Get Alc 119 Tennessee Template in PDF

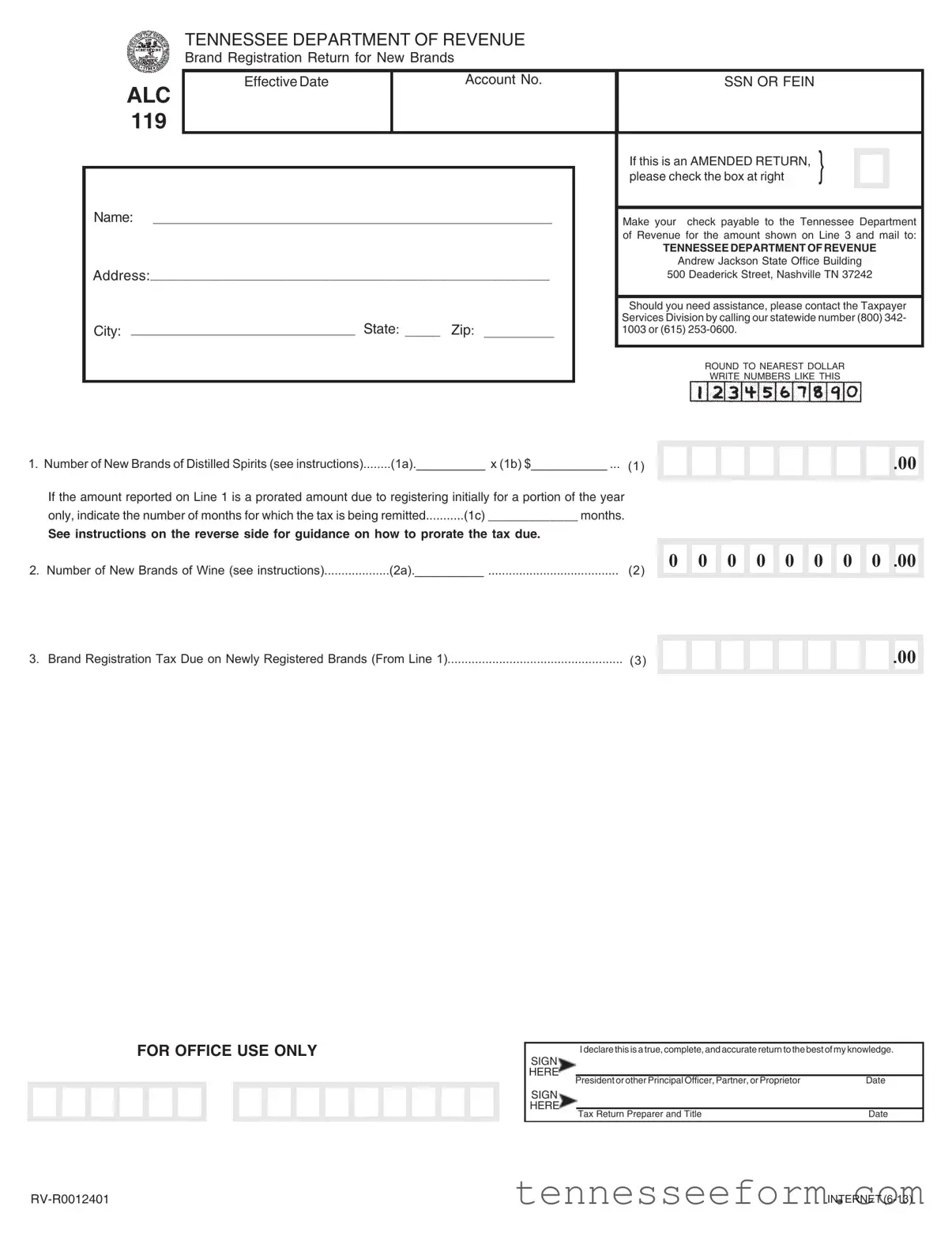

In the realm of alcoholic beverage distribution within Tennessee, navigating the bureaucratic intricacies is key to ensuring compliance with state regulations. Central to this endeavor is the Alc 119 form, a mandatory document known as the Brand Registration Return for New Brands, which companies must submit to the Tennessee Department of Revenue for the registration of new brands of distilled spirits and wine. This comprehensive form requires detailed information about the registrant, including the effective date, account number, and identification numbers such as the SSN or FEIN, alongside a declaration that an amended return is not being filed unless indicated. Crucially, the form delineates specific instructions for calculating the registration tax due on newly registered brands of distilled spirits, factoring in proration for partial tax year registrations and exempting new brands of wine from registration tax. Moreover, the submission process mandates accompanying documentation, including copies of the non-resident Tennessee license, federal basic permit, brand label, and the Tennessee wholesaler contract, ensuring that all brands are properly licensed and accounted for. Payment equivalent to the tax calculated on Line 3 must accompany this return, which is then to be mailed to the Tennessee Department of Revenue. This intricate process not only helps maintain the integrity of the state's alcoholic beverage market but also ensures that all entities are contributing their fair share to the state's coffers.

Document Preview Example

TENNESSEE DEPARTMENT OF REVENUE

Brand Registration Return for New Brands

ALC |

Effective Date |

|

Account No. |

SSN OR FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

119 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

If this is an AMENDED RETURN, |

} |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

please check the box at right |

|

|

|

|

|

Name: _________________________________________________________ |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

||||

|

Make your check payable to the Tennessee Department |

|||||||||

|

|

|

|

|

||||||

|

|

|

|

|

of Revenue for the amount shown on Line 3 and mail to: |

|||||

|

|

|

|

|

TENNESSEE DEPARTMENT OF REVENUE |

|||||

|

|

|

|

|

Andrew Jackson State Office Building |

