Get Tennessee Bus 416 Template in PDF

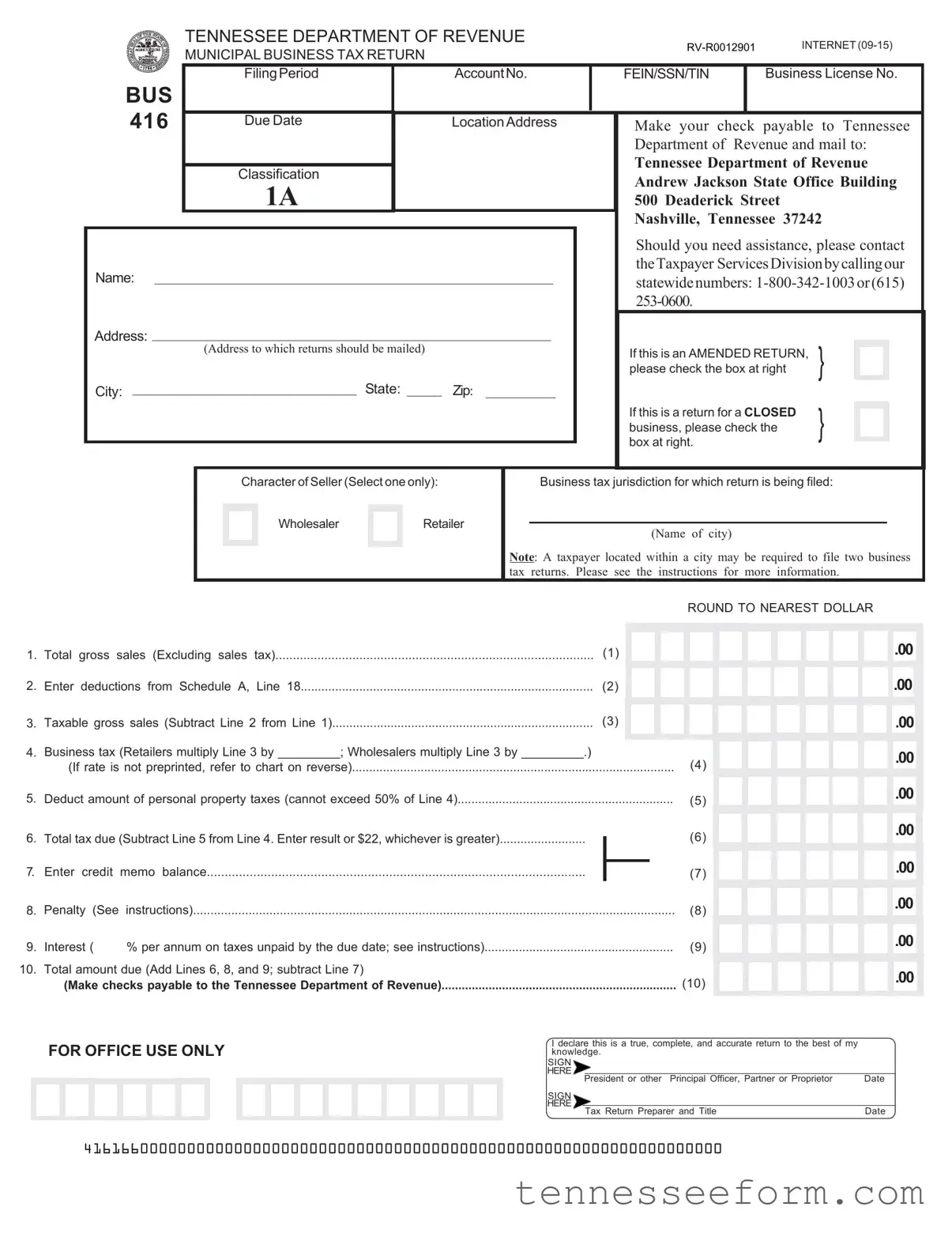

Business operations within Tennessee are subject to various regulations and tax obligations, one of which includes the Municipal Business Tax Return, more formally known as the BUS 416 form. This essential document, overseen by the Tennessee Department of Revenue, serves as a comprehensive tool for businesses to report their taxable sales, calculate due taxes, and summarize deductions such as sales in interstate commerce, returned merchandise, and bad debts, among others. The form caters to both wholesalers and retailers by offering different tax rate calculations and allows for adjustments based on personal property taxes paid. Significantly, it also accommodates businesses that are closing or amending previous returns, highlighting the state's adaptability to changing business landscapes. Deductions, a crucial part of the tax return process, demand meticulous record-keeping, as failure to substantiate claimed deductions can lead to their disallowance. Moreover, the form delineates specific rates for different classifications of retailers and wholesalers, along with the tax periods and due dates, thereby guiding businesses through their fiscal responsibilities. It's a testament to the structured yet flexible approach Tennessee takes towards business taxation, ensuring clarity and compliance in the pursuit of a healthy economic environment.

Document Preview Example

TENNESSEE DEPARTMENT OF REVENUE

MUNICIPAL BUSINESS TAX RETURN

INTERNET |

|

|

FilingPeriod |

|

AccountNo. |

|

FEIN/SSN/TIN |

|

Business License No. |

||||||

BUS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

416 |

|

|

|

|

|

|

|

|

|

|

||||

|

Due Date |

|

LocationAddress |

Make your check |

payable |

to Tennessee |

||||||||

|

|

|

|

|

|

|

Department of Revenue and mail to: |

|||||||

|

|

|

|

|

|

|

Tennessee Department of Revenue |

|||||||

|

|

Classification |

|

|

|

|

||||||||

|

|

|

|

|

|

Andrew Jackson State Office Building |

||||||||

|

|

1A |

|

|

|

|

||||||||

|

|

|

|

|

|

500 Deaderick Street |

|

|

|

|

|

|||

|

|

|

|

|

|

|

Nashville, Tennessee 37242 |

|||||||

|

|

|

|

|

|

|

Should you need assistance, please contact |

|||||||

Name: _________________________________________________________ |

|

|

theTaxpayer ServicesDivisionbycallingour |

