Get 450 Tennessee Template in PDF

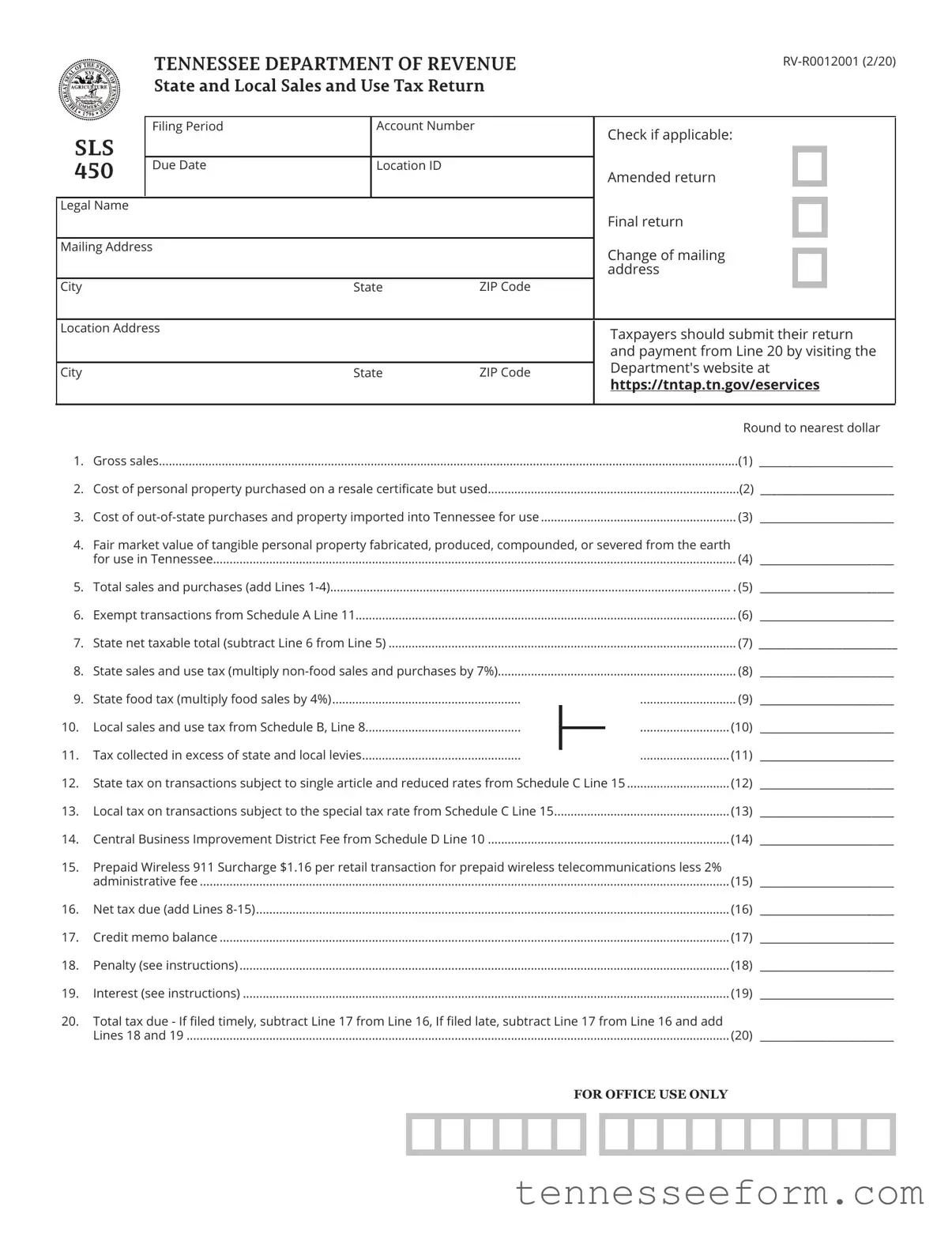

The 450 Tennessee form, officially referred to as the State and Local Sales and Use Tax Return, is a comprehensive document designed by the Tennessee Department of Revenue to detail the various aspects of sales and use tax obligations for businesses operating within the state. This form encompasses a wide array of categories including gross sales, exemptions, taxable totals, as well as specific taxes on certain types of transactions like the Central Business Improvement District Fee and the Prepaid Wireless 911 Surcharge. Businesses are required to meticulously calculate their net taxable sales after accounting for exempt transactions, which are further elaborated in Schedule A, and then apply both state and local tax rates as appropriate, with particular attention to tax collected in excess of state and local levies. Attention to detail is crucial when filling out the form, as it also includes sections for adjustments related to out-of-state purchases, single article sales at special tax rates, and specific sales like food and industrial machinery, requiring accuracy in reporting to comply with state tax regulations. Updates and amendments to the return involve indicating changes such as final returns, mailing address updates, or corrections to previously submitted figures. The structure of the form demands thorough documentation, while its digital submission through the Tennessee Department of Revenue's website simplifies the process, ensuring businesses can fulfill their tax obligations efficiently and accurately.

Document Preview Example

TENNESSEE DEPARTMENT OF REVENUE |

|

STATE AND LOCAL SALES AND USE TAX RETURN |

|

|

Filing Period |

|

Account Number |

|

SLS |

|

|

|

|

450 |

Due Date |

|

Location ID |

|

|

|

|

|

|

Legal Name |

|

|

|

|

|

|

|

|

|

Mailing Address |

|

|

|

|

|

|

|

|

|

City |

|

State |

ZIP Code |

|

|

|

|

|

|

Check if applicable:

Amended return

Final return

Change of mailing address

Location Address

City |

State |

ZIP Code |

Taxpayers should submit their return and payment from Line 20 by visiting the Department's website at

https://tntap.tn.gov/eservices

|

|