|||||

Address:_________________________________________________________ |

|

500 Deaderick Street, Nashville TN 37242 |

||||||||

|

|

|

|

|

Should you need assistance, please contact the Taxpayer |

|||||

City: ________________________________ State: _____ |

|

|

Services Division by calling our statewide number (800) 342- |

|||||||

Zip: __________ |

|

1003 or (615) |

|

|

|

|

|

|||

|

|

|

|

|

|

|||||

|

|

|

|

|

ROUND TO NEAREST DOLLAR |

|||||

|

|

|

|

|

WRITE NUMBERS LIKE THIS |

|||||

1. Number of New Brands of Distilled Spirits (see instructions) |

(1a).__________ x (1b) $___________ ... |

(1) |

|

If the amount reported on Line 1 is a prorated amount due to registering initially for a portion of the year |

|

||

only, indicate the number of months for which the tax is being remitted |

(1c) _____________ months. |

|

|

See instructions on the reverse side for guidance on how to prorate the tax due.

2. Number of New Brands of Wine (see instructions) |

(2a).__________ |

(2) |

.00

.00

0 0 0 0 0 0 0 0 .00

3. Brand Registration Tax Due on Newly Registered Brands (From Line 1) |

(3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

.00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FOR OFFICE USE ONLY

I declare this is a true, complete, and accurate return to the best of my knowledge.

SIGN

HERE

President or other Principal Officer, Partner, or Proprietor |

Date |

||

SIGN |

|

||

HERE |

|

|

|

Tax Return Preparer and Title |

Date |

||

|

|||

INTERNET

For additional information, contact the Taxpayer Services Division in one of our Department of Revenue Offices:

Chattanooga |

Jackson |

Johnson City |

Knoxville |

Memphis |

Nashville |

(423) |

(731) |

(423) |

(865) |

(901) |

(615) |

Suite 350 |

Suite 340 |

204 High Point Drive |

Suite 300 |

3150 Appling Road |

Andrew Jackson Building |

State Office Building |

Lowell Thomas Building |

|

7175 Strawberry |

|

500 Deaderick Street |

540 McCallie Avenue |

225 Martin Luther King Blvd. |

|

Plains Pike |

|

|

Tennessee residents can also call our statewide toll free number at

INSTRUCTIONS

The Brand Registration Return and the accompanying Schedule A must be printed legibly or typed, and each field must be completed fully. A spreadsheet containing the information required on Schedule A may be submitted with this return in lieu of the Schedule A.