|||||||||||

|

|

statewidenumbers: |

||||||||||||

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address: _________________________________________________________ |

|

|

|

|

|

|

|

|

|

|

||||

|

|

(Address to which returns should be mailed) |

|

|

|

If this is an AMENDED RETURN, |

} |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

please check the box at right |

|

|

|

|

|||

City: ________________________________ State: _____ |

Zip: __________ |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

If this is a return for a CLOSED |

} |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

business, please check the |

|

|

|

|

|||

|

|

|

|

|

|

|

box at right. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Character of Seller (Select one only):

Wholesaler Retailer

Business tax jurisdiction for which return is being filed:

(Name of city)

Note: A taxpayer located within a city may be required to file two business tax returns. Please see the instructions for more information.

|

|

|

|

|

|

|

ROUND TO NEAREST DOLLAR |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Total gross sales (Excluding sales tax) |

(1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

Enter deductions from Schedule A, Line 18 |

(2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

(3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. |

Taxable gross sales (Subtract Line 2 from Line 1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Business tax (Retailers multiply Line 3 by _________; Wholesalers multiply Line 3 by _________.) |

|

|

|

|

|

(If rate is not preprinted, refer to chart on reverse) |

(4) |

|||

5. |

Deduct amount of personal property taxes (cannot exceed 50% of Line 4) |

(5) |

|||

6. |

Total tax due (Subtract Line 5 from Line 4. Enter result or $22, whichever is greater) |

|

(6) |

||

|

|||||

7. |

Enter credit |

memo balance |

|

|

|

|

(7) |

||||

8. |

Penalty (See |

instructions) |

|||

9. |

Interest ( |

% per annum on taxes unpaid by the due date; see instructions) |

(9) |

||

10. |

Total amount due (Add Lines 6, 8, and 9; subtract Line 7) |

|

|

|

|

|

(Make checks payable to the Tennessee Department of Revenue) |

(10) |

|||

.00

.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

FOR OFFICE USE ONLY

I declare this is a true, complete, and accurate return to the best of my knowledge.