|

|

Round to nearest dollar |

|

1. |

Gross sales |

(1) |

________________________ |

||

2. |

Cost of personal property purchased on a resale certificate but used |

(2) ________________________ |

|||

3. |

Cost of |

(3) |

________________________ |

||

4. |

Fair market value of tangible personal property fabricated, produced, compounded, or severed from the earth |

|

|

||

|

for use in Tennessee |

(4) |

________________________ |

||

5. |

Total sales and purchases (add Lines |

. (5) |

________________________ |

||

6. |

Exempt transactions from Schedule A Line 11 |

(6) |

________________________ |

||

7. |

State net taxable total (subtract Line 6 from Line 5) |

(7) |

_________________________ |

||

8. |

State sales and use tax (multiply |

(8) |

________________________ |

||

9. |

State food tax (multiply food sales by 4%) |

(9) |

________________________ |

||

10. |

Local sales and use tax from Schedule B, Line 8 |

|

|

(10) |

________________________ |

|

|

||||

|

|

||||

11. |

|

|

|

(11) |

________________________ |

Tax collected in excess of state and local levies |

|||||

12. |

State tax on transactions subject to single article and reduced rates from Schedule C Line 15 |

(12) |

________________________ |

||

13. |

Local tax on transactions subject to the special tax rate from Schedule C Line 15 |

(13) |

________________________ |

||

14. |

Central Business Improvement District Fee from Schedule D Line 10 |

(14) |

________________________ |

||

15.Prepaid Wireless 911 Surcharge $1.16 per retail transaction for prepaid wireless telecommunications less 2%

|

administrative fee |

(15) |

________________________ |

16. |

Net tax due (add Lines |

(16) |

________________________ |

17. |

Credit memo balance |

(17) |

________________________ |

18. |

Penalty (see instructions) |

(18) |

________________________ |

19. |

Interest (see instructions) |

(19) |

________________________ |

20.Total tax due - If filed timely, subtract Line 17 from Line 16, If filed late, subtract Line 17 from Line 16 and add

Lines 18 and 19 |

(20) ________________________ |

FOR OFFICE USE ONLY

Schedule A- Exempt Transactions (See Separate Instructions)