This return must be accompanied by the following documents: (a) A copy of the

If the entity completing the return is not the producer, bottler, or manufacturer, the return must be accompanied by a prime American source letter for imported products or an appointment letter for domestic products. If the federal basic permit has the listed products as an additional trade name authorized by such permit, the Department of Revenue will accept this documentation.

The return must be signed and dated by an officer of the company. Payment equal to the amount reported on Line 3 must be submitted with this application. Mail the application and all copies of Schedule A or the accompanying spreadsheet to: Tennessee Department of Revenue, Andrew Jackson State Office Building, 500 Deaderick Street, Nashville, Tennessee 37242.

NOTE: The annual registration tax for brands of distilled spirits is $250. The initial brand registration tax of $250 on any brand(s) of distilled spirits subsequent to the beginning of the privilege tax year is to be prorated on a monthly basis from the date of registration to the end of that privilege tax year. The registration tax for distilled spirits for the subsequent first full privilege tax year shall be based on the average monthly number of cases sold at wholesale during the initial partial privilege tax year times twelve (12). There is no tax due on the initial registration of any brand(s) of wine.

Line1: Enter the number of new brands of distilled spirits being registered for the first time in the first blank field. In the second blank field, enter $250 if registering for the entire tax year. If registering new brands for a portion of the tax year, divide $250 by 12, then multiply that result by the number of months for which the registration applies in the initial year and enter the prorated amount in the second blank field. Multiply the number of new brands entered by the registration fee (either the $250 or the prorated amount) and enter in Line 1.

Line2: Enter the number of new brands of wine being registered for the first time in the blank field. There is no tax due on registering new brands of wine, so this is the only entry required for Line 2.

Line3: Report the amount of tax due from Line 1.

INTERNET

Document Data

| Fact | Details |

|---|---|

| Document Name | ALC 119 Tennessee Brand Registration Return for New Brands |

| Governing Law | Tennessee Alcoholic Beverage Laws |

| Purpose | To register new brands of distilled spirits and wine in Tennessee |

| Requirement for Distilled Spirits | Annual registration tax of $250, prorated if registering during the tax year |

| Requirement for Wine | No initial registration tax due for new brands of wine |

| Additional Documents | Non-resident Tennessee license, federal basic permit, brand label copies, federal C.O.L.A., and original Tennessee wholesaler contract |

| Submission Address | Tennessee Department of Revenue, 500 Deaderick Street, Nashville, TN 37242 |

| Contact Information | Statewide toll-free: 1-800-342-1003, Nashville: (615) 253-0600 |

| Payment Information | Payment must be made payable to the Tennessee Department of Revenue |

Detailed Guide for Using Alc 119 Tennessee

Filling out the ALC 119 form, required by the Tennessee Department of Revenue, is a necessary step for those aiming to register new alcohol brands in the state. This procedural task, while it might seem daunting at first, can be quite straightforward once you understand each step required. By carefully following the instructions and having the necessary documents at hand, applicants can ensure a smoother registration process. It is crucial to complete the form legibly, whether by printing or typing, and to include all required supplementary documents. The process also involves calculating and paying the appropriate registration tax for new brands of distilled spirits, although it should be noted that initially registering wine brands does not incur a tax. Here's a step-by step guide to help you through the application process.

- Start by writing the effective date of your return in the space provided.

- Enter your account number, Social Security Number (SSN), or Federal Employer Identification Number (FEIN) as applicable.

- If you are amending a previous return, make sure to check the "AMENDED RETURN" box.

- Write the name of the registrant in the “Name” field.

- Fill out the address section, including city, state, and zip code, of the registrant.

- For Line 1, enter the total number of new distilled spirit brands you are registering.

- In the first blank field (1a), write the number of brands.

- In the second blank (1b), enter $250 if registering for the entire tax year. For partial year registrations, calculate the prorated fee: divide $250 by 12, multiply by the number of months of registration, and enter this amount.

- If Line 1’s amount is prorated, specify the number of months you're paying for in the third blank (1c).

- For Line 2, simply enter the total number of new wine brands you’re registering. Remember, there's no tax due for these, so the entry for tax will be $0.