SIGN

HERE

|

President or other Principal Officer, Partner or Proprietor |

Date |

|

SIGN |

|

||

HERE |

|

|

|

Tax Return Preparer and Title |

Date |

||

|

|||

41616600000000000000000000000000000000000000000000000000000000000000

INTERNET

Schedule A. Deductions from Gross Sales |

|

1. Sales of services received by persons located in other states |

(1) |

2. Returned merchandise when the sales price is refunded to the customer |

(2) |

.00

.00

.00

.00

3.Sales in interstate commerce where the purchaser takes possession outside Tennessee for use or consumption outside Tennessee.......................................................................................................

4.Cash discounts allowed and taken on sales.......................................................................................

5.Repossessions - The portion of the unpaid principal balance in excess of $500 due on tangible per- sonal property repossessed from customers.......................................................................................

6.The amount allowed as

7.Bad debts written off during the reporting period and eligible to be deducted for federal income tax purposes.........................................................................................................................................

8.Amounts paid by a contractor to a subcontractor holding either a business license or contractor's license for performing activities described in Tenn. Code Ann. Section

complete Schedule B and file with the return......................................................................................

Federal and Tennessee privilege and excise taxes:

(3)

.00

.00

(4)

.00

.00

(5)

.00

.00

(6)

.00

.00

(7)

.00

.00

(8)

.00

.00

(Note: All deductions must have adequate records maintained to substantiate deductions claimed or they will be disallowed.)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

...............................................................................................9. Federal and Tennessee gasoline tax |

(9) |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

10. |

Federal and Tennessee motor fuel tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

(10) |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

||

11. |

Federal and Tennessee tobacco tax on cigarettes |

(11) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||

12. Federal and Tennessee tobacco tax on all other tobacco products |

(12) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13.Federal and Tennessee beer tax....................................................................................................

14.Tennessee special tax on petroleum products........................................................

15.Tennessee liquified gas tax for certain motor vehicles..............................................

16.Tennessee beer wholesale tax..........................................................................................................

17.Other deductions not taken elsewhere on the return.........................................................................

(Specify)

18. Total Deductions. Add Lines 1 through 17. Enter here and in Page 1, Line 2 |

(18) |

(13)

.00

.00

(14)

.00

.00

(15)

.00

.00

(16)

.00

.00

(17)

.00

.00

.00

.00

CLASSIFICATION |

RETAILER RATES |

WHOLESALER RATES |

TAX PERIOD |

DUE DATE |

Class 1A |

0.001 |

0.00025 |

|

|

Class 1B & 1C |

0.001 |

0.000375 |

|

Not later than the |

Class 1D |

0.0005 |

Notapplicable |

|

15th day of the 4th |

Class 1E |

Notapplicable |

0.0003125 |

Fiscal Year |

month following the |

Class 2 |

0.0015 |

0.000375 |

|

end of the tax |

Class 3 |

0.001875 |

0.000375 |

|

period. |

Class 4 |

0.001 |

Not applicable |

|

|

Class 5 |

0.003 |

Not applicable |

|

|

|

|

|

|

|

Document Data

| Fact | Detail |

|---|---|

| 1. Form Designation | Tennessee BUS 416 |

| 2. Form Title | Municipal Business Tax Return |

| 3. Issuing Authority | Tennessee Department of Revenue |

| 4. Revision Date | September 2015 (09-15) |

| 5. Legal Framework | Governs the filing of business taxes within Tennessee |

| 6. Required Information | Filing Period, Account No., FEIN/SSN/TIN, Business License No., and due date, among others |

| 7. Amendment and Closure Declaration | Options to indicate if the return is an amended version or for a closed business |

| 8. Payment Recipient | Check payable to Tennessee Department of Revenue |

| 9. Supporting Schedules | Schedule A for Deductions from Gross Sales and requirement for adequate records |

| 10. Tax Rate Classes and Due Dates | Multiple classes with specific rates for retailers and wholesalers; due not later than the 15th day of the 4th month following the end of the tax period |

Detailed Guide for Using Tennessee Bus 416

To successfully complete the Tennessee Bus 416 form—a Municipal Business Tax Return—it's important to follow the procedures meticulously. Upon finishing this form, you will make checks payable to the Tennessee Department of Revenue and mail your submission to the specified address. Additionally, ensure to check the appropriate boxes if you're filing an amended return or for a closed business. Every detail matters to ensure accurate processing of your business tax obligations.