1. |

Net taxable food sales |

(1) |

____________________ |

2. |

Sales made to vendors or other establishments for resale, and sales of items to be used in processing |

|

|

|

articles for sale. (Certificates of Resale required) |

(2) |

____________________ |

3. |

Sales of items paid for with SNAP Benefits |

(3) |

____________________ |

4. |

Sales to federal or Tennessee governments and qualified nonprofit institutions (Certificate required) |

(4) |

____________________ |

5. |

Returned merchandise reported as sales on this or a previous return. Show on Schedule B, Line 2 |

|

|

|

amounts claimed on Schedule B, Line 4, of prior returns |

(5) |

____________________ |

6. |

Exempt industrial machinery and agricultural purchases |

(6) |

____________________ |

7. |

Sales in interstate commerce |

(7) |

____________________ |

8. |

Repossessions - portion of unpaid principal balances in excess of $500 due on TPP repossessed from |

|

|

|

customers. Report same amount on Schedule B, Line 2 |

(8) |

____________________ |

9. |

Other deductions (See instructions) |

(9) |

____________________ |

10. Sales Tax Holiday (last Friday in July through following Sunday) |

(10) ____________________ |

||

11. Total exemptions (Add Lines 1 through 10; enter here and on First Page, Line 6) |

(11) ____________________ |

||

Attention Sellers located outside Tennessee:

Beginning October 1, 2019, all sales that originate from a business located outside of Tennessee and sold to a destination inside Tennessee must be reported using the tax rate applicable to the delivery destination. Report all your sales made by location using Schedule E and bring total of all sales from Columns C through J over to Lines 1 through 8 below.

Schedule B - Local Sales and Use Tax (See Separate Instructions)

1. |

State net taxable total from First Page, Line 7 |

(1) |

____________________ |

2. |

Adjustments (total of Schedule A, Line 1 and any applicable amounts from Schedule A, Lines 5 and 8) |

(2) |

____________________ |

3. |

Total with adjustments (add Lines 1 and 2) |

(3) |

____________________ |

4. |

Excess amount over single article tax base |

(4) |

____________________ |

5. |

Energy fuel sales taxed at full state rate |

(5) |

____________________ |

6. |

Other deductions including sales of specified digital products and of merchandise sold through vending machines (6) ____________________ |

||

7. |

Net taxable total (subtract Lines 4, 5, and 6 from Line 3) |

(7) |

____________________ |

8. |

Local sales and use tax (multiply Line 7 x the applicable local tax rate; Enter here and on the first page, Line 10).... |

(8) |

____________________ |

Schedule C - State Single Article Tax and Special Tax Rates (See Separate Instructions) If no taxable single articles were sold at $1,600 or above, or if you have no special tax rate products to report, put $0 on Lines 9 and 15 below

and on Lines 12 and 13 on the first page.

1. |

Taxable single article sales from $1,600 to $3,200 |

(1) |

___________________ |

2. |

State single article sales tax (multiply Line 1 x 2.75%) |

(2) |

___________________ |

3. |

Industrial water sales |

(3) |

___________________ |

4. |

Industrial water tax (multiply Line 3 x 1.00%) |

(4) |

___________________ |

5. Industrial energy fuel sales |

(5) |

___________________ |

|

6. |

Industrial energy fuels tax (multiply Line 5 x 1.50%) |

(6) |

___________________ |

7. |

Aviation fuel tax (total amounts from Lines A and B; multiply x 4.50%) |

(7) ____________________ |

|

A.Taxable aviation fuel sales ($__________) Gallons (__________)

B.

