Tennessee Promissory Note Document

When individuals or entities in Tennessee decide to lend or borrow money, a crucial step in ensuring clarity and security for both parties involved is the drafting of a promissory note. This legal document, tailored specifically to meet the state's regulations, outlines the vital details of the financial agreement. It includes information such as the amount loaned, the interest rate applied, repayment schedule, and the consequences of non-payment. Beyond its fundamental roles, the Tennessee Promissory Note also serves as a legal record that can be used in court if there's a dispute or if the borrower fails to uphold their end of the deal. It's not just a formality but a key piece of documentation that protects the interests of both the lender and the borrower, ensuring that the terms of their agreement are clear from the outset. Crafting this document carefully is essential to avoid future misunderstandings and legal complications.

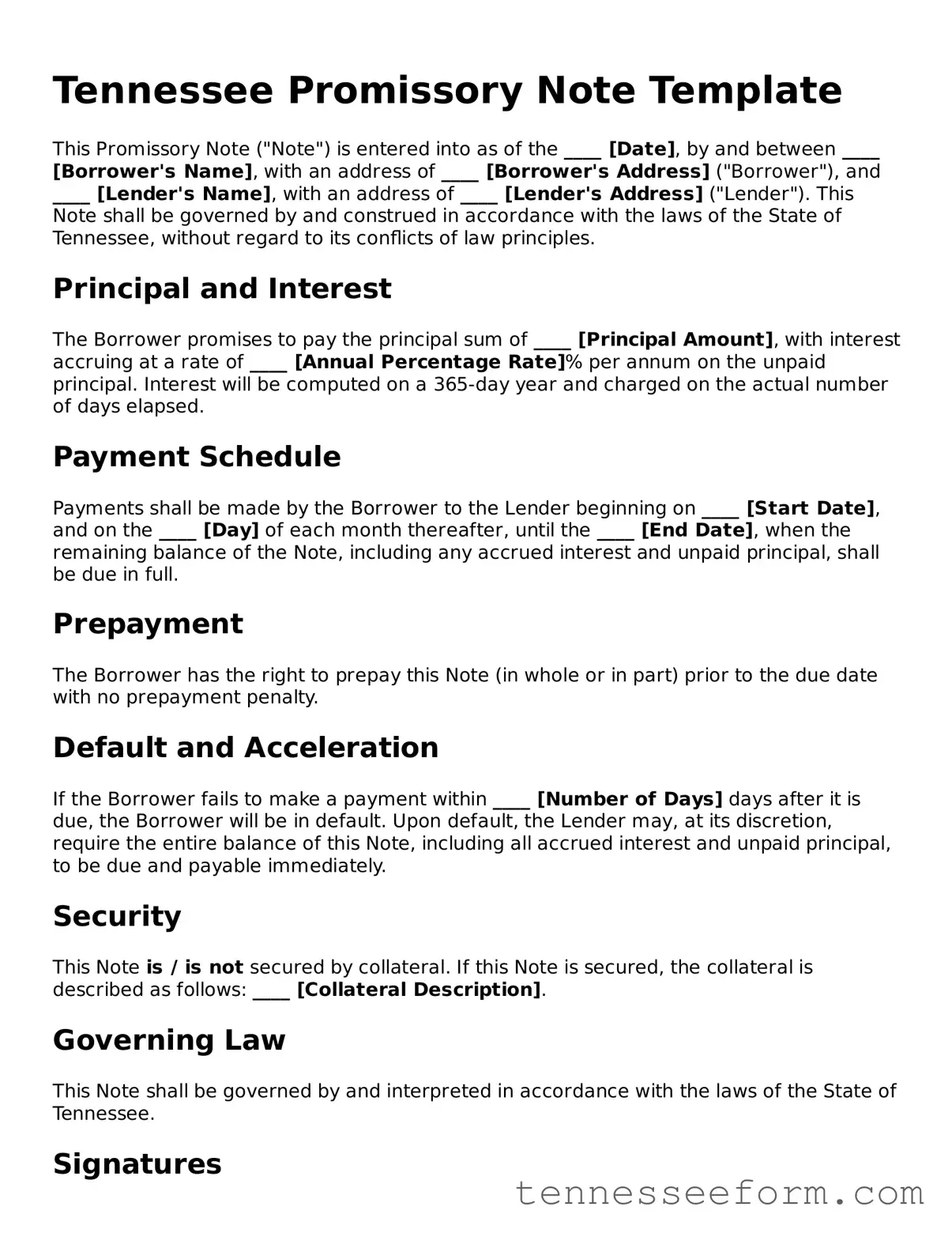

Document Preview Example

Tennessee Promissory Note Template

This Promissory Note ("Note") is entered into as of the ____ [Date], by and between ____ [Borrower's Name], with an address of ____ [Borrower's Address] ("Borrower"), and ____ [Lender's Name], with an address of ____ [Lender's Address] ("Lender"). This Note shall be governed by and construed in accordance with the laws of the State of Tennessee, without regard to its conflicts of law principles.