- Start by identifying the filing period for your return and enter the account number assigned to your business.

- Provide your Federal Employer Identification Number (FEIN), Social Security Number (SSN), or Individual Taxpayer Identification Number (TIN), depending on what's applicable to your business.

- Fill in your business license number.

- Note the due date for the form and fill in your business's location address as requested.

- Check the appropriate box to indicate if this is an amended return or if it's a return for a closed business.

- Select your character of seller: wholesaler or retailer. Only one can be chosen.

- For the business tax jurisdiction, specify the name of the city your business is located in. Remember, if your business is within a city’s limits, you might be required to file two tax returns.

- Enter your total gross sales, excluding sales tax, in the designated area.

- Refer to Schedule A to calculate and enter your allowable deductions.

- Subtract the amount in Step 9 from your total gross sales to calculate your taxable gross sales. Enter this amount accordingly.

- Determine your business tax by applying the appropriate rate for retailers or wholesalers to the taxable gross sales amount and enter it.

- Enter the deduction amount for personal property taxes, which cannot exceed 50% of the amount calculated in the previous step.

- Calculate the total tax due, ensuring the amount entered is the result or $22, whichever is greater.

- Enter any credit memo balances you have.

- Review the instructions to determine the penalty amount, if applicable, and enter it.

- Calculate the interest due for taxes unpaid by the due date, using the specified percentage rate per annum, and fill it in.

- Add the total tax due, the penalty, and interest, then subtract any credit memo balances to determine the total amount owed. Enter this final total.

- Complete Schedule A by listing deductions from gross sales, ensuring you maintain adequate records for all deductions claimed.

- Sign and date the return in the designated areas for the President, Principal Officer, Partner, or Proprietor, and the Tax Return Preparer, if applicable.

After completing all the necessary steps, recheck your entries for accuracy. Make your check payable to the Tennessee Department of Revenue. Mail the completed form and your payment to the address listed on the form. This careful attention to detail and adherence to the instructions will help ensure that your business tax responsibilities are met accurately and in a timely manner.

Important Questions on This Form

What is the Tennessee Bus 416 form used for?

The Tennessee Bus 416 form, officially titled "Municipal Business Tax Return," is a document that businesses operating in Tennessee must submit to the Department of Revenue. It is used to calculate and report business taxes owed based on the company's gross sales, less any allowable deductions. This form is essential for both wholesalers and retailers and must be filed by the deadline to avoid penalties. The form also includes provisions for those amending a previous return or reporting the closure of a business.

Who needs to file the Tennessee Bus 416 form?

This form must be filed by businesses that are physically located within Tennessee cities that impose a business tax. This includes wholesalers and retailers alike. Notably, a taxpayer operating within a city's limits may be required to file two business tax returns, one for the city and another for the state, depending on local regulations and the specific obligations of the business. It's essential for business owners to understand their filing requirements to ensure compliance with state tax laws.

When is the Tennessee Bus 416 form due?

The due date for filing the Tennessee Bus 416 form falls on the 15th day of the 4th month following the end of the business's fiscal year. This timing allows businesses to organize their financial statements and calculate the taxes due accurately. Failing to meet this deadline can result in penalties and interest charges, so timely filing is crucial for all businesses covered under this requirement.

What deductions can be claimed on the Tennessee Bus 416 form?

Deductions play a significant role in determining the amount of business tax owed. The Tennessee Bus 416 form outlines several permissible deductions, including:

- Sales of services to customers located outside Tennessee.

- Returned merchandise with a refunded sales price.

- Sales in interstate commerce where the purchaser takes possession outside Tennessee.

- Cash discounts allowed and taken on sales.

- Repossessed items, specifically the unpaid principal balance in excess of $500 on tangible personal property.

