Get Tennessee Bus 415 Template in PDF

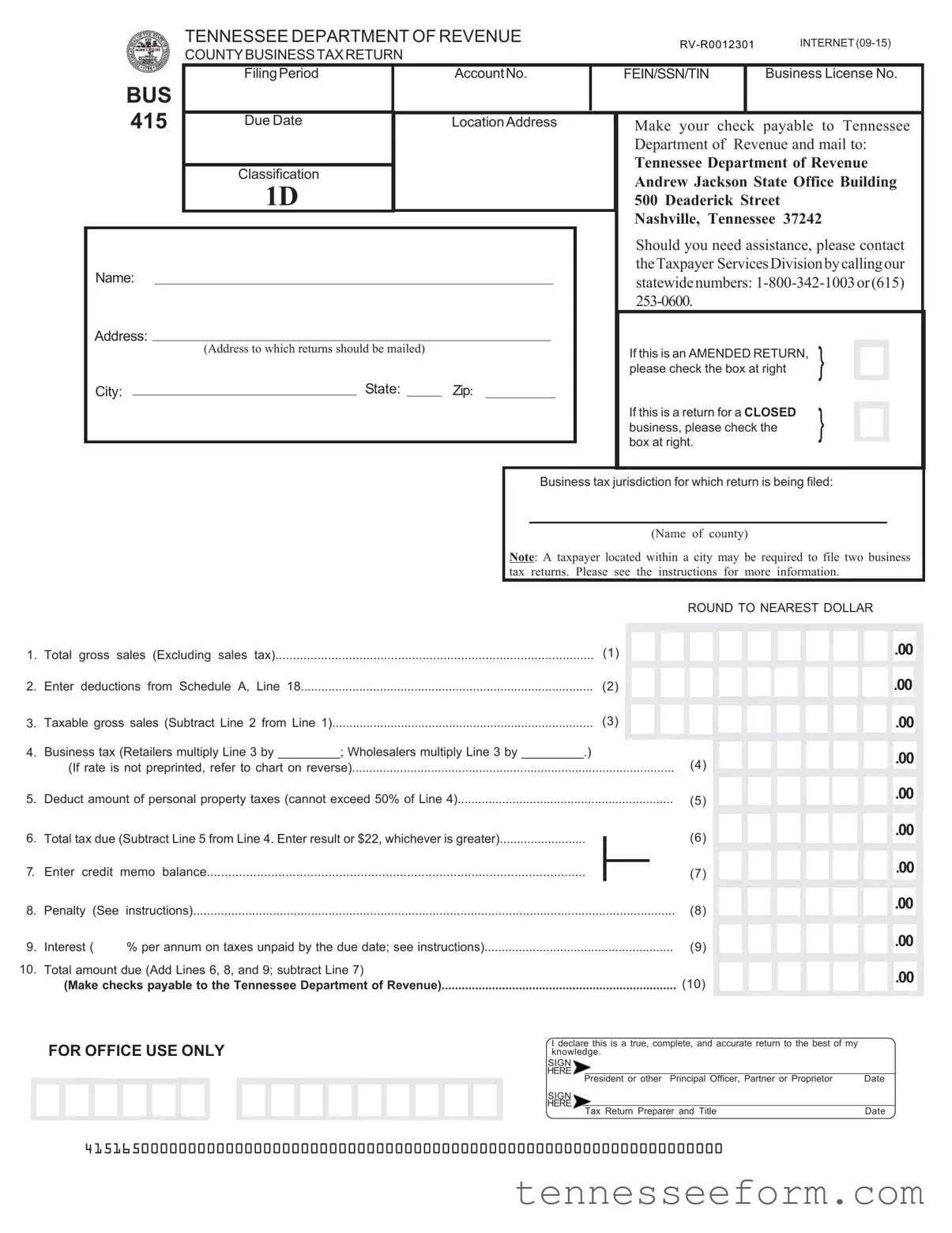

In the landscape of business regulation within Tennessee, the Tennessee Department of Revenue's BUS 415 form serves as a crucial document for business entities operating within the state. This form, titled the County Business Tax Return, is tasked with the role of reporting and computing the dues owed by businesses under the state's business tax statutes. Designed to streamline the reporting process, the BUS 415 form mandates the disclosure of total gross sales, while also allowing for certain deductions—such as returned merchandise or sales eligible for interstate commerce exemptions—to be subtracted, leading to the calculation of taxable gross sales. Critical to this process are the rates applied to retailers and wholesalers, which are contingent upon the business's classification, as specified within the document. The capability to adjust the business tax liability with personal property taxes, subject to limitations, introduces an additional layer of complexity. Furthermore, the form facilitates amendments and adjustments for closed businesses, thereby accommodating changes in business status. Penalties and interest provisions underscore the importance of adherence to deadlines and accuracy in reporting. Accompanied by detailed instructions and ancillary schedules, including a comprehensive list of allowable deductions and a directive for calculating taxes owed, the BUS 415 form encapsulates a comprehensive fiscal responsibility framework, ultimately culminating in the payable amount to the Tennessee Department of Revenue. This encapsulation not only necessitates meticulous record-keeping and a deep understanding of applicable deductions but also underscores the interconnectedness of state regulation and business operations.

Document Preview Example

TENNESSEE DEPARTMENT OF REVENUE

COUNTYBUSINESSTAXRETURN

|

|

FilingPeriod |

|

AccountNo. |

|

|

FEIN/SSN/TIN |

|

Business License No. |

|

|||||||||||||||||||

|

BUS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

415 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Due Date |

|

LocationAddress |

|

|

|

|

Make your |

check payable |

to Tennessee |

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

Department of Revenue and mail to: |

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

Tennessee Department of Revenue |

|

|||||||||||||||||

|

|

Classification |

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

Andrew Jackson State Office Building |

|

||||||||||||||||||

|

|

1D |

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

500 Deaderick Street |

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

Nashville, Tennessee 37242 |

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

Should you need assistance, please contact |

|

|||||||||||||||||