- In Line 3, input the total brand registration tax due for newly registered distilled spirits brands, as calculated in Line 1.

- Sign and date the form where indicated, ensuring an authorized company officer completes this section.

- Make sure a tax return preparer signs and titles the form if applicable.

- Compile the required documents to accompany your form:

- A copy of the non-resident Tennessee license for the registrant.

- The federal basic permit.

- A copy of the brand label for each brand.

- The federal Certificate of Label Approval (COLA) for each brand.

- The original Tennessee wholesaler contract for each brand.

- A prime American source letter for imported products or an appointment letter for domestic products, if applicable.

- Make your check payable to the Tennessee Department of Revenue for the amount shown on Line 3.

- Mail the completed form, along with all accompanying documents and payment, to the specified address: Tennessee Department of Revenue, Andrew Jackson State Office Building, 500 Deaderick Street, Nashville, Tennessee 37242.

Following these steps accurately and thoroughly will help ensure your registration process is completed correctly. For any questions or needed assistance, reaching out to the Taxpayer Services Division via the provided contact numbers can provide further guidance. Remember, completing this form accurately is crucial for the legal registration and tax compliance of new alcohol brands in Tennessee.

Important Questions on This Form

What is the purpose of the Alc 119 Tennessee form?

The Alc 119 Tennessee form is specifically designed for the registration of new alcohol brands with the Tennessee Department of Revenue. This includes both distilled spirits and wines that are being registered in the state for the first time. The process ensures that these brands are properly recorded, taxed, and in compliance with state regulations. The form requires details about the brand, along with any fees due for the registration process.

Who needs to file the Alc 119 Tennessee form?

This form must be filed by entities introducing new brands of distilled spirits or wine into Tennessee's market. Specifically, producers, bottlers, or manufacturers looking to distribute their alcohol brands in Tennessee must complete and file this form. If the entity completing the return is not the producer, bottler, or manufacturer, documentation such as a prime American source letter for imported products or an appointment letter for domestic products must accompany the form.

What documents are required to accompany the Alc 119 Tennessee form?

Filing the Alc 119 form requires including several important documents:

- A non-resident Tennessee license issued by the Tennessee Alcoholic Beverage Commission.

- A copy of the federal basic permit.

- A copy of the brand label(s). If a brand is distributed under more than one label, each respective label must be furnished.

- A copy of the federal Certificate of Label Approval (C.O.L.A.) for each brand.

- The original Tennessee wholesaler contract, listing the exact brand name.

How is the tax for registering a new brand of distilled spirits calculated?

The initial registration tax for brands of distilled spirits is set at $250. If registering a brand partway through the tax year, this fee is prorated based on the number of months remaining in the tax year. To calculate, divide $250 by 12 to find the monthly rate, then multiply by the number of months the registration covers. This prorated fee should be reported on Line 1 of the form. For subsequent full tax years, the tax is based on the average monthly number of cases sold at wholesale during the initial, partial tax year, multiplied by twelve.

Is there a tax due for registering new brands of wine?

No, there is no tax due for the initial registration of any brand(s) of wine. This makes the process of introducing new wine brands to the Tennessee market more accessible. Registrants simply need to complete the relevant section of the Alc 119 form to ensure their new wine brands are officially recorded with the Tennessee Department of Revenue.

Where and how do I submit the Alc 119 Tennessee form and the associated payment?

The completed Alc 119 form, along with all required documents and payment equal to the amount on Line 3 of the form, should be mailed to the Tennessee Department of Revenue at the Andrew Jackson State Office Building, located at 500 Deaderick Street, Nashville, Tennessee 37242. Make sure the check for the payment is made payable to the Tennessee Department of Revenue. It's important to ensure all parts of the form are filled out accurately and legibly to avoid any processing delays.

Common mistakes

Filling out the ALC 119 Tennessee form, which is essential for brand registration, often includes mistakes that can lead to unnecessary delays or complications. Understanding and avoiding these mistakes can streamline the process and ensure a smoother submission.