- The trade-in value for any articles sold.

- Bad debts written off during the reporting period and eligible for deduction for federal income tax purposes.

- Payments to subcontractors holding a business or contractor's license for eligible activities.

Additionally, several specific taxes like federal and Tennessee gasoline, motor fuel, tobacco, beer, special tax on petroleum products, liquified gas tax for certain motor vehicles, and beer wholesale tax can also be deducted. Proof for all deductions must be maintained as inadequate documentation may lead to disallowances.

Common mistakes

Filling out tax forms accurately is crucial for compliance and avoiding unnecessary mistakes that can lead to penalties or delays. The Tennessee Department of Revenue Municipal Business Tax Return, commonly referred to as the BUS 416 form, is no exception. Here are ten common mistakes people make when completing this form:

- Not checking the box for an amended return or a closed business: It's essential to indicate if you're filing an amended return or if your business has closed. Failing to do so might confuse the processing of your return.

- Incorrectly reporting total gross sales: A frequent error is not properly excluding sales tax from the total gross sales figure. This can result in an inflated tax liability.

- Miscalculating deductions: Deductions must be accurately entered from Schedule A, Line 18. Overlooking or wrongly calculating these can affect your taxable gross sales.

- Applying the wrong business tax rate: Retailers and wholesalers have different rates, and it's a common mistake to apply the incorrect rate to your taxable gross sales.

- Exceeding the personal property tax deduction: The deduction for personal property taxes cannot exceed 50% of the business tax calculated. Not adhering to this rule is a common oversight.

- Failing to claim or incorrectly calculating credit memo balances: This can lead to overstating your tax due.

- Inaccurately assessing penalty and interest: Penalties and interest apply for late submissions, and inaccuracies here can either inflate your liability or result in underpayment.

- Omitting necessary signatures: The form requires signatures from the president, principal officer, partner, or proprietor, and, if applicable, the tax return preparer. Missing signatures can delay processing.

- Not maintaining adequate records for deductions: All deductions need supporting documentation. Failure to do so can lead to disqualification of these deductions.

- Misclassifying the nature of the seller: Specifying whether you are a retailer or wholesaler is pivotal because it affects the tax rate applied. Misclassification can lead to incorrect tax calculations.

To avoid these and other mistakes, it's essential to:

- Read instructions carefully before filling out the form.

- Double-check all entries, especially calculations and classifications.

- Maintain updated and accurate financial records.

- Consult with a professional if you're unsure about any aspect of the form.

In summary, paying close attention to detail, double-checking your work, and seeking professional advice when necessary can help ensure your BUS 416 form is filled out correctly. This not only aids in maintaining compliance with Tennessee's tax requirements but also helps avoid potential penalties or audits.

Documents used along the form

Completing the Tennessee BUS 416 form, a key document for the state's Department of Revenue, requires accuracy and completeness to ensure compliance with municipal business tax obligations. Besides the BUS 416 form, several other forms and documents are essential in facilitating full compliance with tax regulations and supporting business operations in Tennessee. These documents range from tax-specific forms to broader business documents necessary for accurate reporting and legal operation.

- Schedule A Deductions: This detailed list accompanies the BUS 416 form, outlining deductible items such as sales of services to out-of-state customers, returned merchandise, interstate commerce sales, and other allowed deductions, ensuring accurate taxable gross sales calculation.

- Business Tax Application: Before filing taxes, businesses must register with the Tennessee Department of Revenue, requiring a business tax application to obtain a business license and account number for tax purposes.

- Schedule B: Specifically required for contractors who pay subcontractors for work performed. This schedule is necessary for those seeking to claim deductions for such payments on their BUS 412 form.

- Personal Property Tax Return: Businesses may deduct a portion of their personal property taxes on the BUS 416 form. To do so, they must first file a Personal Property Tax Return with their county's assessor's office.

- Annual Report: Required by the Tennessee Secretary of State, this report maintains a business's active status and is essential for updated and accurate company information, which can affect tax filings.