|

Name: _________________________________________________________ |

|

|

|

|

theTaxpayer ServicesDivisionbycallingour |

|

||||||||||||||||||||||

|

|

|

|

|

statewidenumbers: |

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Address: _________________________________________________________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

(Address to which returns should be mailed) |

|

|

|

|

|

|

If this is an AMENDED RETURN, |

} |

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

please check the box at right |

|

|

|

|

|

|

|

||||||||||||

|

City: ________________________________ State: _____ |

Zip: __________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

If this is a return for a CLOSED |

} |

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

business, please check the |

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

box at right. |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business tax jurisdiction for which return is being filed: |

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

(Name of county) |

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

Note: A taxpayer located within a city may be required to file two business |

|

|||||||||||||||||||||||

|

|

|

|

|

tax returns. Please see the instructions |

for more information. |

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ROUND TO NEAREST DOLLAR |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. Total gross sales (Excluding sales tax) |

|

|

(1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. Enter deductions from Schedule A, Line 18 |

|

|

(2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

||||||

|

............................................................................ |

|

|

|

|

(3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

3. Taxable gross sales (Subtract Line 2 from Line 1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Business tax (Retailers multiply Line 3 by _________; Wholesalers multiply Line 3 by _________.) |

|

|

|

|

|

(If rate is not preprinted, refer to chart on reverse) |

(4) |

|||

5. |

Deduct amount of personal property taxes (cannot exceed 50% of Line 4) |

(5) |

|||

6. |

Total tax due (Subtract Line 5 from Line 4. Enter result or $22, whichever is greater) |

|

(6) |

||

|

|||||

7. |

Enter credit |

memo balance |

|

|

|

|

(7) |

||||

8. |

Penalty (See |

instructions) |

|||

9. |

Interest ( |

% per annum on taxes unpaid by the due date; see instructions) |

(9) |

||

10. |

Total amount due (Add Lines 6, 8, and 9; subtract Line 7) |

|

|

|

|

|

(Make checks payable to the Tennessee Department of Revenue) |

(10) |

|||

.00

.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

%.00

FOR OFFICE USE ONLY

I declare this is a true, complete, and accurate return to the best of my knowledge.