One common mistake is not providing a complete set of accompanying documents. The form requires specific documents such as a copy of the non-resident Tennessee license, the federal basic permit, brand labels, the federal Certificate of Label Approval (C.O.L.A.), and the original Tennessee wholesaler contract. Failing to attach any of these documents can lead to the rejection of the application.

Another mistake involves incorrectly calculating the tax amount due on newly registered brands. The ALC 119 form outlines a specific method for calculating the tax, which includes prorating for partial year registrations. Often, errors are made by not following the given formula for prorating the tax or by misunderstanding the tax rate for distilled spirits versus wine, where there is no initial registration tax for wine.

Moreover, applicants sometimes enter inaccurate information regarding the number of new brands of distilled spirits or wine. This is crucial since it directly affects the tax calculation. Ensuring accuracy in these figures is essential for a correct submission.

Additionally, legibility and completeness of the form and attached Schedule A or spreadsheet can be a stumbling block. The instructions specify that the form and Schedule A must be printed legibly or typed and fully completed. Submissions that are hard to read or incomplete are likely to encounter processing delays.

Another area where mistakes occur is in the signature section. The form must be signed and dated by an officer of the company or the individual responsible for the submission. Sometimes, this requirement is overlooked or improperly completed, which can invalidate the submission.

Failing to provide a correct payment matching the amount reported on Line 3 is also a common mistake. The check must be made payable to the Tennessee Department of Revenue for the exact amount due. Discrepancies between the reported amount and the payment can lead to processing issues.

Finally, not checking the amended return box when submitting an amendment to a previously filed return is a frequent oversight. This box is crucial for the Department of Revenue to differentiate between an original submission and an amendment, ensuring the correct processing of the form.

To avoid these pitfalls, it is advisable to carefully review the form's instructions and ensure all information is accurate and complete before submission. Double-checking accompanying documents, calculations, and payment details can save time and prevent issues with the submission process.

Documents used along the form

When businesses deal with alcohol brand registration in Tennessee, they use the ALC 119 form, which serves as the Brand Registration Return for New Brands. This form is a crucial element for companies looking to introduce new alcohol brands to the market, helping ensure compliance with state regulations. However, the ALC 119 form is often not the only document required in this process. Several other forms and documents frequently accompany the ALC 119 form to complete the registration seamlessly and comply thoroughly with the various legal and regulatory requirements.

- Tennessee Non-Resident Seller's License Application: This document is necessary for brands based outside of Tennessee. It establishes the legal authority to sell alcoholic beverages within the state.

- Federal Basic Permit: Issued by the Alcohol and Tobacco Tax and Trade Bureau (TTB), this permit is essential for entities involved in the production, blending, or importing of alcohol.

- Brand Label: A copy of the label used on the alcohol product is required for registration. If multiple labels are used for the same product, copies of each label must be submitted.

Certificate of Label Approval (COLA): Also issued by the TTB, this certificate is proof that the label complies with federal labeling requirements. - Wholesaler Contract: The original contract between the brand and a Tennessee wholesaler must be submitted, detailing the agreement for distribution and sales.

- Prime American Source Letter: For imported products, this letter confirms that the entity registering the product is the primary source of the product in the United States.

- Appointment Letter: For domestic products, this letter from the manufacturer appoints the distributor or registrant as the brand’s representative in Tennessee.

- Proof of Trademark Registration: If the brand is trademarked, a copy of the trademark registration provides legal assurance of the brand’s protected status.

- Business License: Proof of a valid business license ensures that the entity registering the brand is legally permitted to conduct business within the state.

- Articles of Incorporation or Organization: These documents are necessary for verifying the legal structure and existence of the business entity registering the brand.

Together with the ALC 119 form, these documents form a comprehensive packet to facilitate the alcohol brand registration process in Tennessee. By submitting a complete and accurate set of documents, companies can navigate the regulatory landscape more effectively, ensuring a smoother introduction of their brands to the market. Remember, the specific requirements may vary depending on the nature of the alcoholic beverage and the business structure of the entity making the registration. It's always a good idea to consult with legal counsel or the Tennessee Department of Revenue for guidance tailored to your specific situation.