Federal Tax Return: While not directly tied to the BUS 416 form, a copy of the business’s federal tax return may be necessary to substantiate income and deductions reported to the State of Tennessee. - Employer's Quarterly Federal Tax Return (Form 941): Businesses with employees must file this form to report federal withholdings, Social Security, and Medicare taxes, which can affect state tax liabilities and credits.

Each of these documents plays a crucial role in ensuring that businesses meet their legal obligations and provide the necessary information for tax purposes. Together, they form a comprehensive suite of documents that support the Tennessee BUS 416 form, helping businesses to navigate the complexities of tax reporting and compliance effectively.

Similar forms

The IRS Form 1040 for individual income tax returns has a shared essence with the Tennessee Bus 416 form, primarily in their core purpose of calculating and reporting due taxes. Both documents guide the taxpayer through a series of income statements, allowable deductions, and credits to determine the final tax obligation. They are structured to lead the filer step by step, ensuring accuracy and compliance with tax laws, allowing deductions (such as personal property taxes on the BUS 416 and standard deductions or itemized deductions on the Form 1040) to reduce the taxable amount, thereby influencing the final calculation of taxes owed.

Similarly, the Schedule C (Form 1040), Profit or Loss from Business (Sole Proprietorship), mirrors the Tennessee Bus 416 in that both are geared toward business-related financial activities. Each form requires the business owner to report gross receipts or sales, subtract allowable expenses, and arrive at the net profit or loss for the tax period. Deductions for expenses such as cost of goods sold, and other business expenses are critical in both documents for accurately calculating the tax due or refundable to the business owner, showcasing their focus on business operational financial reporting.

The Uniform Commercial Code (UCC) financing statement, though more specialized, shares a connection with the BUS 416 form through its role in the registration and notification process within a business's financial operation. While the UCC filing declares a secured interest in a debtor's assets to the public, the BUS 416 form declares taxable business activities to the state revenue department. Both serve crucial regulatory compliance functions, ensuring transparency and proper financial conduct of businesses within their respective frameworks.

The State of Tennessee Business License Application bears resemblance to the BUS 416 in that both documents are fundamental to the business regulatory and financial framework within the state. Each requires critical business information, such as business name, location, and nature of business, to ensure compliance with state regulations and taxation requirements. While the business license application is a prerequisite for legally conducting business, the BUS 416 form is a requisite for fulfilling tax liabilities, marking their importance in the establishment and maintenance of a business’s legal and tax status in Tennessee.

Dos and Don'ts

When dealing with the Tennessee Department of Revenue Municipal Business Tax Return, identified as the BUS 416 form, properly completing and submitting this document is crucial for compliance and to potentially avoid penalties. Below are key do's and don'ts to consider:

Do's- Ensure accuracy: Double-check all the information you provide, such as total gross sales, deductions, and business tax calculations, to avoid common mistakes.

- Round to the nearest dollar: As instructed on the form, round all amounts to the nearest dollar to keep calculations simple and consistent.

- Select the correct character of seller: Whether you're a wholesaler or retailer, selecting the correct option is critical for accurate tax assessment.

- Include deductions: Carefully review and include eligible deductions from Schedule A, ensuring you maintain adequate records to substantiate these deductions.

- Calculate taxes and fees accurately: Use the provided rates and calculation instructions for your specific classification to determine the business tax, penalties, and interest accurately, if applicable.

- Sign and date the return: A signature is required from either the president, principal officer, partner, or proprietor, as well as from the tax return preparer, if applicable.

- Contact for assistance if necessary: If you encounter any issues or have questions, utilize the provided contact information for the Taxpayer Services Division.

- Ignore the due date: Ensure submission by the specified due date to avoid late penalties and interest charges.

- Forget to check applicable boxes for amended or closed businesses: If filing an amended return or for a closed business, failing to check the appropriate box can lead to processing errors.

- Leave fields blank: Instead of leaving a field blank, enter "N/A" or "0" to indicate that the section does not apply or there is nothing to report.

- Neglect to make the check payable correctly: All payments should be made payable to the Tennessee Department of Revenue, as stated on the form.