Principal and Interest

The Borrower promises to pay the principal sum of ____ [Principal Amount], with interest accruing at a rate of ____ [Annual Percentage Rate]% per annum on the unpaid principal. Interest will be computed on a 365-day year and charged on the actual number of days elapsed.

Payment Schedule

Payments shall be made by the Borrower to the Lender beginning on ____ [Start Date], and on the ____ [Day] of each month thereafter, until the ____ [End Date], when the remaining balance of the Note, including any accrued interest and unpaid principal, shall be due in full.

Prepayment

The Borrower has the right to prepay this Note (in whole or in part) prior to the due date with no prepayment penalty.

Default and Acceleration

If the Borrower fails to make a payment within ____ [Number of Days] days after it is due, the Borrower will be in default. Upon default, the Lender may, at its discretion, require the entire balance of this Note, including all accrued interest and unpaid principal, to be due and payable immediately.

Security

This Note is / is not secured by collateral. If this Note is secured, the collateral is described as follows: ____ [Collateral Description].

Governing Law

This Note shall be governed by and interpreted in accordance with the laws of the State of Tennessee.

Signatures

IN WITNESS WHEREOF, the parties have executed this Promissory Note as of the date first above written.

Borrower's Signature: ___________________________

Borrower's Printed Name: ____ [Borrower's Name]

Lender's Signature: _____________________________

Lender's Printed Name: ____ [Lender's Name]

Form Features

| Fact Number | Description |

|---|---|

| 1 | The Tennessee Promissory Note form is governed by the state laws of Tennessee. |

| 2 | It serves as a legal agreement to borrow and repay money. |

| 3 | Two main types exist: secured and unsecured. |

| 4 | In a secured note, the borrower pledges collateral. |

| 5 | An unsecured note does not require collateral. |

| 6 | Interest rates must comply with Tennessee's usury laws. |

| 7 | Co-signers may be used to guarantee the note. |

| 8 | It must be signed by the borrower and any co-signer to be valid. |

| 9 | Default terms should be clearly outlined, including any grace periods and penalties. |

Detailed Guide for Using Tennessee Promissory Note

Filling out a Tennessee Promissory Note form is an essential process for anyone entering a loan agreement in the state. This document, which outlines the promise to repay the borrowed amount, must be filled out carefully to ensure the legal binding of the agreement and to clearly define the terms, including the repayment schedule, interest rate, and the consequences of default. The following steps have been designed to guide individuals through the process, making it as straightforward as possible.

- Begin by clearly printing the full legal names of both the borrower and the lender at the top of the form. Ensure these are the names as they appear on official documents to avoid any confusion or legal issues.

- Specify the principal amount of the loan in U.S. dollars. This is the amount the borrower is agreeing to repay, excluding any interest.

- Write down the interest rate, expressed as an annual percentage. This should be agreed upon by both parties and comply with Tennessee's legal maximum rates to ensure the note's enforceability.

- Choose and detail the repayment schedule. This could be in the form of regular payments (monthly, quarterly, etc.) or a lump sum by a specific date. Check the most appropriate box and fill in any necessary details such as dates and amounts.

- Include any provisions for late fees and missed payments. Specify the amount or percentage that will be charged on late payments and after how many days a payment is considered late.

- Define the collateral, if applicable. For secured loans, describe the property or asset that will be used as security for the loan. This assures the lender of repayment either through regular payments or by claim of the collateral.

- Both the borrower and the lender must sign and date the promissory note. Their signatures legally bind them to the terms outlined in the document.

- For added legal protection, consider having the signatures notarized. While not always necessary, a notary public can certify the authenticity of the signatures, giving the note additional legal weight.

Once the Tennessee Promissory Note form is completed, both parties should keep a copy for their records. This ensures that both the borrower and the lender can refer back to the agreed terms throughout the duration of the loan, safeguarding the interests of both parties. Remember, the note serves as a crucial document in the lending process, laying the foundation for a clear and transparent financial transaction.