Similar forms

The Alc 119 Tennessee form, used for brand registration return for new brands of alcoholic beverages, has similarities with several other types of regulatory and tax forms. These include applications and returns related to the alcohol industry across various states, as well as forms used in other regulated industries for registering products, paying taxes, and ensuring compliance with state laws.

A similar document is the "New Business Registration" forms used by state Departments of Revenue for businesses to register for a tax identification number. Like the Alc 119, these forms require personal and business identification details, but their scope encompasses a broader range of business activities beyond alcohol brand registration. They serve a foundational role for new businesses to establish their tax reporting requirements with the state.

The "TTB F 5100.31 – Application for and Certification/Exemption of Label/Bottle Approval (COLA)" form required by the Alcohol and Tobacco Tax and Trade Bureau (TTB) at the federal level shares similarities with the Alc 119. Both require details about the product, such as brand and label information. However, the TTB form focuses more on the federal approval of labels for alcoholic beverages, ensuring they meet all requirements before going to market.

Another analogous document is the "State Alcohol Excise Tax Return" that businesses must file to report and pay taxes on the sale of alcoholic beverages. While the Alc 119 form focuses on the initial registration and taxation of new alcohol brands in Tennessee, the excise tax return is concerned with ongoing sales and the taxes incurred from these sales, highlighting the lifecycle of regulatory compliance for alcohol products.

The "Non-Resident Dealer License Application" form, required for out-of-state alcohol vendors to sell products within a state, has similarities with the Alc 119. Both involve regulatory compliance and the need to provide detailed information about the business and its products. However, the non-resident license application specifically facilitates cross-state commerce in the alcohol industry.

Forms like the "Food Facility Registration" required by the Food and Drug Administration (FDA) for businesses that manufacture, process, pack, or hold food products for consumption in the United States also share a common purpose with the Alc 119. Even though one is for food and the other for alcoholic beverages, both types of forms are essential for regulatory compliance, safety, and public health.

The "Trademark Application" forms submitted to the United States Patent and Trademark Office (USPTO) share the concept of brand registration with the Alc 119, albeit in a different context. While the Alc 119 is specific to registering alcohol brands with the Tennessee Department of Revenue for tax purposes, trademark applications are broader in scope, seeking legal protection for brand names, logos, and slogans across all types of products and services.

Last, the "Environmental Impact Assessment" forms, which may be required for businesses that could affect the environment, although not directly related to brand registration or the alcohol industry, encapsulate the theme of regulatory compliance for new initiatives. Like the Alc 119, these forms are part of the preparatory work necessary for businesses to address regulatory requirements before starting a new project or launching a new product.

Dos and Don'ts

Filling out the ALC 119 Tennessee form, a key document for brand registration, can be a straightforward process if you know what to do and what to avoid. Paying attention to the form's requirements will help ensure your submission is successful. Below is a guide with dos and don'ts to make the process as smooth as possible.

Do:

- Double-check that you have entered the correct Effective Date, Account No., SSN or FEIN, and indicated whether it is an amended return clearly. Accuracy in these fields is crucial for your form's processing.

- Ensure that every document required is attached, including a copy of the non-resident Tennessee license, the federal basic permit, the brand label(s), the federal C.O.L.A., and the original Tennessee wholesaler contract for each brand being registered. Missing documents can cause delays.

- Print or type the accompanying Schedule A legibly. If preferred, submit a spreadsheet containing all the required information as specified in the instructions, ensuring it's easy to read and understand.

- Sign and date the return as indicated, ensuring that an officer of the company completes this section. An unauthorized signature can invalidate your entire submission.

Don't:

- Forget to prorate the tax due if registering for a portion of the year. Calculate the tax accurately based on the number of months you're registering the distilled spirits brands. Incorrect calculations can result in underpayment or overpayment.

- Omit any section of the form or accompanying documents; incomplete submissions will likely be returned or delayed.

- Round off numbers incorrectly. Remember, the instructions specify to round to the nearest dollar. Incorrect rounding could affect your tax liability.

- Delay in submitting your form and payment. Ensure your documents are mailed to the Tennessee Department of Revenue in a timely manner to avoid any penalties or late fees associated with late registration.