8. Water carrier energy fuel tax (total amounts from Lines A and B; multiply x 7.00%) |

|

|

(8) ____________________ |

|||

|

A. Taxable energy fuel sales to water carriers ($__________) Gallons (__________) |

|

|

|

||

|

|

|

|

|||

|

B. |

|

|

|

|

|

|

|

|

|

|

||

9. State single article and reduced rates tax (Add Lines 2, 4, 6, 7, and 8) |

|

|

(9)___________________ |

|||

|

|

|||||

|

Enter here and on Line 12 on the first page |

|

|

|

||

10. Local industrial water tax (multiply total sales x 0.50%) |

|

|

(10) __________________ |

|||

11. Specified digital products sales |

|

|

(11) __________________ |

|||

12. Specified digital products local tax (multiply Line 11 x 2.50%) |

|

|

(12) __________________ |

|||

13. Sales of merchandise through vending machines |

|

|

(13) __________________ |

|||

14. Local tax on merchandise sold through vending machines (Multiply Line 13 x 2.25%) |

|

|

(14) __________________ |

|||

15. Total local special rates tax (Add Lines 10, 12, and 14). Enter here and on Line 13 on the first page |

(15) __________________ |

|||||

|

Schedule D- Central Business Improvement District (CBID) Schedule |

|

|

|

||

1. |

Gross sales less exempt transactions (Page 1, Line 1 minus Line 6) plus net taxable food sales |

|

|

|

||

|

(Schedule A, Line 1) |

|

|

(1) ___________________ |

||

2 . Sales of professional services included in Line 1 above |

|

|

(2) ___________________ |

|||

3. |

Sales of lodging provided to transients not included in exempt transactions |

|

|

(3) ___________________ |

||

4. |

Sales of tickets to sporting events or other live ticketed events not included in exempt transactions |

(4) ___________________ |

||||

5. |

Sales of alcoholic beverages subject to LBD tax not included in exempt transactions |

|

|

(5) ___________________ |

||

6. |

Sales of newspapers and other publications not included in exempt transactions |

|

|

(6) ___________________ |

||

7. |

Sales of overnight and |

|

|

(7) ___________________ |

||

8. |

Total CBID Exempt Sales - add Lines 2 - 7 |

|

|

(8) ___________________ |

||

9. |

Net Sales - subtract Line 8 from Line 1 |

|

|

(9) ___________________ |

||

10. Central Business Improvement District Fee - multiply Line 9 x 0.25%. Enter here and on page 1, Line 14 |

(10)___________________ |

|||||

|

|

|

||||

|

|

Under penalties of perjury, I declare that I have examined this report, and to the best of my knowledge and belief, |

||||

|

|

it is true, correct, and complete. |

|

|

|

|

|

|

____________________________________________________ |

_____________________ __________________________________________ |

|||

|

|

Taxpayer's Signature |

Date |

Title |

|

|

|

|

____________________________________________________ |

_____________________ ________________ |

________________________ |

||

|

|

Tax Preparer's Signature |

Preparer's PTIN |

Date |

Telephone |

|

|

|

____________________________________________________ |

____________________________ ________ |

________________________ |

||

|

|

Preparer's Address |

City |

|

State |

ZIP Code |

|

|

Preparer's Email Address____________________________________________________________________________________________ |

||||

|

|

|

|

|

|

|

Schedule E - For Sellers Located Outside Tennessee Destination Sales Report

A |

B |

C |

D |

E |

F |

|

G |

|

H |

|

I |

|

J |

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or County |

Sales Tax |

State Net |

Adjustments |

Adjusted |

Excess of |

|

Energy Fuel |

|

Other |

|

Local Net |

|

|

Location |

Holiday |

Taxable Total |

Total |

Single Article |

|

Sales |

|

Deductions |

|

Taxable Total |

|

Local Tax |

|

|

|

|

|

|

Tax Base |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Totals |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note: If you have additional entries to report, please add additional Schedules as needed. Report total of all sheets on last page.

Document Data

| Fact Name | Description |

|---|---|

| Form Title | TENNESSEE DEPARTMENT OF REVENUE STATE AND LOCAL SALES AND USE TAX RETURN |

| Form Number | RV-R0012001 (2/20) SLS 450 |

| Purpose | Used for reporting state and local sales and use tax. |

| Submission Method | Taxpayers submit their return and payment online via the Department's website. |

| Special Features | Includes provisions for amended returns, final returns, and changes of mailing address. |

| Governing Law | Tennessee sales and use tax regulations. |

Detailed Guide for Using 450 Tennessee

After completing the 450 Tennessee form, the process does not end with the final signature or online submission. The Tennessee Department of Revenue requires individuals and businesses to stay informed about their tax obligations and ensure that all future filings are done accurately and by the due dates. This proactive approach helps in avoiding penalties and interest charges. Furthermore, it's essential to maintain records of all filed returns and payments, as these documents are crucial during any possible audits by the Department. Now, let's walk through the step-by-step process of filling out the 450 Tennessee form.