SIGN

HERE

|

President or other Principal Officer, Partner or Proprietor |

Date |

|

SIGN |

|

||

HERE |

|

|

|

Tax Return Preparer and Title |

Date |

||

|

|||

41516500000000000000000000000000000000000000000000000000000000000000

INTERNET

Schedule A. Deductions from Gross Sales |

|

1. Sales of services received by persons located in other states |

(1) |

2. Returned merchandise when the sales price is refunded to the customer |

(2) |

.00

.00

.00

.00

3.Sales in interstate commerce where the purchaser takes possession outside Tennessee for use or consumption outside Tennessee.......................................................................................................

4.Cash discounts allowed and taken on sales.......................................................................................

5.Repossessions - The portion of the unpaid principal balance in excess of $500 due on tangible per- sonal property repossessed from customers.......................................................................................

6.The amount allowed as

7.Bad debts written off during the reporting period and eligible to be deducted for federal income tax purposes.........................................................................................................................................

8.Amounts paid by a contractor to a subcontractor holding either a business license or contractor's license for performing activities described in Tenn. Code Ann. Section

complete Schedule B and file with the return......................................................................................

Federal and Tennessee privilege and excise taxes:

(3)

.00

.00

(4)

.00

.00

(5)

.00

.00

(6)

.00

.00

(7)

.00

.00

(8)

.00

.00

(Note: All deductions must have adequate records maintained to substantiate deductions claimed or they will be disallowed.)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

...............................................................................................9. Federal and Tennessee gasoline tax |

(9) |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

10. |

Federal and Tennessee motor fuel tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

(10) |

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

||

11. |

Federal and Tennessee tobacco tax on cigarettes |

(11) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||

12. Federal and Tennessee tobacco tax on all other tobacco products |

(12) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13.Federal and Tennessee beer tax....................................................................................................

14.Tennessee special tax on petroleum products........................................................

15.Tennessee liquified gas tax for certain motor vehicles..............................................

16.Tennessee beer wholesale tax..........................................................................................................

17.Other deductions not taken elsewhere on the return.........................................................................

(Specify)

18. Total Deductions. Add Lines 1 through 17. Enter here and in Page 1, Line 2 |

(18) |

(13)

.00

.00

(14)

.00

.00

(15)

.00

.00

(16)

.00

.00

(17)

.00

.00

.00

.00

CLASSIFICATION |

RETAILER RATES |

WHOLESALER RATES |

TAX PERIOD |

DUE DATE |

Class 1A |

0.001 |

0.00025 |

|

|

Class 1B & 1C |

0.001 |

0.000375 |

|

Not later than the |

Class 1D |

0.0005 |

Notapplicable |

|

15th day of the 4th |

Class 1E |

Notapplicable |

0.0003125 |

Fiscal Year |

month following the |

Class 2 |

0.0015 |

0.000375 |

|

end of the tax |

Class 3 |

0.001875 |

0.000375 |

|

period. |

Class 4 |

0.001 |

Not applicable |

|

|

Class 5 |

0.003 |

Not applicable |

|

|

|

|

|

|

|

Document Data

| Fact Name | Description |

|---|---|

| Form Identification | Tennessee Department of Revenue County Business Tax Return, Form BUS 415 |

| Governing Law | Tennessee Code Annotated (Tenn. Code Ann.) includes laws relevant to the business tax obligations covered by this form. |

| Document Version | Internet (09-15), indicating a revision or issue date of September 2015. |

| Payment Recipient | Make checks payable to the Tennessee Department of Revenue. |

| Mailing Address | Andrew Jackson State Office Building 1D, 500 Deaderick Street, Nashville, Tennessee 37242 |

| Contact Information | Taxpayer Services Division can be reached at 1-800-342-1003 or (615) 253-0600 for assistance. |

| Amended or Closed Business Return Indication | Options to indicate if the form is for an amended return or for a closed business are provided. |

| Reporting Requirements | A taxpayer located within a city may need to file two business tax returns, one for the city and one for the county. |

| Schedule A Inclusions | Details deductions from gross sales, including sales of services to out-of-state customers, returned merchandise, and other specific deductions eligible under state tax law. |

| Tax Rates and Classifications | Lists retail and wholesaler rates for various classes, indicating differentiated tax rates based on business type and activities as defined in Tennessee tax legislation. |

Detailed Guide for Using Tennessee Bus 415

Preparing the Tennessee Bus 415 form is an essential task for businesses operating within Tennessee, aimed at properly reporting their business tax obligations to the Tennessee Department of Revenue. This document must be filled out accurately to reflect the business activities within the specified filing period. Below are detailed steps to guide you through the process of completing the form.