- Omit personal property tax deduction: If eligible, do not overlook the deduction for personal property taxes, which cannot exceed 50% of the business tax amount.

- Fail to attach Schedule A or B when necessary: If deducting amounts that require detailed information on Schedules A or B, make sure these are completed and attached.

- Incorrectly calculate total amount due: To determine the total amount you owe, add the calculated tax due, penalties, and interest, then subtract any credit memo balances.

Misconceptions

There are several common misconceptions about the Tennessee Bus 416 form, a municipal business tax return, which can lead to confusion for those filing it. Understanding these misconceptions is crucial for accurate and timely submissions.

Misconception 1: The form is only for retail businesses.

One widespread misconception is that the Tennessee Bus 416 form is exclusively for retail businesses. This misunderstanding stems from the classification section of the form, which requires the character of the seller to be listed as either a wholesaler or retailer. However, the truth is that both wholesalers and retailers use this form to report and pay their municipal business taxes, a requirement underscored by different tax rates applicable to each classification provided in the document.

Misconception 2: Amended returns and returns for closed businesses are filed differently.

Another mistaken belief is that amended returns and returns for closed businesses need to be filed through a distinct process or on a different form. On the contrary, the Bus 416 form includes specific checkboxes for indicating whether the submission is an amended return or for a business that has closed. This feature simplifies the process, ensuring all business types utilize the same form, fostering a streamlined approach to filing.

Misconception 3: Sales tax must be included in the total gross sales.

Many filers incorrectly assume that they must include the sales tax collected from customers in their total gross sales figure. This incorrect assumption can result in overestimation of gross sales. Importantly, the form specifically instructs taxpayers to exclude sales tax from the total gross sales amount, aiming to calculate the tax base accurately. Understanding this can prevent errors and potential overpayment of taxes.

Misconception 4: Deductions are limited to bad debts and returned merchandise.

Finally, a common misconception is that the only deductions allowed on the Bus 416 form are for bad debts and returned merchandise. In reality, the form’s Schedule A details a broader range of deductible items, including sales of services to out-of-state customers, sales in interstate commerce, cash discounts, repossessions, and trade-ins, among others. Recognizing the extent of permitted deductions is vital for businesses to accurately report their taxable gross sales and minimize their tax liability appropriately.

Correctly understanding these aspects of the Tennessee Bus 428 form can greatly assist businesses in fulfilling their tax obligations accurately and efficiently.

Key takeaways

Filling out and using the Tennessee BUS 416 form, a Municipal Business Tax Return, is essential for businesses operational within the state. This document is designed to ensure that businesses comply with local tax regulations, making its correct completion a priority. Here are key takeaways that can help in navigating through the process:

- The BUS 416 form is used specifically by businesses to report and pay municipal tax to the Tennessee Department of Revenue. Whether you're a wholesaler or a retailer, this form plays a critical role in your business tax filings.

- Businesses should pay close attention to the filing period, account number, FEIN/SSN/TIN, and business license number sections at the top of the form to avoid processing delays.

- When preparing to pay taxes, make sure your checks are made payable to the Tennessee Department of Revenue. It's also crucial to mail the form to the correct address provided on the form to ensure it reaches the intended department without any hiccups.

- If filing for an amended return or reporting a closed business, specific boxes need to be checked to inform the Department of Revenue of these circumstances. These small but significant details help in processing your return accurately.

- Understanding the calculation of your tax obligations, including deductions, tax rates, penalties, and interests, is essential. The form requires detailing gross sales, taxable gross sales after deductions, and applying the correct tax rate based on your classification as a retailer or wholesaler. Additionally, keeping meticulous records to substantiate any deductions claimed is paramount.

For assistance with the form, taxpayers are encouraged to contact the Taxpayer Services Division. Whether filing for the first time or an experienced business owner, taking advantage of the resources and support offered by the Tennessee Department of Revenue can streamline the tax filing process.

Create Other Documents

How to File a Notice of Completion in California - This form is used in Tennessee by corporations to officially announce the completion of improvements on a property they own.

Articles of Organization Tennessee - Valuation of gifts must represent their full and true value as of the date the gift was made.