- Filing Period: Enter the specific period for which you are filing.

- Account Number SLS 450: Input the account number assigned to you by the Tennessee Department of Revenue.

- Due Date: Mark the due date for the filing.

- Location ID: Provide the unique location ID.

- Legal Name, Mailing Address, City, State, ZIP Code: Fill in the legal name of your entity and the full mailing address where it is registered.

- Check the appropriate box if this is an Amended return, Final return, or if there's a Change of mailing address.

- Location Address: If different from the mailing address, provide the physical location address of your entity.

- Schedule A - Exempt Transactions: Report exempt transactions as instructed, including specific details in the provided fields.

- Sales and Tax Calculations: Follow the form’s sequence from "Gross sales" to "Prepaid Wireless 911 Surcharge," inputting amounts in each line based on your sales records, ensuring to round to the nearest dollar as prompted.

- Schedule B - Local Sales and Use Tax: Calculate and input the local sales and use tax details as directed.

- Schedule C - State Single Article Tax and Special Tax Rates: If applicable, enter details for taxable single article sales and special tax rates, including any exempt amounts.

- Schedule D - Central Business Improvement District Fee: Fill in the required fields if your business is located within a Central Business Improvement District.

- Under penalties of perjury, sign and date the form, providing your title. If a tax preparer completed the form, ensure their signature, PTIN, date, telephone number, address, and email address are also included.

- Schedule E - For Sellers Located Outside Tennessee: Complete this section if applicable, detailing Destination Sales Report for compliance with the October 1, 2019 mandate.

Successfully completing and submitting the form ensures compliance with the Tennessee Department of Revenue's requirements. It’s advisable to review your submission for accuracy and completeness to prevent any unforeseen issues. Also, keep abreast of any changes in tax legislation that might affect future filings.

Important Questions on This Form

What is the 450 Tennessee form used for?

The 450 Tennessee form, also known as the State and Local Sales and Use Tax Return, is a document utilized by businesses to report their gross sales, the cost of items purchased for resale but used by the business, out-of-state purchases, and the fair market value of items produced for use within Tennessee. This form helps in calculating the sales and use taxes owed to the state and local governments. It covers various taxes including general state and local sales taxes, special single article rates, and other specific surcharges.

How can I submit the 450 Tennessee form?

To submit the 450 Tennessee form, taxpayers are advised to visit the Tennessee Department of Revenue's website at https://tntap.tn.gov/eservices . Here, the return and accompanying payment can be filed electronically. This method ensures accuracy and prompt processing of your sales and use tax return.

What are the penalties for filing the 450 Tennessee form late?

Late filings of the 450 Tennessee form may result in penalties and interest charges. The penalty for late filing is generally calculated as a percentage of the tax due. The specifics of these penalties, including rates and how they are applied, can be found in the instructions that accompany the form. It’s important to file on time and pay any taxes owed by the due date to avoid these additional charges.

Can I amend a previously filed 450 Tennessee form?

Yes, amendments to a previously filed 450 Tennessee form are permissible. To file an amended return, taxpayers should check the "Amended return" box at the top of the form. They should then fill out the form with the corrected information and submit it according to the provided instructions. Amending a return may involve adjusting the amounts reported as sales, taxable income, or tax owed, and may result in either additional tax due or a refund.

Common mistakes

When individuals and businesses fill out the 450 Tennessee form, there are several common mistakes that can lead to inaccuracies or delays in processing. Understanding these errors can help filers avoid unnecessary complications.

- Failing to round to the nearest dollar: The form instructs to round figures to the nearest dollar, but often, decimals are mistakenly included. This might seem minor, but it can cause discrepancies and processing delays.

- Incorrectly reporting gross sales: Another frequent error is not accurately reporting gross sales in line 1. Whether overestimating or underestimating, this mistake impacts the calculation of taxes due and can lead to underpayment or overpayment.