By following these guidelines carefully, you can minimize potential issues and ensure your brand registration in Tennessee is a success. Remember, the state's requirements are there to ensure that all registrants meet the standard criteria and that the process is fair and consistent for everyone.

Misconceptions

Understanding the intricacies of the ALC 119 Tennessee form, which deals with brand registration returns for new brands of alcoholic beverages, can often lead to misconceptions. Here are six common misunderstandings and the facts to clear them up:

- Misconception #1: The form is only for alcohol producers based in Tennessee.

This is incorrect. The ALC 119 form is used by any entity, regardless of its location, registering a new brand of alcoholic beverage to be sold in Tennessee. This includes out-of-state producers who must comply with Tennessee's Department of Revenue requirements.

- Misconception #2: The brand registration is a one-time process.

Actually, while initial registration is essential, brands need to renew their registrations annually. This process ensures that all the brands remain compliant with any changes in legislation or taxation requirements.

- Misconception #3: There is a registration tax for new brands of wine.

Contrary to this belief, there is no tax due on the initial registration of any brand(s) of wine. The registration tax applies solely to distilled spirits, with an initial fee and a prorated amount if registration does not coincide with the beginning of the tax year.

- Misconception #4: A single document is sufficient for brand registration.

In reality, several documents are required alongside the ALC 119 form, including a copy of the non-resident Tennessee license, the federal basic permit, brand label(s), the federal C.O.L.A. (Certificate of Label Approval), and the Tennessee wholesaler contract with the exact brand name listed. Additional documentation may be required for imported or domestically appointed products.

- Misconception #5: The registration fee is negotiable.

The fee for registering a new brand of distilled spirits is fixed at $250, or a prorated amount if applicable, and is not subject to negotiation. This standardized fee ensures equality and fairness in the registration process for all brands.

- Misconception #6: Assistance is difficult to obtain.

On the contrary, the Tennessee Department of Revenue offers several ways to get help, including a statewide number and specific offices across Tennessee. Assistance is readily available for anyone needing clarification or help with the registration process.

Through understanding these aspects of the ALC 119 form, companies can more effectively navigate the process of registering new alcoholic beverage brands in Tennessee, ensuring compliance and avoiding potential setbacks.

Key takeaways

Filling out the Alc 119 Tennessee form, a Brand Registration Return for New Brands, requires your attention to detail and an understanding of the process. Here are key takeaways for successfully completing and using the form:

- Importance of accuracy: The form must be printed legibly or typed out completely, ensuring all fields are fully completed to avoid processing delays or rejections.

- Required documents: Alongside the Alc 119 form, you must include a copy of the non-resident Tennessee license, federal basic permit, brand label(s), federal C.O.L.A. for each brand, and the Original Tennessee wholesaler contract with exact brand names listed.

- Additional documentation for imports and appointments: If the return is filed by someone other than the producer, bottler, or manufacturer, you'll need to provide a prime American source letter for imported products or an appointment letter for domestic products.

- Payment: The form must be accompanied by a payment equal to the amount reported in line 3. Make checks payable to the Tennessee Department of Revenue.

- Mailing the form: Send the completed application, payment, and all required documents to the Tennessee Department of Revenue at their designated address.

- Proration of tax: The initial brand registration tax for distilled spirits must be prorated if registering after the start of the privilege tax year. This proration is based on the portion of the year for which the registration applies.

- No initial registration tax for wine brands: There's no tax due for the initial registration of any wine brands, simplifying the process for wine producers.

- Signing requirement: An officer of the company must sign and date the form, affirming the accuracy and completeness of the information provided.

- Seeking assistance: If any issues arise or clarification is needed, don't hesitate to reach out to the Taxpayer Services Division via their statewide number or specific office contacts provided in the instructions.

By carefully following these guidelines, you can ensure a smooth submission process for registering new alcohol brands in Tennessee, adhering to legal requirements, and supporting your business's compliance efforts.

Create Other Documents

Tennessee Ps 0376 - Includes provisions for listing a designated contact to handle alleged violation notices from the regulatory authority.

What Disqualifies You From Unemployment in Tennessee - An essential legal tool in Tennessee, providing landlords a framework to address and rectify tenant lease violations effectively.