- Start by entering the filing period and account number in the designated fields at the top of the form.

- Provide the Federal Employer Identification Number (FEIN), Social Security Number (SSN), or Taxpayer Identification Number (TIN), alongside your Business License Number.

- Indicate the due date as specified by the form and fill in the business location address accurately.

- If you are amending a return or reporting for a closed business, check the appropriate box located near the top of the form.

- Write down the name of the county for the business tax jurisdiction. Remember, if your business is within a city's limits, you might need to file two separate returns.

- For Total Gross Sales, exclude sales tax and enter the amount on Line 1.

- Calculate and enter on Line 2 the deductible amounts from Schedule A, Line 18.

- Subtract the amount on Line 2 from Line 1 to find your Taxable Gross Sales and enter the result on Line 3.

- Depending on your classification as a retailer or wholes har, multiply your Taxable Gross Sales by the appropriate rate indicated at the bottom of the form and enter this on Line 4.

- Deduct any applicable amount of personal property taxes from Line 4, ensuring it does not exceed 50% of the business tax, and enter this on Line 5. Enter the total tax due on Line 6.

- If applicable, record any credit memo balance on Line 7.

- Refer to the instructions for details on calculating penalties and interest, if any, and fill in Lines 8 and 9 as appropriate.

- Add Lines 6, 8, and 9 then subtract Line 7 to find the Total Amount Due, and enter this on Line 10.

- Complete the bottom section with the signature of the President, Principal Officer, Partner, or Proprietor and the Tax Return Preparer, along with the date.

- Lastly, include any applicable deductions in Schedule A. Make sure to have records to substantiate these deductions as needed.

Once you have completed filling out the form and Schedule A, make your check payable to the Tennessee Department of Revenue and mail the form to the address provided on the form. It is crucial to ensure that all the information provided is accurate and complete to avoid any potential issues. This step is important in fulfilling your business tax obligations and maintaining compliance with Tennessee law.

Important Questions on This Form

What is the Tennessee Bus 415 form and who needs to file it?

The Tennessee Bus 415 form is a document utilized by the Tennessee Department of Revenue for business tax returns at the county level. It is mandatory for businesses operating within Tennessee to file this form if they are engaging in taxable sales. The necessity to file can mean preparing one or more business tax returns, contingent on whether the business is located within both a city and a county jurisdiction that mandates tax filing. The purpose of the form is to calculate and report the amount of business tax owed to the state based on the business’s gross sales after deductions.

How does a business determine the applicable tax rate for the Bus 415 form?

To accurately determine the applicable tax rate for filing the Bus 415 form, a business must identify its classification based on the type of goods or services it provides. The form outlines different rates for retailers and wholesalers across various classifications (e.g., Class 1A, Class 2) and the specific tax rate applicable to each class. These rates are crucial for calculating the taxable gross sales, from which the business tax due is derived. Businesses should refer to the reverse side of the form or consult with the Tennessee Department of Revenue to ensure they apply the correct rate to their taxable gross sales.

What deductions can be taken when completing the Bus 415 form?

When completing the Bus 415 form, businesses are allowed to deduct certain amounts from their gross sales to calculate the taxable gross sales. These deductions include:

- Sales of services received by persons located in other states.

- Returned merchandise with the sales price refunded to the customer.

- Sales in interstate commerce where the purchaser takes possession outside Tennessee.

- Cash discounts allowed and taken on sales.

- Repossessions over a certain value.

- Trade-in value for articles sold.

- Bad debts written off and eligible for federal income tax deductions.

Additionally, specific federal and Tennessee taxes paid on gasoline, motor fuel, tobacco products, beer, and certain other items are deductible. However, it's important that businesses maintain adequate records to substantiate all deductions claimed on the form, as failing to do so may result in disallowances.

What steps should be taken if filing an amended return or a return for a closed business using the Bus 415 form?