- Omitting exempt transactions: Many filers forget to include exempt transactions on Schedule A. This oversight leads to an inflated taxable total, resulting in a higher tax liability than necessary.

- Misclassifying purchases: Lines 2 and 3 deal with specific types of purchases. Misunderstanding or incorrectly classifying these can significantly affect the tax calculation, especially for out-of-state purchases intended for use in Tennessee.

- Overlooking special taxes and fees: Special taxes and fees, such as those outlined in Schedules C and D for single articles and CBID fees, are often overlooked. Neglecting these sections can lead to inaccuracies in the final tax due.

To ensure accuracy and compliance, it's crucial to:

- Review the form instructions carefully.

- Double-check all figures and round them as required.

- Accurately classify and report all transactions, including exemptions and special tax rates.

- Keep up-to-date records accessible for reference when filling out the form.

Taking the time to understand and correctly complete the 450 Tennessee form can help avoid the common pitfalls many encounter. This attention to detail not only ensures compliance but also optimizes tax liability, helping filers avoid paying more than necessary or facing penalties for underpayment.

Documents used along the form

When dealing with the complexities of tax reporting and compliance, it's common to encounter several documents and forms that go hand-in-hand with the 450 Tennessee form, also known as the State and Local Sales and Use Tax Return. Each of these documents serves a specific purpose, aiding businesses and individuals in accurately reporting their tax obligations to the Tennessee Department of Revenue. Below is a description of up to seven other forms and documents that are commonly used alongside the 450 Tennessee form.

- Schedule A - Exempt Transactions: This schedule is crucial for detailing transactions that are exempt from sales and use tax. It requires taxpayers to list types of exempt sales, such as sales to government entities, sales paid with SNAP benefits, and certain types of machinery or agricultural purchases.

- Schedule B - Local Sales and Use Tax: This document is used for calculating and reporting the local sales and use tax owed. It considers adjustments and deductions from Schedule A to determine the net taxable total that will be subject to local tax rates.

- Schedule C - State Single Article Tax and Special Tax Rates: For items such as high-value single articles or products subject to special tax rates, this schedule helps calculate the additional taxes that may be due. This includes taxes on items like industrial machinery and aviation fuel.

- Schedule D - Central Business Improvement District Fee: This form is used by businesses located within designated central business improvement districts to calculate the special fee they owe based on their gross sales, less any exempt transactions.

- Schedule E - Destination Sales Report: For sellers located outside Tennessee, Schedule E helps report sales made to customers within Tennessee, ensuring the correct local sales tax rate is applied based on the delivery destination.

- Certificate of Resale: This document allows purchasers to buy goods intended for resale without paying sales tax at the time of purchase. It must be presented to the seller to substantiate the exemption claim for resale transactions reported.

- Registration for Tennessee Department of Revenue: Before filing taxes, businesses must register with the Tennessee Department of Revenue. This involves submitting an application that provides essential details about the business, including its legal structure, nature of the business, and identification numbers.

In sum, navigating the tax landscape requires attention to detail and an understanding of how various forms and schedules interact to provide a complete picture of one's tax responsibilities. Whether it's providing detailed information on exempt transactions, calculating local tax obligations, or ensuring accurate reporting of sales across different jurisdictions, each document plays a vital role in the broader tax filing process. Compliance not only helps in avoiding penalties but also ensures businesses contribute their fair share to the community's infrastructure and services.

Similar forms

The Form 1040 used for individual income tax returns by the IRS shares similarities with the 450 Tennessee form in structure and purpose. Both forms require taxpayers to report income, calculate deductions, and determine the amount of tax owed or refund due. They are designed to collect revenue for government operations, albeit at different levels of governance. Taxpayers are guided through a step-by-step calculation process to ensure accurate reporting of their financial obligations.

State sales tax forms from other states, such as the California Sales and Use Tax Return, bear a resemblance to the Tennessee 450 form in their function to report and remit taxes collected from sales. Both types of forms include sections for reporting gross sales, taxable sales, exemptions, and calculations of taxes owed. They serve a regulatory function, ensuring businesses comply with state laws regarding the collection and remittance of sales tax.

