documentation accurately reflects the entity claiming the exemption.

- Do ensure that the person filling out the form is an authorized representative of the organization. This guarantees that the declaration made on the form is valid and legally binding.

- Do keep the original certificate within your organization’s records and provide a copy to suppliers. The original document is essential for future verification and copy purposes.

- Do clearly state the purpose of the purchases (to be used, consumed by the organization, or to be given away) as specified in the certificate. This clarity is crucial for compliance with the exemption’s conditions.

- Don’t use the exemption certificate for personal purchases. Items purchased or services rendered with personal funds are not covered under this exemption certificate.

- Don’t purchase items for resale using this certificate. The exemption specifically excludes items that are bought for the purpose of being resold.

- Don’t fail to notify the Department of Revenue if there are any changes to the organization’s status, address, or form. Keeping the department updated helps maintain the validity of the exemption certificate.

By following these guidelines, organizations can ensure that they are using the Tennessee Exemption Certificate appropriately and staying in compliance with state regulations. Always remember to provide accurate and truthful information to avoid any legal complications.

Misconceptions

Understanding the Tennessee Exemption Certificate can be complex, and several misconceptions commonly arise. To clarify these misunderstandings, here are six common misconceptions explained:

- Only educational institutions can qualify for the exemption: This misconception stems from the certificate's example organization being a university. However, various types of organizations, including non-profits and certain types of businesses, can qualify under T.C.A Section 67-6-322 for tax exemption on eligible purchases.

- The exemption applies to all purchases made by the organization: The exemption is specifically for purchases of tangible personal property or taxable services to be used or consumed by the organization itself or to be given away. It does not cover items purchased for resale or personal purchases made by representatives of the organization.

- Once an exemption certificate is issued, it never needs to be renewed: While the document doesn't specify an expiration date, organizations must notify the Department of Revenue if there are any changes to their status or if they cease to exist. It's also a good practice to ensure that the certificate is still considered valid over time and under current regulations.

- Any representative of an organization can make exempt purchases without further documentation: The certificate makes it clear that purchases must be accompanied by a copy of the exemption certificate, and the name of the organization and the exemption number should be on the invoices. Personal purchases by representatives, even for the organization's use, do not qualify under this exemption.

- Submitting a copy of the exemption certificate is only required for the first transaction with a supplier: While the original certificate should be retained by the organization and a copy is provided to the supplier for file-keeping, it’s crucial that the supplied information is noted on all relevant invoices for tracking and compliance purposes.

- The exemption certificate grants exemption from all types of taxes: The certificate specifically exempts eligible organizations from Sales and Use Taxes on qualified purchases. It does not extend to other types of taxes, such as property taxes or income taxes, that the organization may be subject to.

Understanding the scope and limitations of the Tennessee Exemption Certificate is essential for organizations to ensure compliance and to accurately apply for and use the tax exemption privileges granted under Tennessee law.

Key takeaways

Filling out and using the Tennessee Exemption Certificate requires attention to detail and an understanding of its specific provisions. To assist in navigating this form, here are key takeaways that organizations should consider:

- The exemption certificate is granted by the Tennessee Department of Revenue under T.C.A Section 67-6-322, allowing qualified organizations to make purchases without paying sales or use tax on tangible personal property or taxable services intended for the organization's use or to be given away.

- Organizations must provide suppliers with a copy of the exemption certificate for tax-exempt purchases. However, this certificate does not cover items purchased for resale or purchases made by representatives of the organization with personal funds.

- Retaining the original certificate is crucial for the organization, as it must be available for copy purposes for future transactions. Suppliers will also keep a copy as evidence of the tax exemption.

- Any changes in the organization's status, such as ceasing to exist, moving, or altering its form, must be promptly reported to the Department of Revenue. Compliance with these conditions ensures the continued validity of the tax-exempt status under the provided authority.

It's also important for authorized representatives filling out the form to affirm under penalty of perjury that purchases made under this authority are indeed for the organization's use or to be given away, and not for resale. Accurate completion and compliance with the stipulations outlined in the exemption certificate safeguard the organization's tax-exempt privileges and promote effective fiscal management.

For any additional questions or assistance, organizations can contact the Tennessee Department of Revenue or visit their website. Staying informed and promptly addressing any certificate or tax status changes can help prevent complications and ensure smooth, tax-exempt transactions for eligible entities.

Create Other Documents

What Is a Class D License in Tn - Designed by the Tennessee Department of Safety and Homeland Security, it requires details about the crash, including date, location, and vehicle specifics.

Tennessee In 1655 - Orchestrates a streamlined application process for locksmith apprenticeships in Tennessee, emphasizing critical information gathering and regulatory compliance.