If a business needs to file an amended return or a return for a closed business, specific boxes need to be checked off on the Bus 415 form to indicate the nature of the filing. For an amended return, the appropriate box near the top of the form is marked to show that the filing corrects previously submitted information. Similarly, if filing for a business that has ceased operations, the box indicating a closed business should be checked. These special conditions inform the Tennessee Department of Revenue of the need to adjust records accordingly. In each case, the rest of the form should be filled out with accurate, up-to-date information reflecting the amendments or the final business activities prior to closure.

Common mistakes

Filling out forms for tax purposes can often be a daunting task, and the Tennessee BUS 415 form is no exception. It requires careful attention to detail, and there are common mistakes people tend to make when completing it. These mistakes can lead to delays in processing, potential penalties, or even incorrect assessment of taxes due.

One of the first mistakes is incorrectly reporting total gross sales. The form explicitly asks for sales excluding sales tax, yet many individuals inadvertently include sales tax in their total. This can significantly alter the taxable amount and the tax computation. It's crucial to carefully exclude any collected sales tax from the gross sales figure reported.

Another common error involves miscalculating deductions. The BUS 415 form permits various deductions from gross sales, such as returned merchandise and sales of services to out-of-state persons. However, filers sometimes either overlook eligible deductions or incorrectly calculate the amounts. This mishap can lead to a higher taxable amount, thereby increasing the tax liability unnecessarily.

Moreover, failing to report or incorrectly calculating the business tax due based on the classification rates provided in the form is a prevalent mistake. Each business classification has a corresponding tax rate, and using the incorrect rate can either inflate or deflate the tax due. This step requires double-checking the business classification and applying the correct rate meticulously.

Additionally, overlooking the personal property tax deduction is another oversight many filers commit. The form allows for a deduction up to 50% of the business tax amount for personal property taxes paid, yet this deduction is frequently missed. Not taking advantage of this allowance results in an inflated tax due.

Last but not least, inaccurately computing the final tax due, penalties, and interest is a common error. This part of the form involves several computations including adding or subtracting amounts from previous lines, and considering credits, penalties, and interest rates. Mathematical errors or misunderstandings of what values to include in these computations can significantly affect the total amount due.

In summary:

- Incorrectly reporting total gross sales by including sales tax.

- Miscalculating deductions that could lower the taxable amount.

- Using the incorrect business classification rate for tax calculation.

- Omitting the personal property tax deduction, leading to an inflated tax liability.

- Making computational errors in the final tax due, including penalties and interest.

To avoid these mistakes, thoroughness and attention to each detail on the form are paramount. When in doubt, consulting with a tax professional or the Tennessee Department of Revenue can provide clarity and ensure the form is completed correctly.

Documents used along the form

When preparing and filing the Tennessee BUS 415 form, a comprehensive approach is crucial for compliance and accuracy. This form, used by businesses for reporting county business tax in Tennessee, often requires supplementary documents to provide complete information on gross sales, deductions, and tax computations. Understanding these additional forms and documents can help ensure a thorough and compliant submission.

- Form SS-4243 (Business Tax Application): Before filing BUS 415, new businesses must use this form to register for a business tax account with the Tennessee Department of Revenue.

- Schedule B (Subcontractor Deductions): Accompanies BUS 415 for businesses deducting payments made to subcontractors, as detailed in the BUS 415 instructions.

- Sales and Use Tax Return: While separate, this return may be necessary for businesses that sell taxable goods and services, providing details on sales tax collected and owed.

- Personal Property Tax Schedule: Required for businesses that must report on personal property tax deductions claimed on BUS 415, it details taxable business assets.

- Form FAE 170 (Franchise and Excise Tax Return): Businesses may need to file this along with BUS 415 if they are subject to Tennessee’s franchise and excise taxes.

- Annual Report: Often filed by corporations and LLCs to the Secretary of State, the annual report may influence business tax liability and thus is relevant when preparing BUS 415.

- Business License Renewal Forms: Depending on the local jurisdiction, businesses might need to provide evidence of business license renewal, which ties into the business tax account status.

- Commercial Lease Agreement: The location address on BUS 415 must match the current lease agreement, which may necessitate verifying and including lease documentation.