The VAT Return forms used in countries with a Value-Added Tax system parallel the 450 Tennessee form in their role in tax administration. While the specifics of VAT differ from sales tax in the U.S., both form types are used to report taxable transactions and calculate the tax due. These forms are critical for businesses to navigate and comply with their respective tax systems, ensuring the accurate flow of revenue to the government.

The Business License Renewal forms, which businesses may need to submit annually or biannually depending on jurisdiction, share a common purpose with the 450 Tennessee form in terms of regulatory compliance. While focusing on the licensing aspect, these forms often include sections related to sales and use tax, highlighting the business's financial and operational statuses over the reporting period.

Quarterly Federal Excise Tax Return forms, like the IRS Form 720, are similar to the Tennessee 450 form in that they address the taxation of specific goods and services at the federal level. Both forms require detailed reporting on the types of items or services sold, tax rates applied, and the calculation of taxes owed. These forms are essential tools for implementing tax policies on specific economic activities.

Employer's Quarterly Federal Tax Return forms, such as the IRS Form 941, are used to report payroll taxes and are similar to the Tennessee 450 form in their periodic nature and the requirement for detailed financial reporting. Businesses must accurately report amounts relating to income, social security, and Medicare taxes, akin to the way sales and use taxes are reported on the 450 form.

The Unemployment Insurance Tax forms, required by state governments, share purposes with the Tennessee 450 in monitoring and collecting taxes critical to funding specific government programs. These forms are crucial for the administration of unemployment benefits, requiring employers to report wages paid and taxes owed on behalf of their workers.

Property Tax Declaration forms, which property owners submit to local taxing authorities, resemble the 450 Tennessee form by mandating the reporting of values and calculation of taxes due. These forms contribute to the funding of local services and infrastructure, requiring detailed information about property characteristics and ownership.

The Fuel Tax Report forms required by states for the reporting of taxes on fuel sales or usage are comparable to the Tennessee 450 form. Businesses involved in the sale or distribution of fuel must meticulously report quantities sold and taxes owed, ensuring compliance with state regulations and the proper collection of revenues designated for transportation and infrastructure funding.

Finally, the Gross Receipts Tax forms, used in certain jurisdictions instead of or in addition to sales tax, resemble the Tennessee 450 form in how they assess business activity. These forms require businesses to report their total revenue, applying tax rates to gross receipts rather than specific sales transactions, illustrating another method by which states collect revenue for public services.

Dos and Don'ts

Filling out the 450 Tennessee form, a state and local sales and use tax return, requires attention to detail to ensure accuracy and compliance with the Tennessee Department of Revenue. Here's a guide to help you navigate this process more effectively:

- Do round all amounts to the nearest dollar to keep the calculations straightforward and compliant with the instructions.

- Do visit the Tennessee Department of Revenue website for the most current filing instructions and to submit your return and payment electronically.

- Do check the appropriate boxes at the top if you are filing an amended return, a final return, or if there is a change of mailing address to ensure your return is processed correctly.

- Do ensure that the Legal Name and all mailing and location addresses are current and accurately reflected to avoid processing delays or miscommunication.

- Do thoroughly review all schedules (A, B, C, D, E) for specific instructions on exempt transactions, local taxes, special rates, and other deductions to ensure your form is complete and accurate.

- Do use Schedule E to report sales made by location if your business is located outside of Tennessee, in accordance with the October 1, 2019, mandate for destination-based sales.

- Don't forget to sign and date the form. An unsigned form is considered incomplete and can lead to processing delays or even penalties.

- Don't leave any fields blank unless instructed. If a section does not apply, enter "$0" or "N/A" to indicate that it was not overlooked.

- Don't estimate or guess figures. Use actual sales data and records to fill out the form accurately to avoid potential audits or penalties.

- Don't ignore the due date. Late filings can result in penalties and interest charges, so it's crucial to submit your form and any payment by the specified deadline.