Important Questions on This Form

What is a Tennessee Promissory Note and why is it important?

A Tennessee Promissory Note is a legally binding agreement between two parties - a borrower and a lender - where the borrower promises to repay a specified sum of money to the lender by a certain date. This document is vital because it clearly details the loan’s terms, including payment schedules, interest rates, and what happens if the borrower fails to make a payment. In Tennessee, having a written promissory note is crucial for enforcing the terms of the loan and serves as proof of the transaction should there be any disputes or legal issues.

How can you ensure a Tennessee Promissory Note is legally binding?

To ensure a Tennessee Promissory Note is legally binding, follow these steps:

- Include the full legal names and contact information of the borrower and the lender.

- Specify the loan amount and the interest rate. Remember, the interest rate must not exceed the maximum legal rate set by Tennessee law.

- Outline the repayment schedule, including due dates and the final payoff date.

- Both parties must sign and date the document. Witness signatures or a notary public seal can add additional legal weight, though not always required.

Adhering to these steps will help ensure the promissory note meets all legal requirements, making it enforceable in a court of law.

What should you do if the borrower fails to repay the loan as agreed in the Tennessee Promissory Note?

If the borrower fails to repay the loan according to the terms of the Tennessee Promissory Note, the lender has several options:

- Communicate with the borrower to understand the reason for the default and attempt to negotiate a revised repayment plan.

- If renegotiation fails, the lender may send a formal demand letter, reminding the borrower of their obligations and the consequences of non-payment.

- As a last resort, the lender may initiate legal proceedings to enforce the repayment of the loan. This could include filing a lawsuit to recover the outstanding debt plus any legal fees and costs incurred.

It’s important for lenders to carefully consider the impact of these actions and possibly seek legal advice before proceeding.

Can a Tennessee Promissory Note be modified after it’s signed?

Yes, a Tennessee Promissory Note can be modified after it’s signed, but any modifications must be agreed upon by both the borrower and the lender. It’s strongly recommended to document any changes in writing and have both parties sign the amendment. This ensures that the modifications are legally binding and protects both parties if any disputes arise over the new terms. For significant changes, consider drafting a new promissory note to replace the original agreement.

Common mistakes

Filling out a promissory note in the state of Tennessee, like any legal document, necessitates a careful approach to ensure that all parties are protected and the agreement is enforceable. The document is intended to be a formal commitment by a borrower to repay money lent to them, usually with interest. There are common mistakes, however, that can complicate this seemingly straightforward process.

1. Not Specifying the Terms Clearly: One of the primary issues encountered is the failure to specify the loan's terms clearly. This includes the interest rate, repayment schedule, and what happens in case of default. The absence of these details can lead to disputes and legal challenges, making it tougher for the lender to enforce the note.

2. Ignoring State Laws: Tennessee, like each state, has its own legal requirements concerning interest rates (usury laws) and other aspects of a promissory note. Not adhering to these can render the note unenforceable and could potentially lead to legal penalties against the lender for charging excessive interest.

3. Not Including Both Parties’ Full Information: The full names and addresses of both the lender and the borrower need to be included in the promissory note. Omitting this essential information can lead to issues with enforcement, as it might not be clear who the agreement is between.

4. Failing to Sign the Agreement: It might seem obvious, but another common mistake is failing to have the document duly signed by both parties. A promissory note without the signatures of both the borrower and the lender lacks the necessary evidence of agreement and commitment to the terms outlined within it.

5. Not Notarizing the Document: While not always a legal requirement, not notarizing the document can be a critical oversight. Notarization adds an extra layer of authenticity, making the note more likely to hold up in court if there is a dispute. In some cases, not having the note notarized can lead to challenges about its legitimacy.

When drafting a promissory note in Tennessee, it's crucial to pay attention to these common mistakes. By doing so, all parties can ensure that the agreement is clear, enforceable, and compliant with state law. This not only protects the relationship between the lender and borrower but also helps in preventing unnecessary legal complications that might arise from oversights during the creation of the document.

Documents used along the form

When entering into a financial agreement in Tennessee, a Promissory Note is often just the starting point. This document lays out the borrowing terms, but several additional forms and documents might be used alongside it to ensure a comprehensive and secure transaction. These supplementary documents address various aspects of the financial agreement, from providing additional security for the lender to ensuring compliance with state laws.

- Loan Agreement: This document complements the Promissory Note by detailing the loan’s terms and conditions in a more comprehensive manner. It often includes clauses about the responsibilities of both parties, dispute resolution methods, and the consequences of a breach.