- Proof of Tax Exemptions or Credits: Documentation supporting claims for tax exemptions or credits, such as energy-efficient investment credits, which reduce taxable gross sales.

- Bank Statements and Sales Records: Essential for substantiating the gross sales and deductions reported on BUS 415, these records should be maintained and available for review.

Filing the Tennessee BUS 415 form with completeness and accuracy is essential for compliance with state tax obligations. The supplemental forms and documents not only support the information reported but also assist in ensuring that the business meets all regulatory requirements. Careful preparation and documentation can simplify the process, making it more efficient and less prone to errors or oversight. Business owners and tax preparers should remain informed about the necessary documentation to streamline their filing process effectively.

Similar forms

The Schedule C (Form 1040 or 1040-SR), Profit or Loss from Business, often used by sole proprietors and single-member LLCs in the United States, bears similarities to the Tennessee BUS 415 form. Like the BUS 415, which reports gross sales, deductions, and taxable sales for a specific period, the Schedule C also requires detailing the income and expenses of a business, ultimately determining the net profit or loss. Both forms are crucial for accurate tax reporting and ensure businesses comply with their tax obligations, albeit for different tax types and jurisdictions.

The Sales and Use Tax Return employed by many states for reporting collected sales tax from customers parallels the Tennessee BUS 415 form to a degree. This similarity lies in their shared objective of documenting the total sales generated within a reporting period and identifying taxable and non-taxable sales. Each form serves to calculate the tax due on sales, although the BUS 415 focuses on business taxes while the Sales and Use Tax Return centers on sales tax. Additionally, they both allow for deductions that reduce the taxable amount, thereby ensuring tax calculation accuracy.

The Uniform Business Office (UBO) Third Party Collections (TPC) Form, utilized for capturing the reimbursement of medical services from third-party payers, shares a somewhat analogous purpose with the Tennessee BUS 415 form. Although the TPC form pertains specifically to healthcare services and their payment, both documents are instrumental in tracking revenue and ensuring proper payment processing. Moreover, each form mandates detailed entries about the income received, albeit from vastly different sources and for different purposes.

The Business Property Tax Forms, which various local jurisdictions require for the taxation of business-owned property, exhibit parallels with the BUS 415 in terms of tax reporting. These forms assess the value and tax liability of tangible assets owned by businesses, much like how the BUS 415 determines taxation based on business activities and revenue. Both are essential for fair tax administration, ensuring businesses contribute appropriately to local and state revenues according to their operational scale and assets.

Lastly, the Commercial Activity Tax (CAT) Return, specifically in states like Ohio, mirrors the Tennessee BUS 415 form by focusing on the gross receipts of a business. The CAT Return and the BUS 415 both calculate tax obligations based on the revenue scale, albeit through different taxation frameworks (gross receipts versus business tax). Importantly, both forms play a critical role in the broader context of ensuring businesses meet their tax responsibilities, thereby supporting the fiscal infrastructure of their respective jurisdictions.

Dos and Don'ts

Filling out the Tennessee BUS 415 form accurately is crucial for complying with tax obligations. To assist you, here's a list of dos and don'ts to consider:

- Do round all amounts to the nearest dollar as specified in the form instructions to ensure accuracy.

- Do check the box at the top of the form if you are filing an amended return or if the return is for a closed business, so that your submission is processed correctly.

- Do make your check payable to the Tennessee Department of Revenue to avoid any payment issues.

- Do maintain adequate records for all deductions claimed on Schedule A to substantiate them if required, ensuring your compliance and potentially saving time in case of an audit.

- Don't forget to enter your FEIN/SSN/TIN and Business License No., as these identifiers are key to matching your return to your business records accurately.

- Don't neglect to calculate your taxes based on the correct class rate for retailers or wholesalers; using the wrong rate could lead to underpayment or overpayment of taxes.

- Don't underestimate the importance of signing the return before mailing. Unsigned returns may be considered invalid, potentially delaying processing or leading to penalties.

- Don't ignore the due date specified for your classification. Submitting your return late can result in penalties and interest charges that increase your tax liability.