By following these dos and don'ts, you can ensure a smoother filing process and help avoid common mistakes that could cost your business time and money.

Misconceptions

Understanding the intricacies of tax forms can sometimes feel like wading through thick fog, particularly when grappling with the complexities of state-specific documents like the Tennessee 450 Form, officially known as the State and Local Sales and Use Tax Return. Let's dispel some common misconceptions to clear the air:

- Misconception 1: "The 450 Tennessee form applies only to businesses physically located in Tennessee."

Actually, the form applies to all businesses that sell goods or services in Tennessee, including those located outside the state if they meet certain nexus criteria establishing a significant presence in the state.

- Misconception 2: "Filing the form is only necessary if my business collects Tennessee sales tax."

Filing is required even if you did not collect any sales tax during the reporting period. The form serves not only to remit collected taxes but also to report exempt sales and purchases, among other things.

- Misconception 3: "I only need to report and pay state sales tax, not local sales tax, on the 450 form."

Both state and local sales and use taxes must be reported on the form. Tennessee has a varied local tax structure, and businesses must calculate and report these local taxes based on the jurisdiction of sales or usage of the goods or services.

- Misconception 4: "If I submit an amended return, I cannot file it electronically."

You can and are encouraged to submit both original and amended returns electronically through the Tennessee Department of Revenue's online platform, TNTAP, to ensure accuracy and faster processing.

- Misconception 5: "All my sales are exempt from Tennessee sales tax, so I don't need to file the form."

Even if all your transactions are exempt from sales tax, you are still required to file the form to report those exempt sales. Documentation and proper record-keeping are crucial for all types of sales, taxable or exempt.

- Misconception 6: "There's no need to detail exempt transactions since I'm not paying tax on them."

Reporting exempt transactions on Schedule A of the form is essential. This not only helps validate your tax liabilities (or lack thereof) but also ensures compliance with Tennessee's tax regulations. Detailed reporting supports the exemptions you claim.

Clearing up these misconceptions ensures that businesses can navigate Tennessee's tax obligations with greater confidence and accuracy. Always consider consulting with a tax professional familiar with Tennessee laws to ensure compliance and maximize your business's financial health.

Key takeaways

When completing and utilizing the Tennessee State and Local Sales and Use Tax Return, Form SLS 450, individuals and businesses should be aware of several important aspects to ensure accuracy and compliance:

- All transactions need to be rounded to the nearest dollar, simplifying the calculation process and ensuring consistency throughout the form.

- The form requires detailed information regarding various types of sales and purchases, such as gross sales, purchases for resale that end up being used by the purchaser, and imported goods for use in Tennessee. This diverse data collection ensures that all potential taxable activities are accounted for correctly.

- Individuals and businesses must pay special attention to exemptions listed on Schedule A; these include sales like those made for resale, items purchased with SNAP Benefits, and sales to government or qualified nonprofit institutions. It’s crucial to accurately document these transactions to apply exemptions properly and avoid overpaying taxes.

- For businesses located outside Tennessee, starting October 1, 2019, sales made to destinations within Tennessee must report the tax rate applicable to the delivery destination. This requires sellers to be diligent in keeping track of the differing local tax rates across Tennessee destinations.

- The form also accounts for specialized taxes and fees, such as the Prepaid Wireless 911 Surcharge and the Central Business Improvement District (CBID) Fee, among others. These specifics highlight the requirement for businesses and individuals to be aware of various tax obligations beyond basic sales tax.

Overall, accuracy, completeness, and awareness of specific tax requirements and exemptions are critical when filling out the Tennessee Form SLS 450. Ensuring all transactions are accurately reported in the correct sections and that all applicable exemptions and special tax rates are applied can help avoid common pitfalls, such as underpayment of tax, overpayment, or the need to file amended returns.

Create Other Documents

Tennessee Llc Formation - Documentation facilitating the transition of partnerships to LLPs under Tennessee law, with provision for delayed effective date.

Tennessee Uniform Certification - The certification process includes a detailed review of an applicant’s business to verify disadvantaged status, ownership, control, and size eligibility.