- Mortgage or Deed of Trust: For loans secured against real estate, this document is critical. It grants the lender a security interest in the property, allowing them to foreclose if the borrower defaults on their loan obligations.

- Security Agreement: Similar to a Mortgage or Deed of Trust but for personal property, a Security Agreement provides a lender with a security interest in assets other than real estate, such as vehicles or equipment.

- Guaranty: This is an agreement by a third party to assume the debt obligation of the borrower if they default. It provides an additional layer of security for the lender.

- Amendment Agreement: If the terms of the original Promissory Note or related agreements need to be changed, an Amendment Agreement is used. This ensures that all modifications are documented and legally binding.

- Release of Promissory Note: Once the loan is fully repaid, this document is issued by the lender to officially end the borrower's obligation under the Promissory Note.

- Notice of Default: Should the borrower fail to meet their obligations, this document is used to formally notify them of their default and the potential consequences if the situation is not remedied.

Each of these documents plays a vital role in safeguarding the interests of both the borrower and the lender. By understanding the purpose and function of these additional documents, parties in Tennessee can ensure that their financial transactions are structured effectively and legally sound. Together, they create a clear framework within which both lenders and borrowers can operate with confidence.

Similar forms

The Tennessee Promissory Note form shares similarities with a Loan Agreement, mainly in the way both documents outline the terms and conditions of a loan between two parties. While a promissory note is a straightforward agreement where the borrower promises to repay the lender a certain amount of money within a specified period, a loan agreement delves deeper into the specifics of the loan, including collateral requirements, repayment schedules, and what happens in the event of default. Both serve to formalize the loan process and protect the interests of the involved parties.

Comparable to a Mortgage Agreement, the Tennessee Promissory Note often includes provisions related to securing the loan against real property. In a Mortgage Agreement, the borrower transfers an interest in the real property to the lender as security for the repayment of the loan. This process parallels the security features that can be included within a promissory note, ensuring the lender has recourse should the borrower default on their obligations.

Another document resembling the Tennessee Promissory Note is the IOU (I Owe You). Both function as written acknowledgments of debt. However, an IOU is generally more informal and might not include specifics such as repayment dates or interest rates. In contrast, a promissory note typically provides a detailed repayment plan, interest, and what occurs if the borrower fails to meet their obligations, offering more protection and clarity for both lender and borrower.

The Tennessee Promissory Note also has aspects in common with a Bill of Sale, especially in scenarios where personal property is used as security for the loan. While a Bill of Sale transfers ownership of an item from the seller to the buyer and serves as evidence of the transaction, a promissory note secured by collateral mentions the personal property securing the loan, outlining what happens to the property if the borrower defaults.

A Debt Settlement Agreement is another document related to the Tennessee Promissory Note. This agreement is typically used when a debtor is unable to repay their debts under the original terms and negotiates to settle the debt for a lesser amount. Like a promissory note, it outlines the terms of debt repayment, but it is specifically oriented towards reducing the borrower's debt and providing a framework for repayment that deviates from the original terms.

The Tennessee Promissory Note also shares similarities with a Personal Guarantee. In situations where additional assurance is needed for the repayment of the loan, a third party may provide a personal guarantee to the lender. While a promissory note is an agreement between the lender and borrower regarding the loan itself, a personal guarantee is an assurance from a third party to fulfill the borrower's obligations if they default, providing an additional layer of security to the lender.

Last but not least, a Credit Agreement can be likened to the Tennessee Promissory Note in its basic function of documenting a loan's terms. However, credit agreements are typically more comprehensive, covering a range of credit transactions, facilities, and revolving credits, unlike a promissory note, which generally documents a single loan transaction with defined terms. Both are crucial for outlining the specifics of borrowing arrangements and ensuring clear communication between all parties involved.

Dos and Don'ts

Filling out a Tennessee Promissory Note form requires attention to detail and an understanding of the obligations it creates. Here are things to do and not do to ensure the process is carried out correctly:

Things You Should Do:

Read the form thoroughly to understand all the terms and conditions before you start filling it out.

Include all requested details accurately, such as the full names of both the borrower and the lender, the loan amount, interest rate, and repayment schedule.

Ensure that both parties sign and date the form to make it legally binding. Witnesses or notarization may also be required, depending on the circumstances.

Keep a copy of the fully executed promissory note for each party's records.