By following these guidelines, you can help ensure that your Tennessee BUS 415 form is correctly completed and submitted, thereby avoiding potential issues with your business tax obligations.

Misconceptions

When it comes to understanding and filing the Tennessee Bus 415 form, there are several misconceptions that can lead to confusion and errors. This form is used by businesses to report and pay county business taxes in Tennessee. Let's clear up some of the most common misunderstandings:

- It's only for retailers: Some believe the BUS 415 form is exclusive to retailers. However, both retailers and wholesalers are required to file it, with different tax rates applicable to each group as outlined in the form's classification and rate section.

- Filing is the same for all businesses: The notion that all businesses follow the same filing process overlooks the fact that businesses may need to file separate returns for different locations, especially if they operate in both a city and county jurisdiction within Tennessee. Consulting the form's instructions can help clarify this specific requirement.

- Sales tax should be included in gross sales: When calculating total gross sales on the form, sales tax should not be included. This common mistake can lead to an inaccurate tax liability calculation. The form specifically asks for total gross sales excluding sales tax.

- All deductions are allowed: There's a misconception that any expense can be deducted on the Bus 415 form. In reality, only specific deductions listed in Schedule A are allowed, such as sales of services to out-of-state customers, returned merchandise, or bad debts written off, among others. Adequate records must be maintained for these deductions.

- Personal property taxes fully deductible: While the form allows for the deduction of a portion of personal property taxes, it cannot exceed 50% of the calculated business tax under line 4. Thinking one can deduct all such taxes can significantly affect the accuracy of the total tax due.

- The form doesn't apply to closed businesses: Another misunderstanding is that once a business is closed, filing this form is unnecessary. However, if a business was operational for any part of the filing period, it is required to submit a final BUS 415 form, checking the box indicating it's a return for a closed business.

Clearing up these misconceptions ensures businesses can accurately report and pay their taxes, avoiding common pitfalls and potential penalties associated with incorrect filing. Proper understanding and compliance with the Tennessee Department of Revenue's requirements play a crucial role in the successful management and operation of businesses within the state.

Key takeaways

Understanding the process and requirements for completing the Tennessee BUS 415 form, or the County Business Tax Return, is crucial for businesses operating within the state. Below are key points to help clarify these procedures:

- Identification Information: Businesses must provide comprehensive identification details at the beginning of the form. This includes the filing period, account number, Federal Employer Identification Number (FEIN), Social Security Number (SSN), or Taxpayer Identification Number (TIN), and the business license number. Additionally, the form requires the business location address.

- Dual Filing for City and County: The form notes that businesses located within a city's limits may be required to file two separate business tax returns, one for the county and another for the city, indicating that businesses should be aware of their filing obligations in both jurisdictions.

- Gross Sales and Deductions: Businesses must report total gross sales, excluding sales tax, and then itemize allowable deductions as per Schedule A. These deductions are subtracted from the gross sales to determine the taxable gross sales amount.

- Calculation of Business Tax: The form requires businesses to calculate their tax due based on their taxable gross sales. Retailers and wholesalers have different rates, and these rates must be applied to the taxable gross amount. Additionally, it allows for a deduction of personal property taxes up to 50% of the business tax calculated.

- Penalties and Interest: If applicable, penalties and interest for late payment must be calculated. The form outlines how to calculate these amounts, emphasizing the importance of timely filing and payment to avoid extra charges.

- Documentation and Signatures: To complete the submission, the form requires signatures from a principal officer of the business and the tax return preparer, if there is one. Moreover, maintaining adequate records to substantiate the deductions claimed is critical, as failure to do so could result in disallowances.

- Amended Returns and Business Closure: The form includes provisions for marking a submission as an amended return or indicating that it is a final return for a closed business. This assists in keeping the state's records accurate and up to date with the business's status.

By meticulously following these guidelines and ensuring accurate and complete information is provided, businesses can fulfill their tax obligations efficiently and comply with Tennessee's tax regulations.

Create Other Documents

Tennessee Ps 0376 - Details on how to complete the application, including supplemental attachments for principal solicitors and affiliates.

Tennessee Sales Tax Exemption Nonprofit - Attention to details such as the Preparer's PTIN and contact information ensures accountability in tax preparation.