Things You Shouldn't Do:

Don't leave any sections blank. If a section doesn't apply, mark it as "N/A" (not applicable) instead of leaving it empty.

Avoid using informal language or terms that might be ambiguous or unclear. Stick to clear, concise language that reflects the agreement accurately.

Don't forget to check if state-specific requirements or clauses need to be included in your promissory note to make it valid in Tennessee.

Refrain from altering the form after it has been signed without the agreement of both parties. Any changes should be documented and included in a new promissory note or an amendment to the original.

Misconceptions

When dealing with the Tennessee Promissory Note form, understanding and clarity are essential. However, various misconceptions surround its use, implications, and requirements. Here, common misunderstandings are addressed to ensure parties involved make informed decisions.

A promissory note is the same as a loan agreement: While both documents are used in lending transactions, a promissory note is a simpler instrument that outlines the borrower's promise to pay back the lender. A loan agreement is more comprehensive, often including additional terms such as collateral and actions in the event of default.

Verbal agreements are sufficient for promissory notes in Tennessee: Tennessee law requires promissory notes to be in writing to be enforceable. Relying on verbal promises can lead to disputes and challenges in proving the terms of the agreement.

Witnesses or notarization are always required: While having a promissory note witnessed or notarized can add a layer of validity and protection, Tennessee law does not always require these steps for the note to be legally binding. However, it is advisable in many scenarios to prevent potential disputes.

Only the borrower needs to sign the promissory note: It is a common belief that only the borrower's signature is required on a promissory note. However, best practices dictate that both the lender and the borrower should sign to ensure enforceability and mutual understanding of the terms.

Promissory notes are only for large financial transactions: People often think promissory notes are used exclusively for significant amounts of money. In reality, they can be used for loans of any size, providing clarity and legal documentation for both small and large transactions.

Any template can be used for a Tennessee promissory note: While templates can provide a starting point, it's critical to ensure that the template complies with Tennessee's specific legal requirements and accurately reflects the terms agreed upon by the parties.

Modifying a promissory note is not possible after signing: Another common belief is that once a promissory note is signed, its terms cannot be modified. However, modifications are possible if all involved parties agree and document the changes accordingly.

Failing to repay a promissory note does not have legal consequences: There is a misconception that promissory notes are informal promises without legal standing. On the contrary, failure to repay according to the note's terms can lead to legal action, including lawsuits and damage to the borrower's credit.

Understanding these aspects of the Tennessee Promissory Note form is crucial for both lenders and borrowers to protect their interests and avoid potential legal complications.

Key takeaways

When considering the Tennessee promissory note form, there are crucial points to keep in mind to ensure its effectiveness and validity. This document is pivotal for lending transactions between two parties and lays down the repayment terms for the borrower to the lender. Here are the key takeaways:

- Understand State Regulations: The Tennessee promissory note must comply with state laws, including interest rates and usury laws to be considered valid and enforceable. Familiarity with these laws is crucial for both lender and borrower.

- Choose Between Secured or Unsecured: Determining whether the promissory note will be secured or unsecured is important. A secured note requires collateral to be pledged by the borrower, offering the lender protection in case of default. An unsecured note does not require collateral, posing a higher risk for the lender.

- Include Detailed Information: The note should clearly identify all parties involved, the principal loan amount, interest rate, and the repayment schedule. Accurate and comprehensive details prevent misunderstandings and provide legal clarity.

- Set a Reasonable Interest Rate: The interest rate must comply with Tennessee’s maximum interest rate laws to avoid being considered usurious. Setting a fair and legal interest rate is essential for the note’s enforceability.

- Define the Repayment Schedule: The document should outline a clear repayment plan, including due dates and any late fees. This schedule helps manage expectations and responsibilities, ensuring a smoother repayment process.

- Signatures are Essential: For the promissory note to be legally binding, it must be signed by both the borrower and the lender. Witnesses or notarization may also be required to enhance the document’s legal standing.

- Keep Records: Both parties should retain a copy of the signed promissory note for their records. This document serves as proof of the loan terms and agreement, useful for resolving any future disputes.

Find Popular Templates for Tennessee

Tennessee Purchase and Sale Agreement - It ensures that both parties are aware of any encumbrances, liens, or other legal impediments to the sale.

Tennessee Divorce Contract - Couples can detail how future disputes will be resolved, often including mediation or arbitration clauses.

Trailer Bill of Sale Tennessee - Utilizing a Trailer Bill of Sale is considered best practice in personal property transactions, ensuring a transparent and verifiable sale.